3/21 FOMC passes

※Notice before entering the article content This series is free for the first month, so if you're curious, I’d be glad if you check it out for at least one month. If possible, reviews and shares would also be greatly appreciated as they boost the author's motivation.

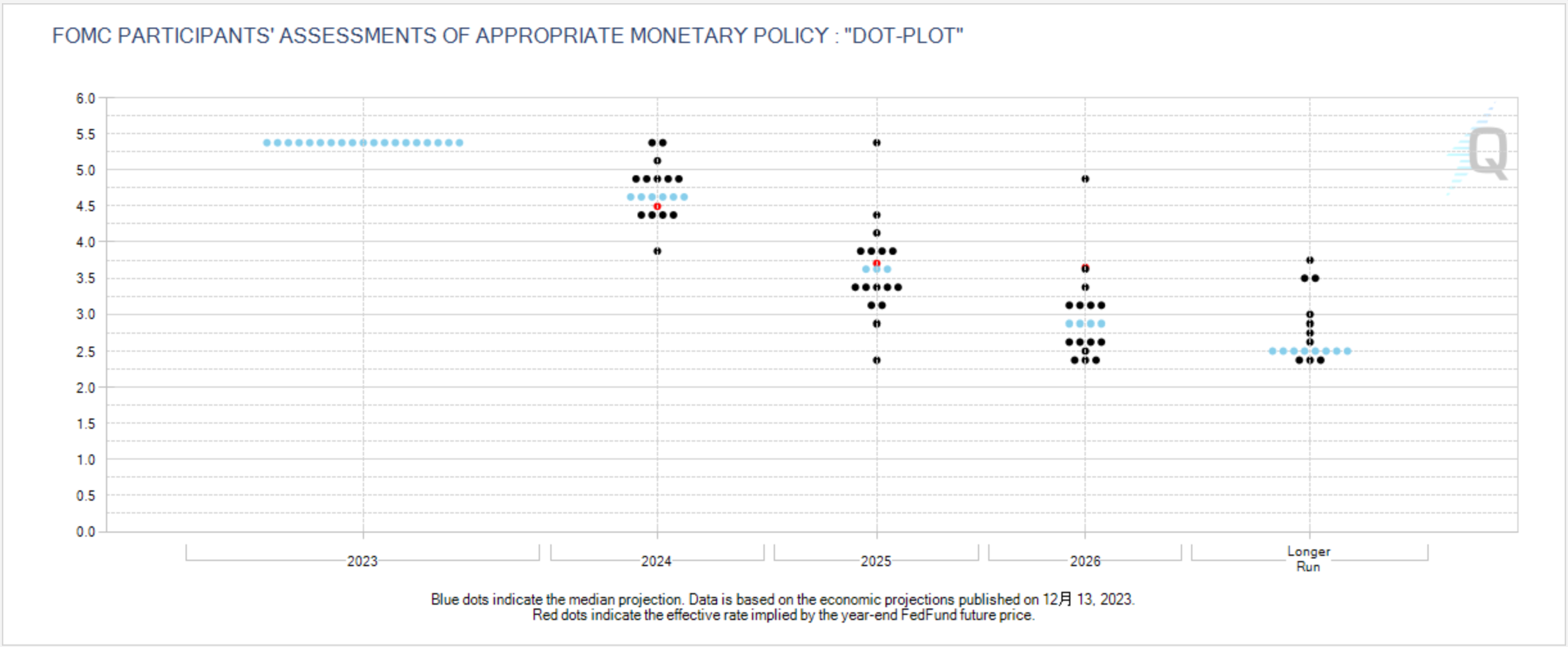

Last night’s FOMC kept the policy rate unchanged. The dot plot shows that the 2024 target is 4.6%, maintained with a 75bp rate cut, and the 2025 policy rate median is 3.9% (up from 3.6%). The long-run FF rate median rose from 2.5% to 2.6%.

● March 20 Statement

・ They will not cut rates until there is greater confidence that inflation is returning to target ・ They believe they will not cut rates until there is greater confidence that inflation will sustainably reach the 2% target.

