EA Craftsman’s EA Course [010] About Profitability Ranking of Automated Trading ~ Backtesting Being Long Isn’t Always Better

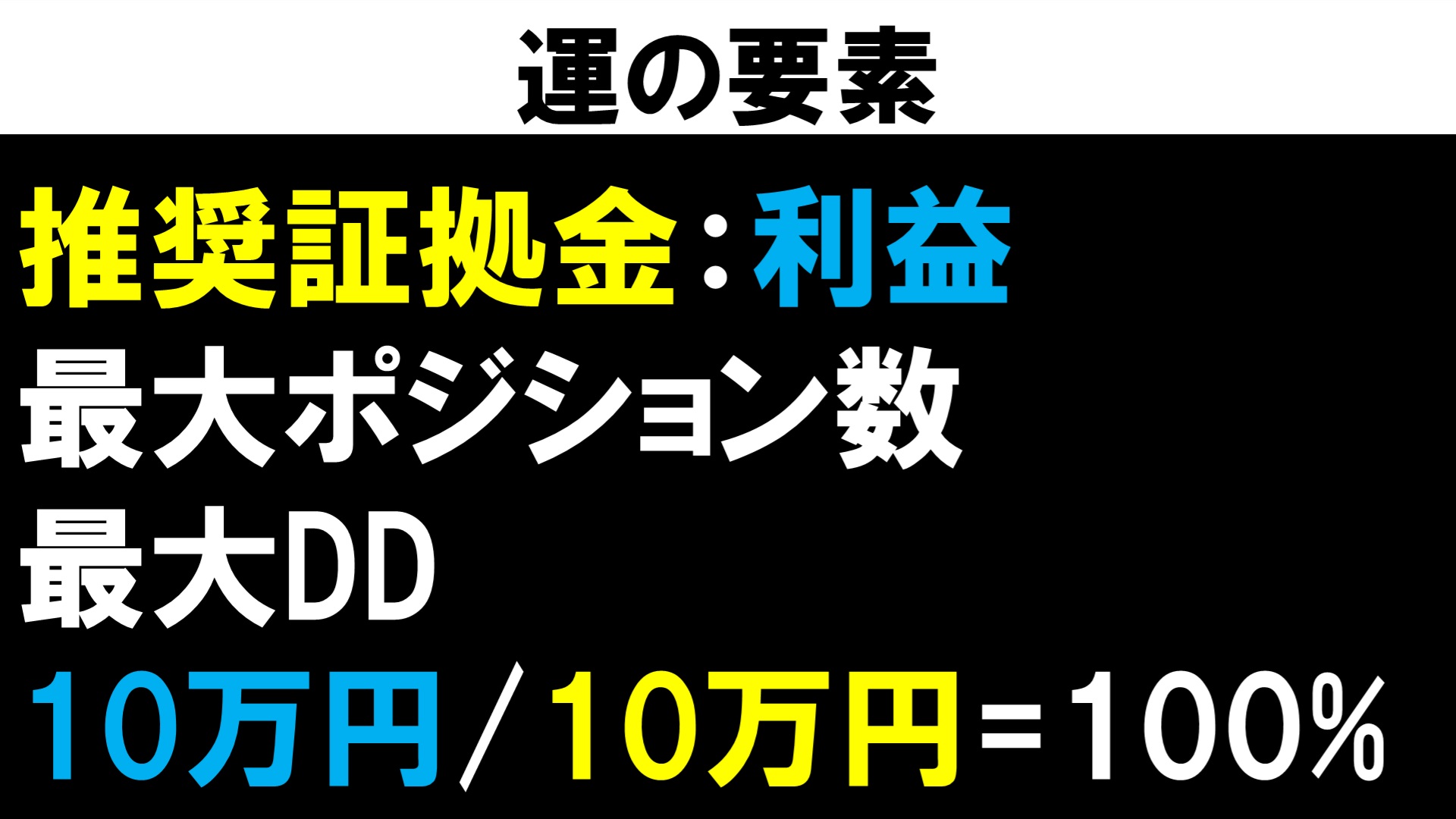

Elements of Luck

In this second installment of the Ranking Series, we discuss the profitability rate.Profitability rate is an indicator of how much you have earned relative to the recommended margin.

The recommended margin, literally interpreted, means “this much margin should be prepared to operate this EA,” but it is generally calculated based on the combination of the maximum number of positions held over a period and the drawdown.

Like other indicators, if you cut out during a period of good performance, it will be displayed only modestly.

Conversely, for example in the sixth lecture, “I got the Holy Grail EA but it doesn’t make money when I run it,” as we discussed,if you cut from a timing when a large drawdown is about to begin, it will look large.It’s only natural.

The ratio of how much you earned against the recommended margin isProfitability rate, so if you understand the previous discussion…

That means profitability rate also has a fairly strong element of luck…

I think you can understand that.

