Policy Rate, OPEC Meeting, and Employment Statistics! A Weekend Event That Will Forecast Canada’s Next Year!

This week the pound is certainly in the spotlight, but as a trading strategy it looks like only short-term trades are feasible. As for swing trading, the Canadian dollar will be in focus from today through the weekend! I’ve summarized the timing and key points to watch for the Canadian dollar’s movements.

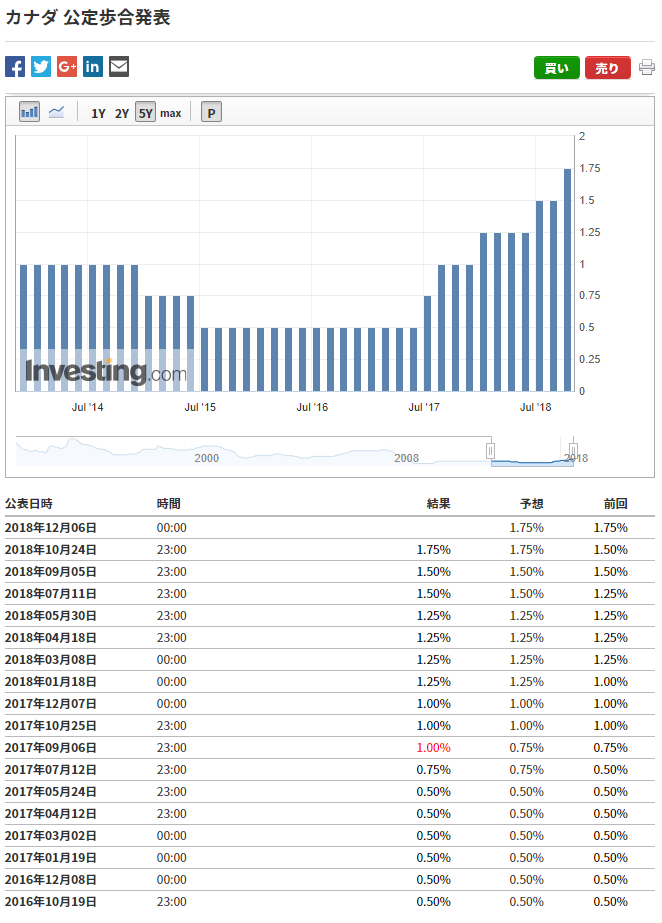

1)Bank of Canada Policy Interest Rate Announcement

At the October meeting, they raised rates and set the policy rate at 1.75%. The analysis of the accompanying statement is below. The tone is bullish, with expectations of 3 to 7 more rate hikes (2.5%–3.5%). Since the previous meeting, crude oil prices have fallen sharply, and GDP has slowed marginally.

Today the Bank of Canada will publish the policy rate decision and the statement. A hold is expected for the policy rate. Therefore the focus will be on the statement. Just like in the previous meeting, will there be a bullish tone? Also, is the outlook for the number of rate hikes still not reduced? This is worth watching. Depending on the content, it could lead to Canadian dollar selling.