● Powell’s Remarks

・ Inflation has eased considerably but remains too high

・ Labor demand continues to exceed labor supply

・ It is likely to begin cutting rates at some point this year, but the outlook is uncertain, and risks will continue to be watched

・ They are prepared to keep rates at a high level for a long period if needed

・ It is unlikely that commodity prices will fall sharply. The declines are expected to be gradual

・ January CPI and PCE numbers were quite high, but this may be due to seasonal adjustment

・ A significant weakening of the labor market would justify starting rate cuts

・ Inflation tends to be slightly stronger in the first half of this year

・ They expect the unemployment rate to rise

The dot plot was modestly raised for 2025 and the long term, but left unchanged for 2024, which caused a dollar sell-off as it had been anticipated to rise. Chairman Powell’s hedged, somewhat dovish remarks that inflation decline may have some seasonality contributed to the dollar’s decline. Given the presidential election and concerns about a potential recession, it seems the market avoided overly tightening rhetoric.

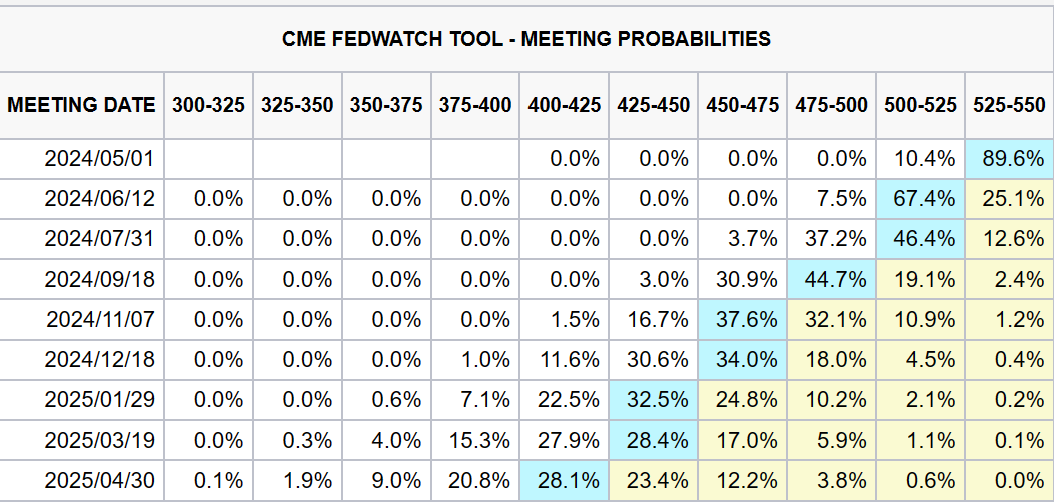

The prospect of a June rate cut remains, with the market pricing in nearly a 70% chance of a June cut.

● Economic Outlook

・ Interest rates

24: 5.1% → 4.6% → 4.6%

25: 3.9% → 3.6% → 3.9%

26: 2.9% → 2.9% → 3.1%

Long term: 2.5% → 2.5% → 2.6%

・ GDP

24: 1.5% → 1.4% → 2.1%

25: 1.8% → 1.8% → 2%

26: 1.8% → 1.9% → 2%

Long term: 1.8% → 1.8% → 1.8%

・ Unemployment rate

24: 4.1% → 4.1% → 4%

25: 4.1% → 4.1% → 4.1%

26: 4.1% → 4%

Long term: 4% → 4% → 4.1% → 4.1%

・ PCE

24: 2.5% → 2.4% → 2.4%

25: 2.2% → 2.1% → 2.2%

26: 2% → 2% → 2%

・ Core PCE

24: 2.6% → 2.4% → 2.6%

25: 2.3% → 2.2% → 2.2%

26: 2% → 2% → 2%

The core PCE and GDP were revised upward for 2024. This aligns with consensus, I think.