The calculation is simple: if an EA earned 100,000 yen so far and the recommended margin is 100,000 yen, the profitability rate will be displayed as 100%.

Because you earned 100,000 yen with a starting capital of 100,000 yen. It means you earned 100% of your capital.

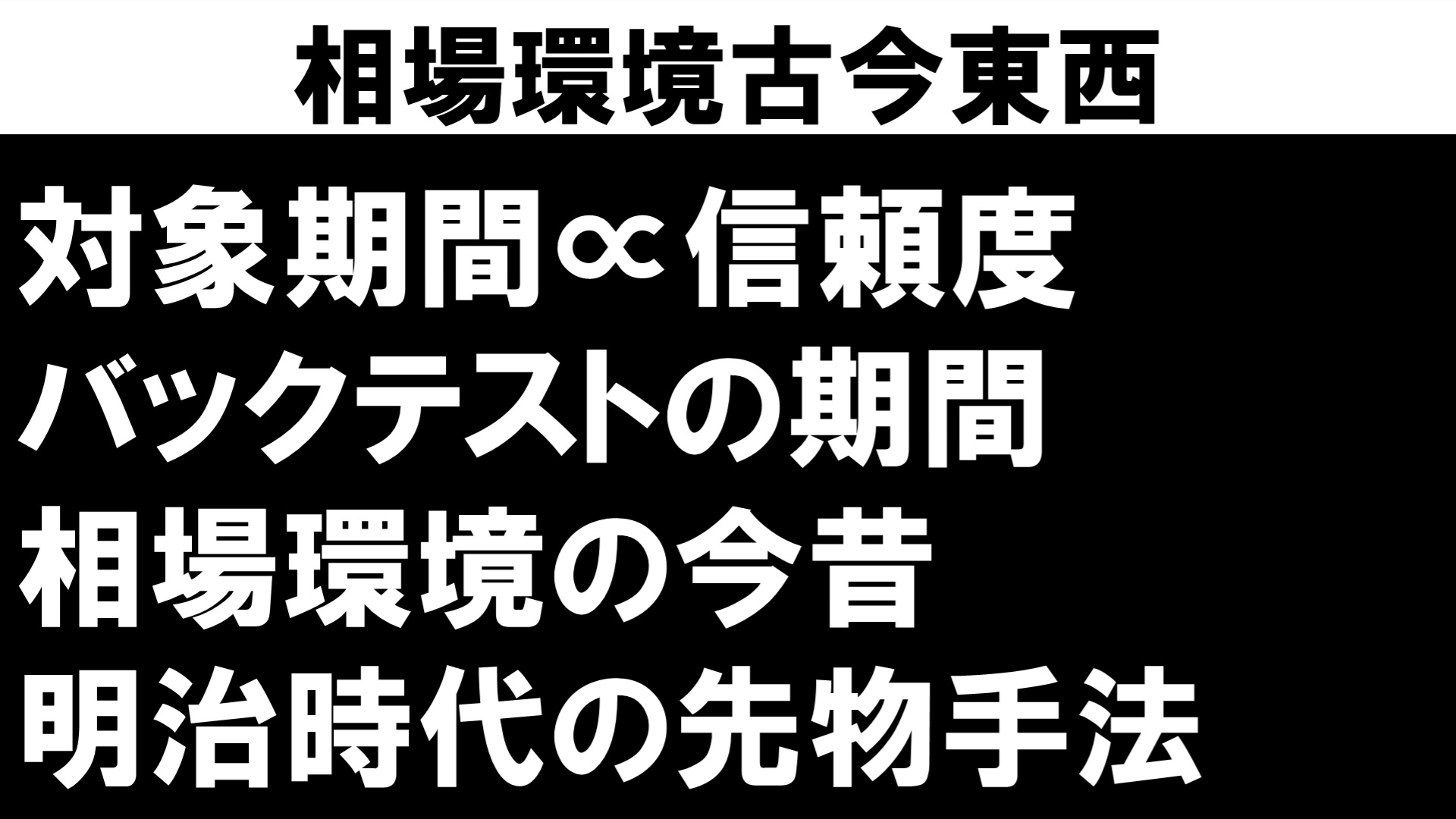

Market Environment Past and Present

If luck plays a strong role, is it completely useless as a reference? Not exactly.The element of luck is diluted as the observation period lengthens, so a profitability rate measured from backtests or forward tests of a certain length can be considered reliable.

How long should it be? There is no clear answer, but empirically, for backtests you should have at least 3 years, ideally 5 years.

As for the duration of backtests, longer is not necessarily better.

Because market conditions have changed over time.

To put it bluntly, would a staple futures trading method that earned huge profits in the Meiji era still work in today’s futures market?

Liquidity, quality of participants, trendy methods, tools, and other factors have changed, so it’s easy to imagine that the methods that work also differ…

Recently, for example, those who had been participating in the market since before the Lehman Brothers crash may have noticed that the market environment changed drastically after that event.

