EA Craftsman EA Course 【015】 Do you tend to underestimate it? Which should be valued more: backtesting or forward testing for automated trading?

0

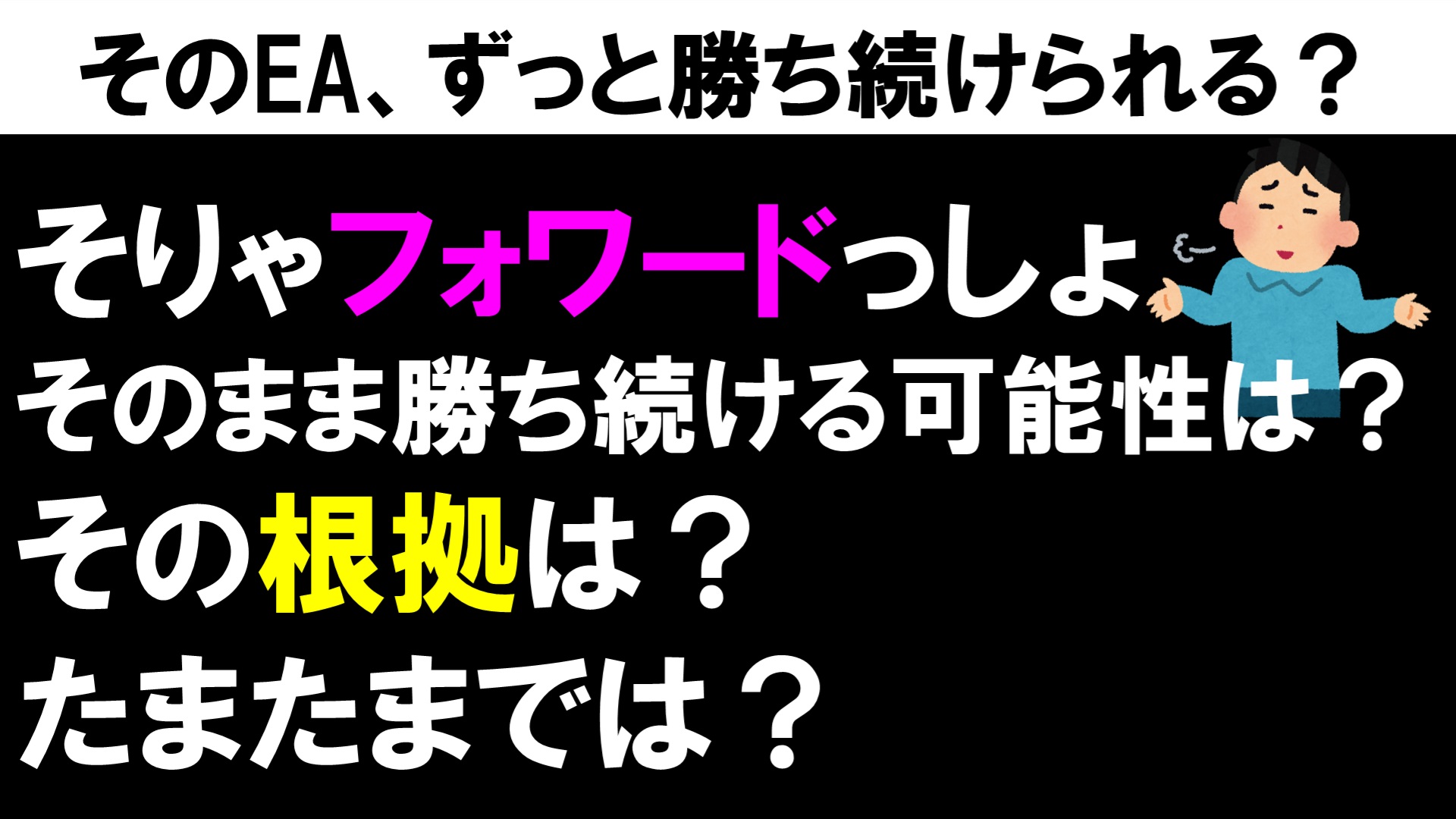

Can that EA stay winning forever?

For those who have been excited by backtest results in the past and operated with a snort of exhaled breath and failed, those who are skeptical or cautious will likely say...“Well, that’s forward testing. No matter how much you show me how much money you made with past data, it alone isn’t trustworthy. If you don’t show me that you’re actually making money in real trading, I won’t believe it.”

I think they would answer like that.

Now, a question: Suppose the EA you are currently operating continues to win steadily, what do you think is the probability that it will continue to win in the same way from now on?