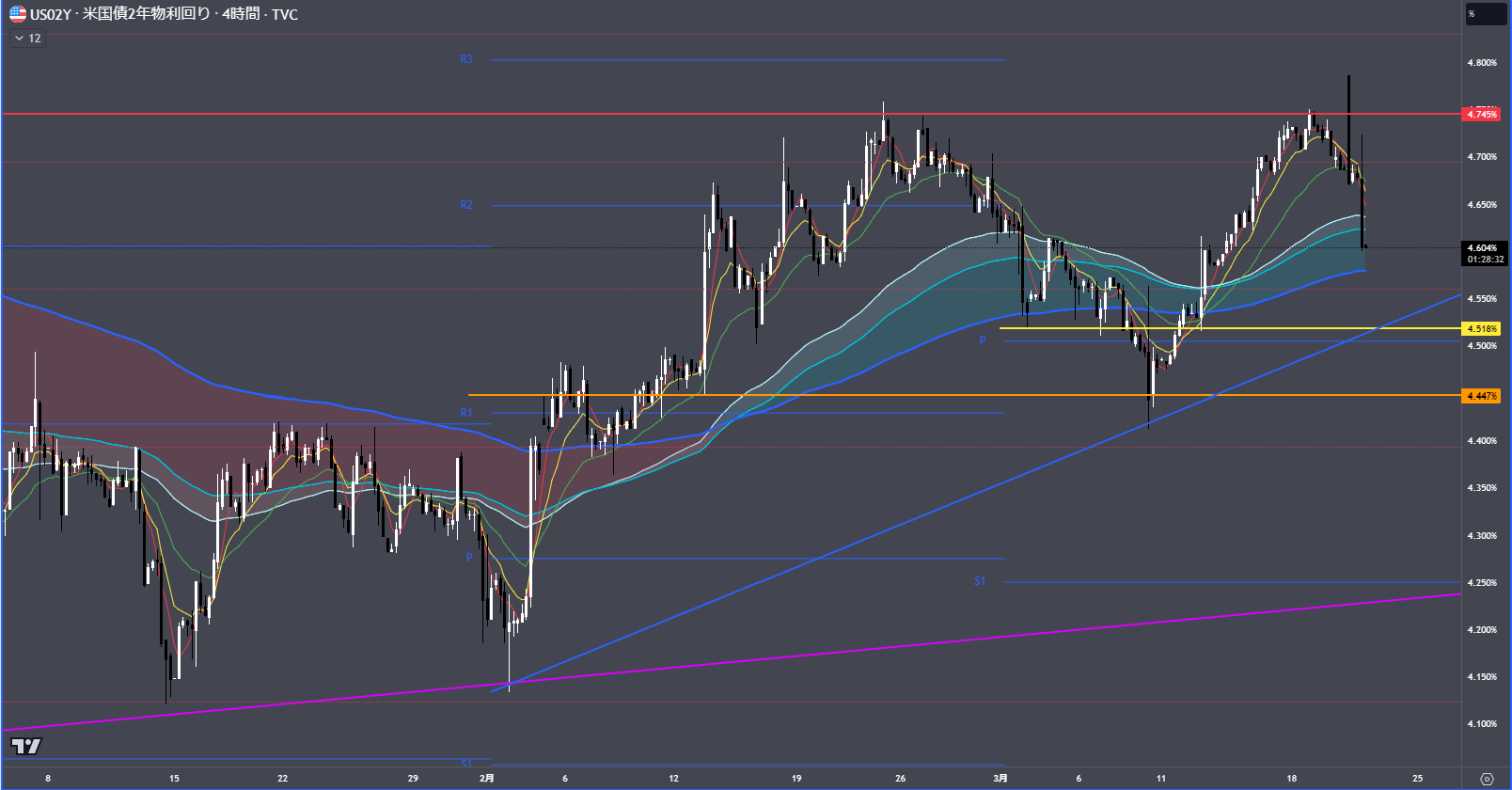

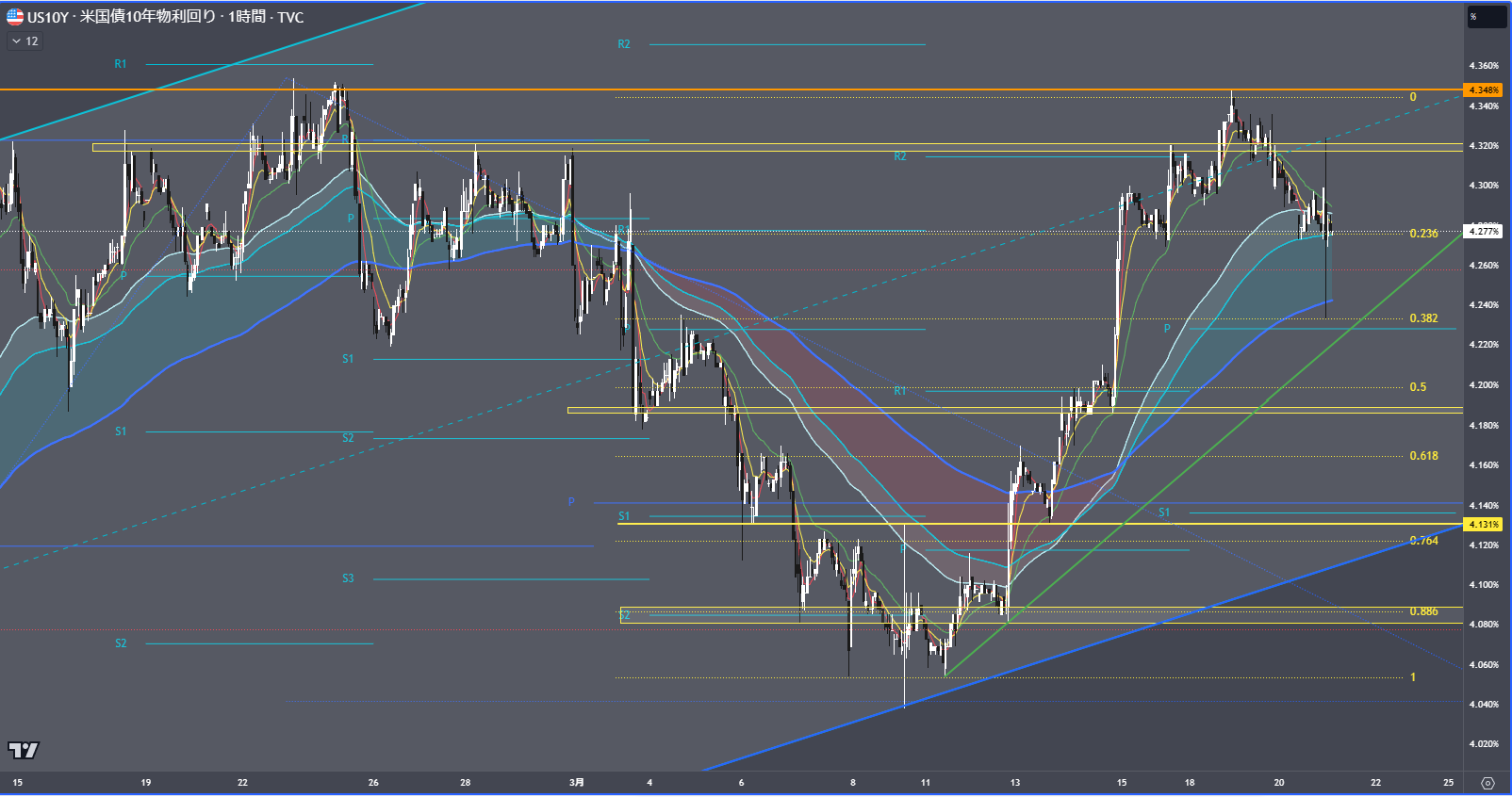

After the release, short-term rates fell, but long-term rates were hardly moved. Moving forward, the market will likely depend on inflation trends.

Today the Bank of England's Monetary Policy Committee meets. A rough preview is posted above, please check that.

3/16 A torrent of central bank week - Analyzing markets from fundamentals and technicals - Investment Navi+ - A marketplace of global trading methods and tools - GogoJungle