Firms that had worked before stopped functioning, while after the crash, somehow trading became profitable.

This led to a flood of traders like that.

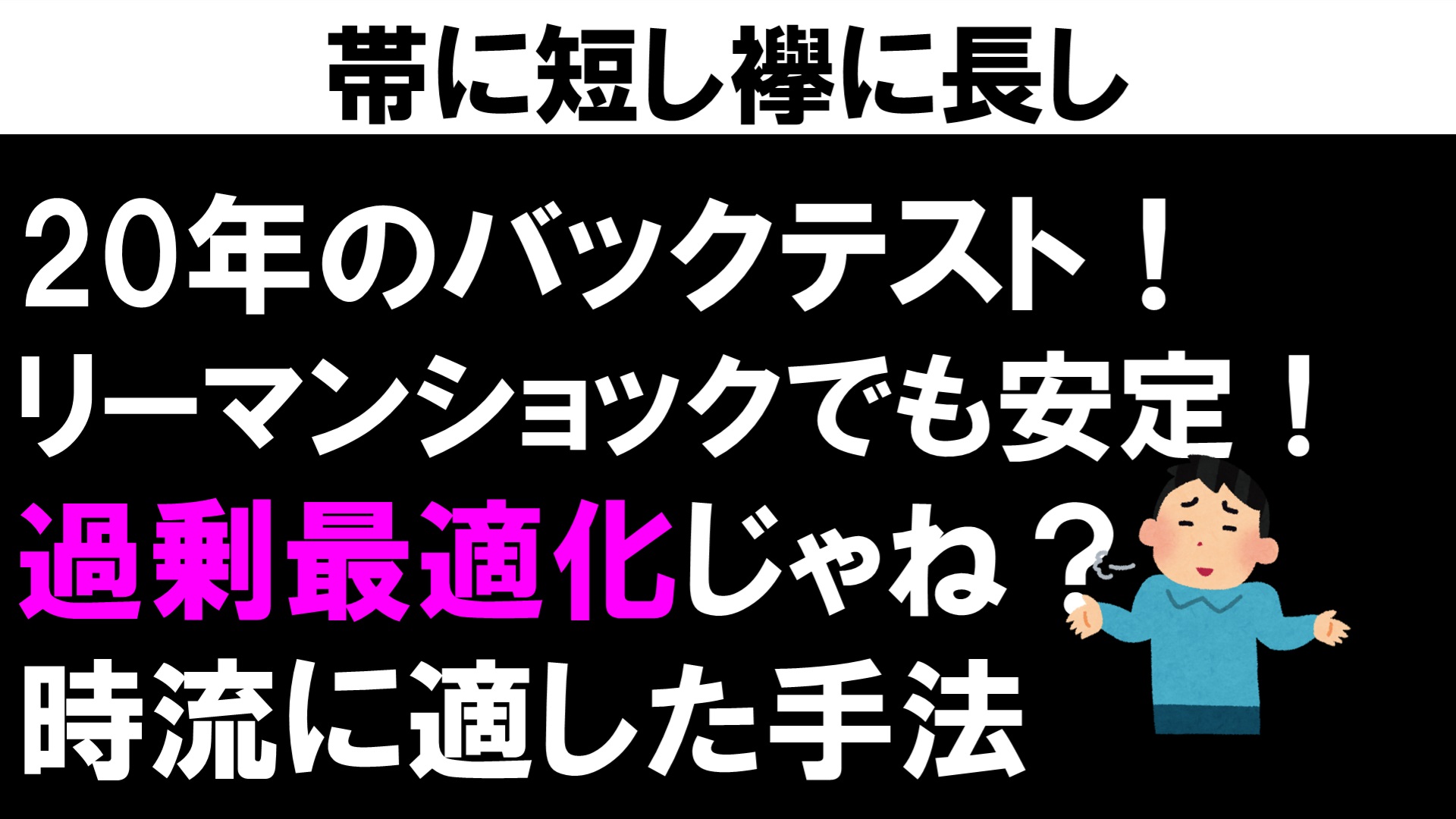

Short Sash, Long Ribbon

Back to the discussion on backtesting, in this light, it seems that…We have been backtesting for 20 years! Whether before or after the 2008 Lehman Shock, it still earns money in the same way!

That suggests a high likelihood of overfitting.

Just like the Meiji era and the present, the market environment is not identical; even if not extreme, the environment before and after Lehman differs fundamentally.

This is why “long backtest periods aren’t guaranteed better.” Short is not good, but too long is also bad.

Whether EA or discretionary trading, the ideal is to earn using a method suited to the current trend, so you need to decide your verification period with that in mind.

Considering this reduces the risk of overfitting and leads to developing a trading method based on simple, fundamental advantages.

By the way, when we say trend here, we mean price movement characteristics derived from factors such as liquidity, volatility, and the quality of participants.

■ Concept and Operational Policy of the EA I Developed

EA Artisan’s EA (Three Arrows) is here

× ![]()