And on what basis do you base that?

Isn’t it just a matter of being lucky?

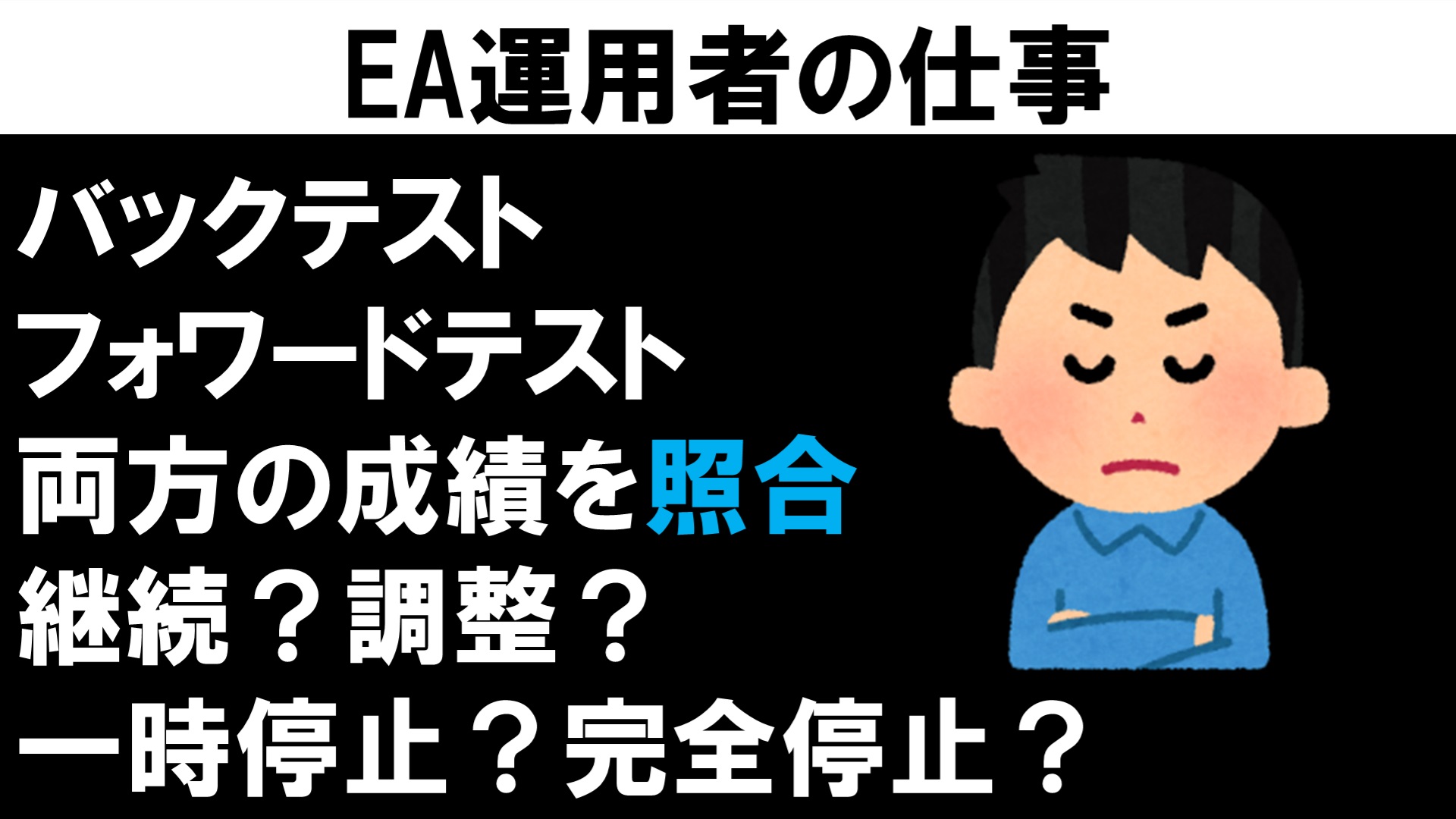

The Job of an EA Operator

When operating an EA, if the operator is doing their own research and analysis, they would likely compare the results of both backtests and forward tests and decide whether to continue the operation as is, adjust position sizing, pause temporarily, stop completely, etc.

