3/20 RBA and Bank of Japan pass-through, and FOMC

※Notice before entering the article content This serialized article is free for the first month, so if you’re curious, please take a look for at least one month. If possible, reviews and shares would also be greatly appreciated as they motivate the author.

There was a RBA announcement, but with almost no changes, stating that they need to be convinced that CPI is persistently moving toward the target, and if it can settle around the 3% target, policy may shift, but for now they are waiting to see the trend. There was no short covering and the price fell; the author could not enter.

The Bank of Japan meeting proceeded as expected with the negative interest rate removed. The main contents are as follows.

〇 Statement

・Unwinding negative interest rates

・Abandonment of YCC

・Abandonment of ETF and J-REIT

・Set the target for the guided relationship between unsecured overnight call rates at 0%–0.1%

・Gradual reduction of purchases of CP and corporate bonds, aiming to end in about one year

・Decided to purchase long-term JGBs in an 8-to-1 ratio

・Excess reserves in current accounts earn 0.1% interest (uniformly)

・If long-term interest rates rise rapidly, regardless of monthly purchase plans, will increase purchases or conduct fixed-rate or common collateral operations (QE maintained)

・Believes easing financial conditions will continue for the time being

・Quarterly plan for government bond purchases: for maturities over 3 years up to 5 years or less, four purchases per month, offer range per purchase 3500–5000 billion yen (previously 4 times 3500–7500 billion yen)

・Quarterly plan for government bond purchases: 5 to 10 years, four times a month, offer range per purchase 4000–5500 billion yen (previously 4 times 4000–9000 billion yen)

・Quarterly plan for government bond purchases: over 25 years, twice a month, offer range per purchase 500–1000 billion yen (previously twice 500–3500 billion yen)

・CPI year-on-year is likely to exceed 2% through fiscal year 2024

・Reassessing consumption expenditure and production

〇 President Kuroda remarks

・Continue roughly the same level of government bond purchases as before

・Do not expect a substantial rise in deposit or lending rates due to this policy change

・Main policy tool going forward will be short-term interest rates

・Rise in short-term rates due to policy changes will be limited to about 0.1%

・Future rate-hike path will be determined by prices and economic outlook, selecting an appropriate rate level

・If short-term rates rise, the pace will be modest based on current outlook

・Large-scale asset purchases by the BOJ have been influencing the easing financial environment

・Intend to refrain from using government bond buying operations or balance adjustments as an active monetary policy tool

・Even if rate hikes occur in the future, it will be a gradual process

・After the large-scale easing ends, will consider balance sheet reduction

・Even after this policy change, current real interest rates are well below neutral rates, indicating a clearly accommodative environment

・Based on inflation outlook, the easing monetary environment will continue for the time being

・Inflation expectations have reached a sustainably stable level

・Inflation target is within sight

・There remains distance to the 2% expected inflation rate, so maintaining the accommodative environment remains important

・Evidence of a positive wage-price cycle strengthening has been observed

・In the future, consideration of reducing government bond purchases

・The possibility of achieving the 2% price target is not 100% yet, but increasing

・Further inflation increases are expected to lead to rate hikes

・If inflation outlook overshoots or shows possibility, it could lead to changes in monetary policy

・If core inflation remains below 2%, accommodative monetary environment will continue

・If core inflation rises, the degree of easing will be reduced

They revised unconventional easing measures, but since this had already been fully priced in by leaks, there was no yen buying and easing measures continued, with yen selling accelerating. It is expected to watch wage and inflation trends for now, so there are no yen-buying catalysts for now.

Dollar/yen has reached 150, but while the BOJ still indicates easing, watch whether the Ministry of Finance may intervene verbally. If such extensive easing is followed by intervention, that would be quite extreme...

And today is the much-anticipated FOMC announcement. Please refer to the preview for the main outlook as a guide.