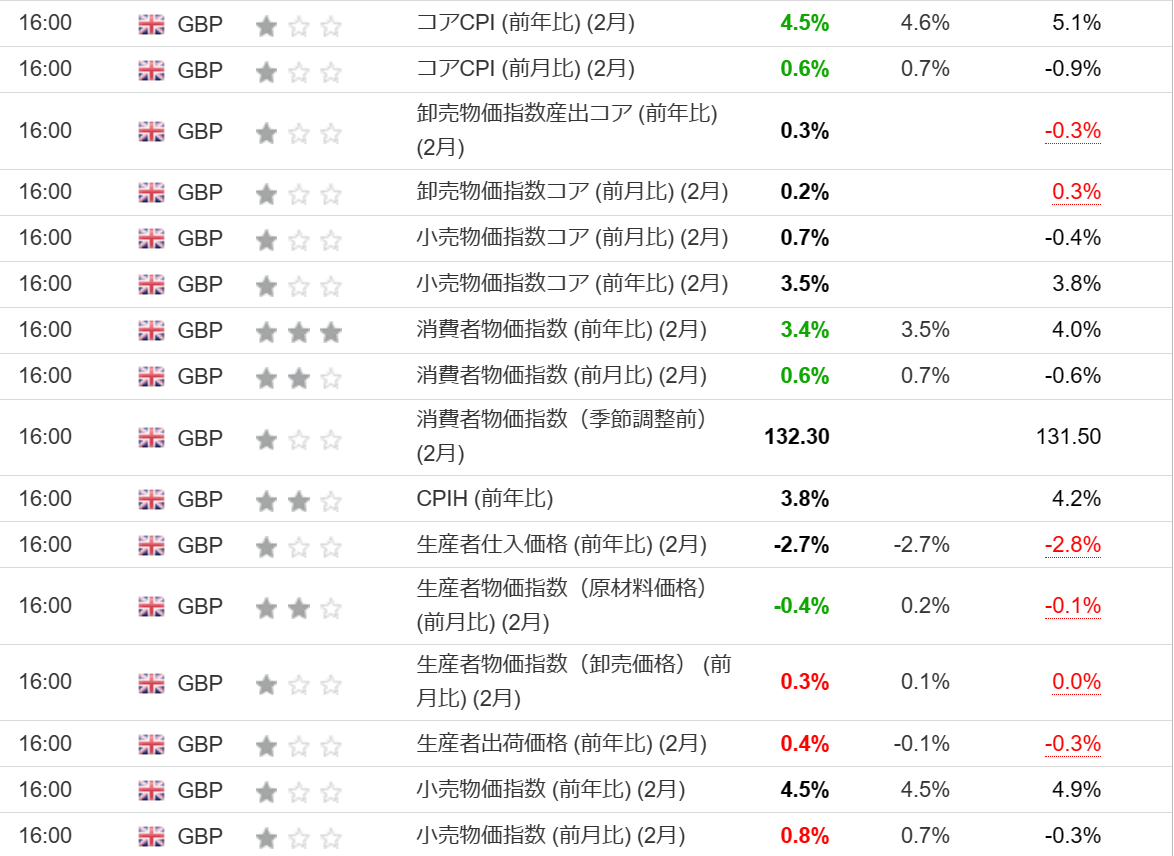

Yesterday, UK CPI fell sharply year-on-year, in line with market expectations for both headline and core. Central banks are likely meeting expectations, perhaps a bit higher than anticipated. However PPI rose due to crude oil prices, and with housing prices rising month-on-month, the result remains strong and optimism cannot be fully embraced.

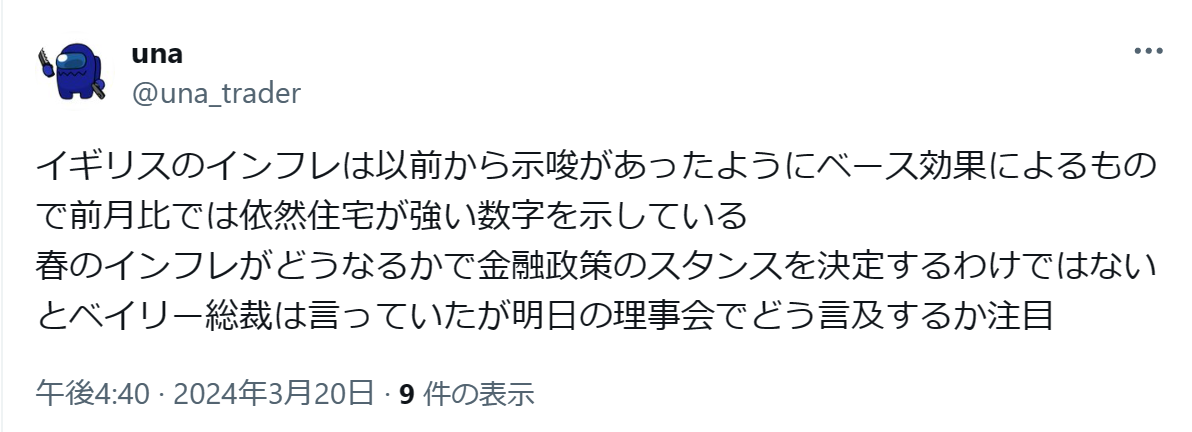

I also posted a tweet, but pay attention to whether Bailey’s language changes today.

Also, with PMI releases from various countries ahead, please pay attention to both the report content and the data. The euro area and the UK show slight improvement, but the impression is still somewhat tight.

◇ Stock Market