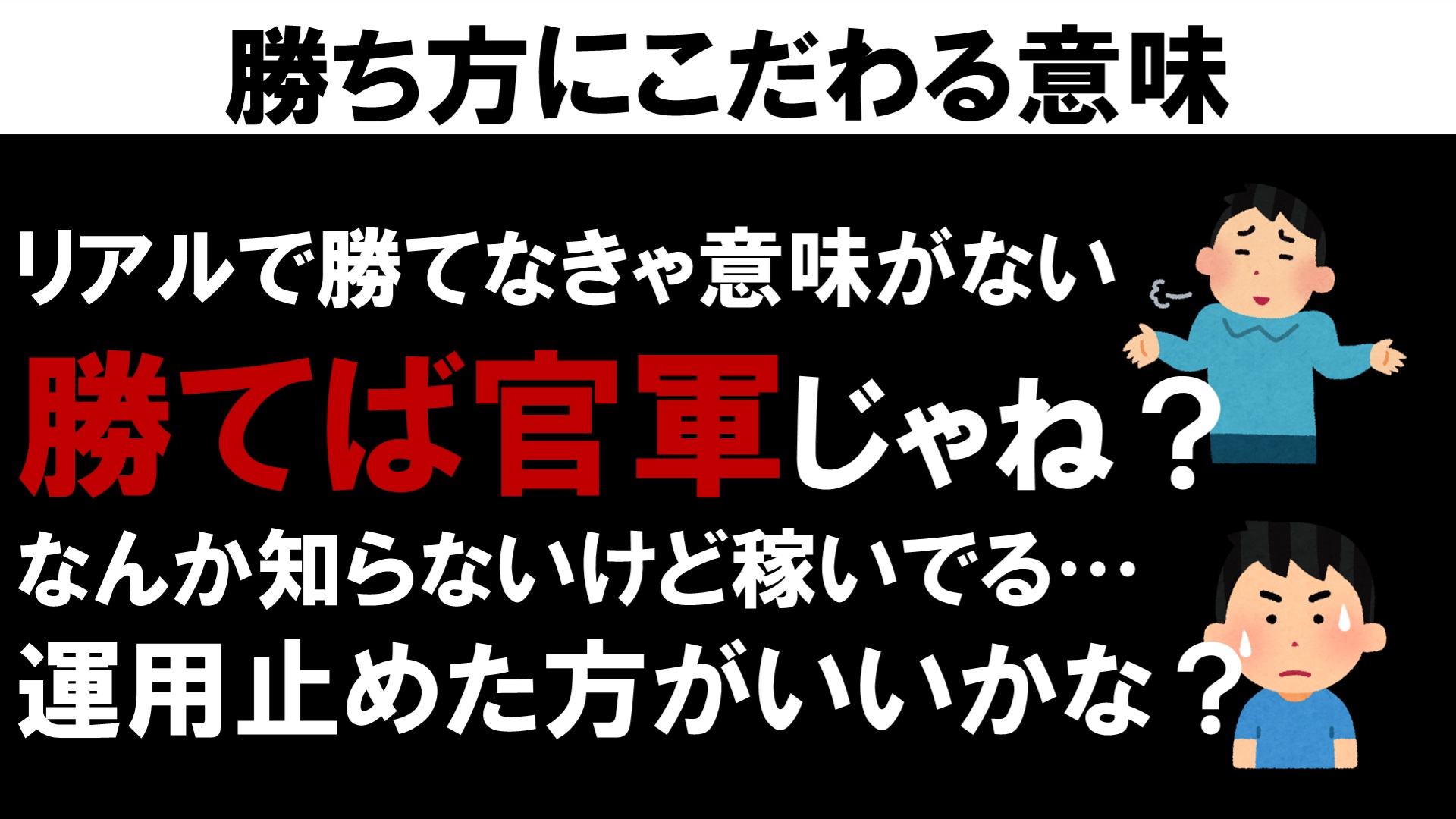

The Meaning of Focusing on Winning Methods

Of course, it’s not acceptable unless you are winning in real trading and forward testing. That’s true.However, simply winning isn’t everything.

“Huh? The goal of trading is to make money, so no matter how you win, winning is winning, right?”

I understand what you’re saying. If that EA will keep making money from now on, that would be fine.

But how would you know that? Isn’t it unsettling to see a state where it’s making money for some reason you don’t understand? Wouldn’t you be scared if a drawdown began in such a state?

“Eh… should I stop using this EA?”

Wouldn’t you worry about that?