3/16 A whirlwind week for central banks - Market analysis from fundamentals and technicals - Investment Navi+ - A marketplace where global trading methods and tools gather - GogoJungle

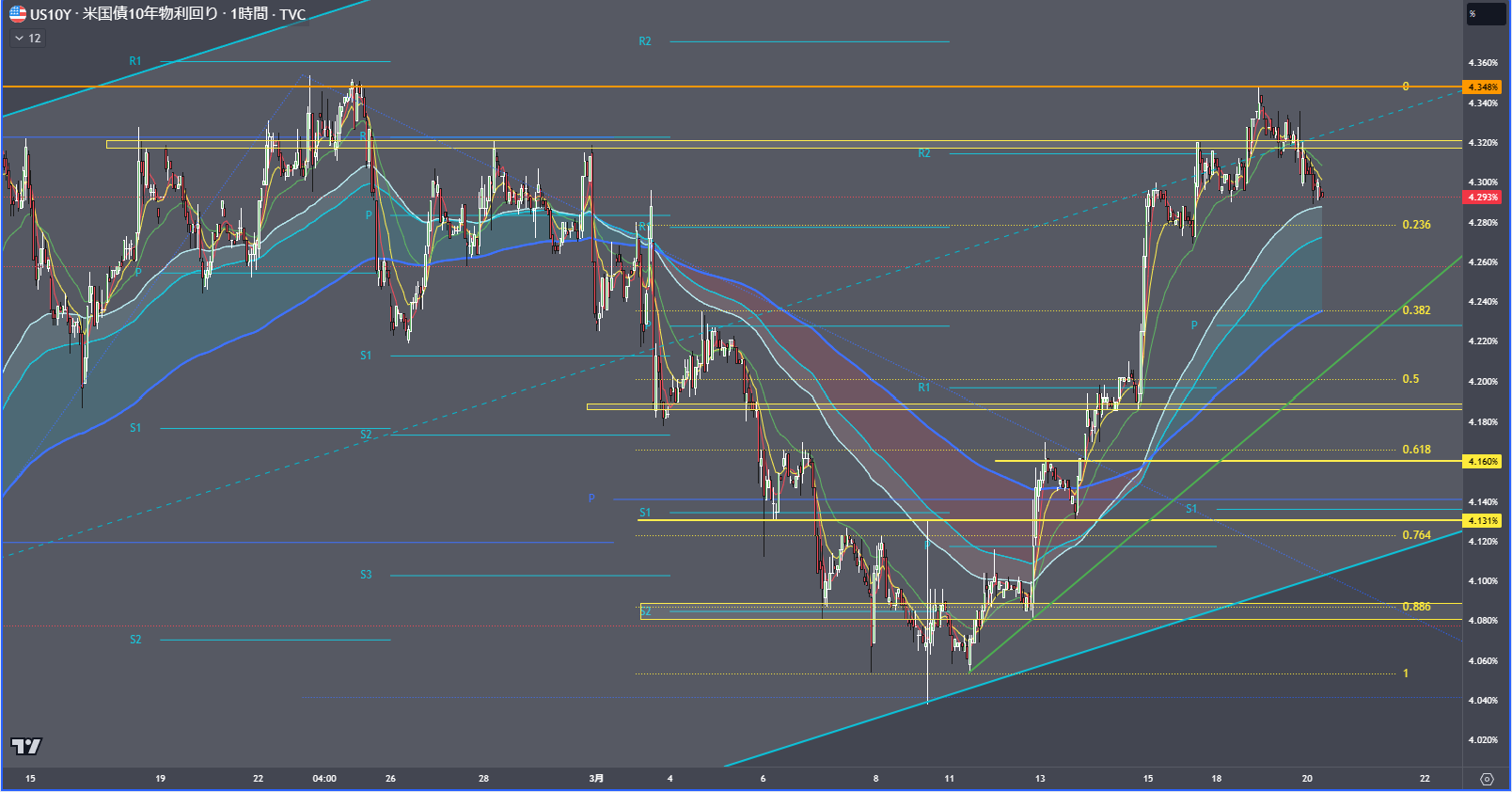

U.S. interest rates remained flat after last night’s 20-year Treasury auction performed well, so we are likely to approach FOMC at this level, and whether it moves higher depends on the dot plot.

◇ Stock market