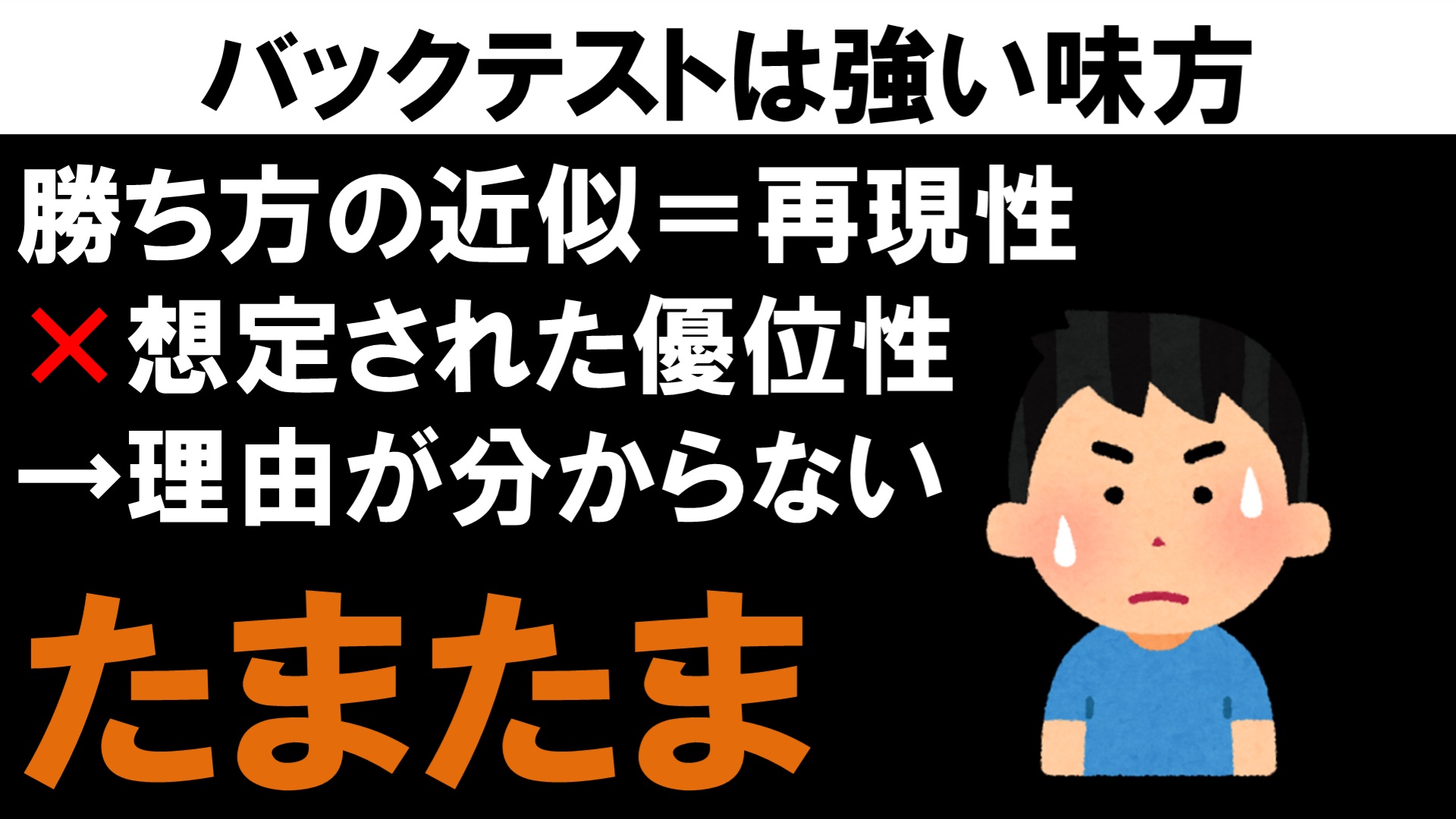

Backtesting Is a Strong Ally

The strong ally at that time is the results of backtesting.You examine how closely the ‘winning method’ in forward testing or real trading approximates the backtest. That is what you look at.

In other words, reproducibility.

If you are making money in the backtest with the same logic, you have a highly reproducible strategy; if you are making money with a completely different winning method, then you are profitable but have low reproducibility.

If you are making money with low reproducibility… in other words, not based on the assumed edge… what you are doing is often described as being lucky.

People call this “just by chance.”

As I mentioned in the 10th lecture, a backtest period should not be too short, but it also isn’t necessarily better if it’s very long. The discussion repeats, so please refer to that article for details.

In short, at least three years, ideally five or more.

However, something like twenty years or a very long period is a bit suspicious. Please see the 10th lecture for the reason.

■The Concept and Operating Policy of the EA I Developed

EA Artisan’s EA (Three Arrows) is here

× ![]()