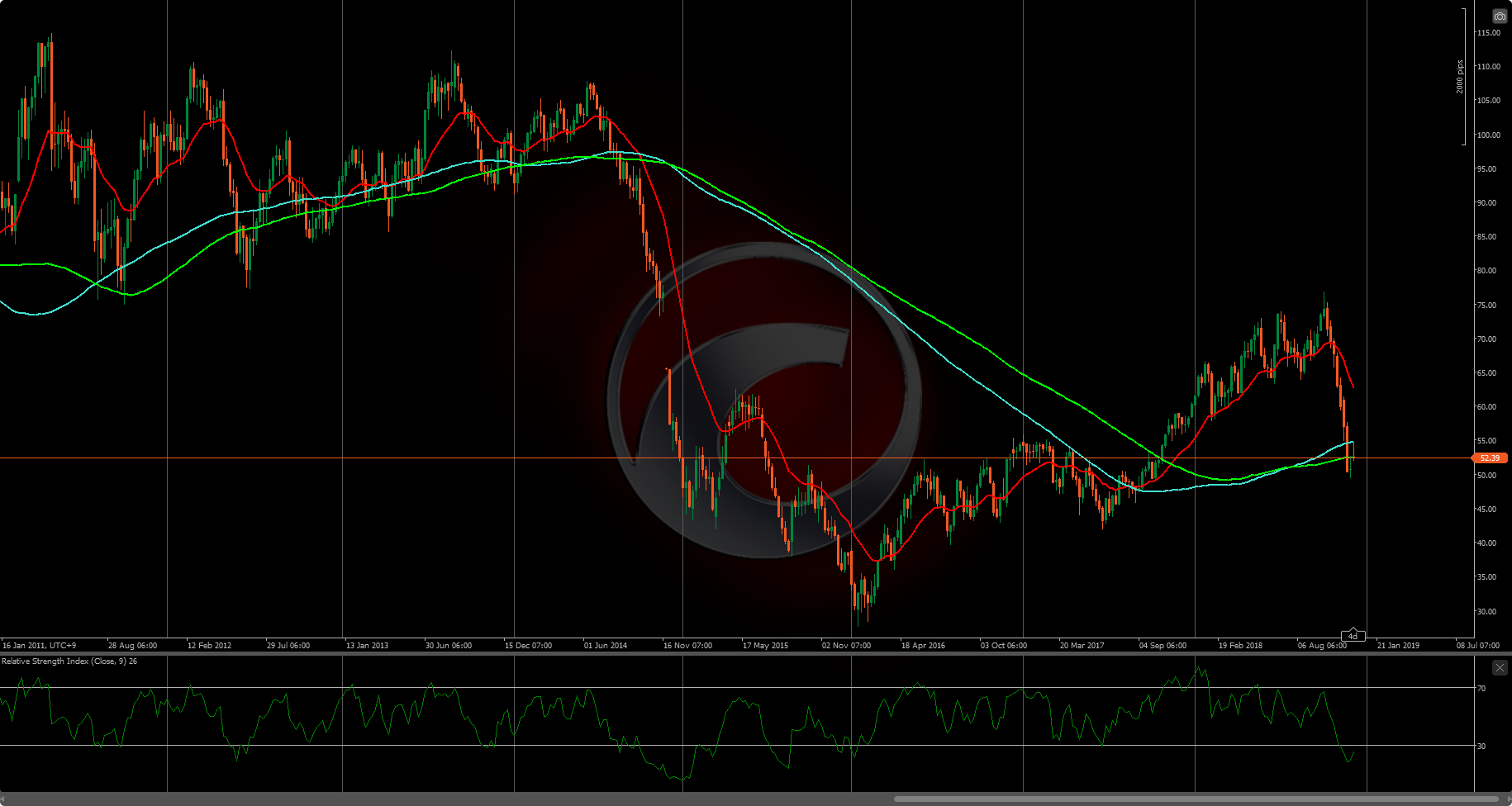

2)OPEC Meeting

Tomorrow the OPEC meeting will be held. The focus is clearly on whether a production cut agreement will be reached and the size of the cut. Crude oil prices have plunged from around $77 two months ago to about $50. Will an agreement on production cuts stop the price decline? This is something to watch.

WTI Crude Oil Price Daily Chart

WTI Crude Oil Price Weekly Chart

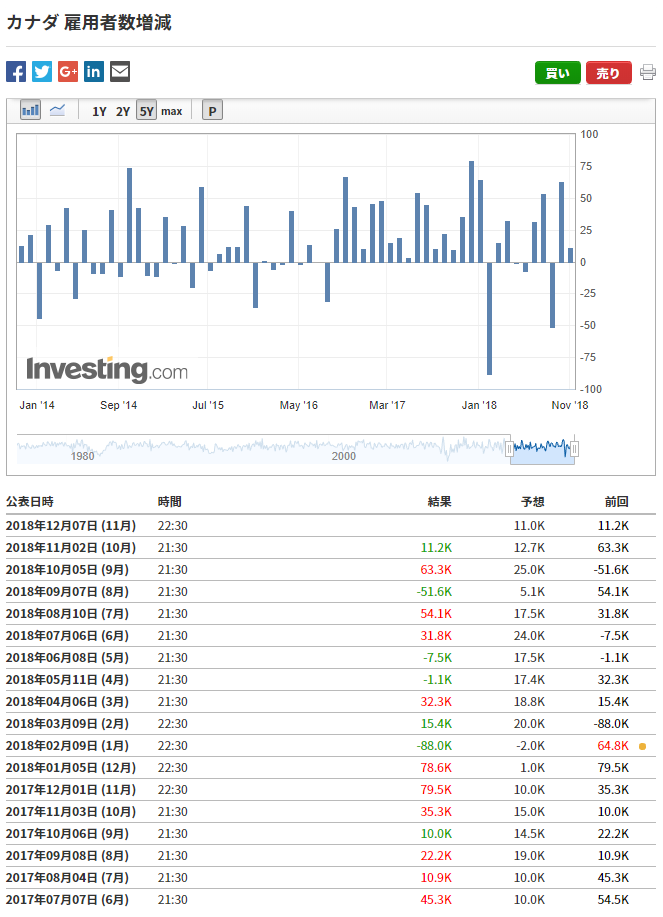

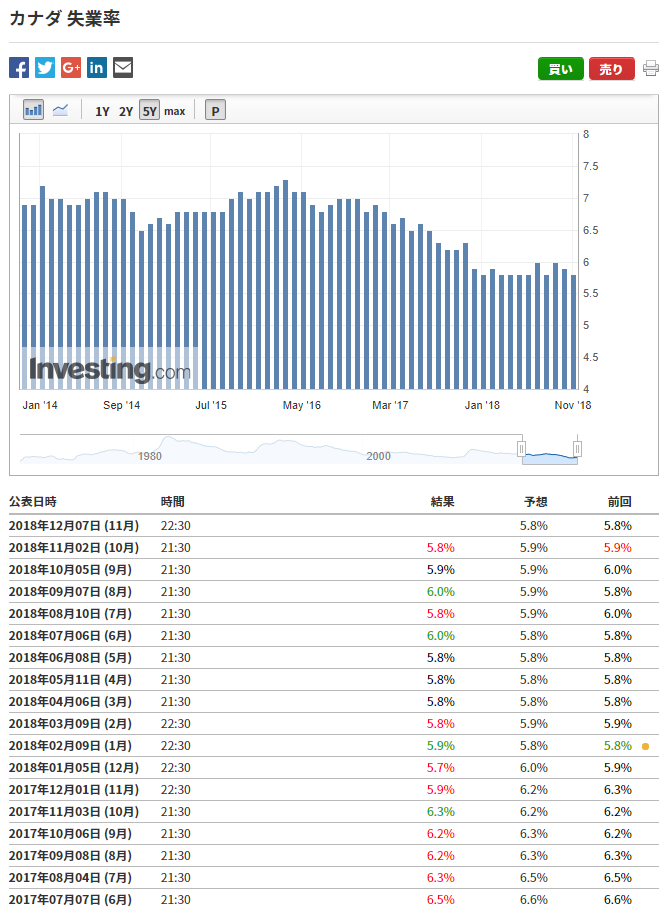

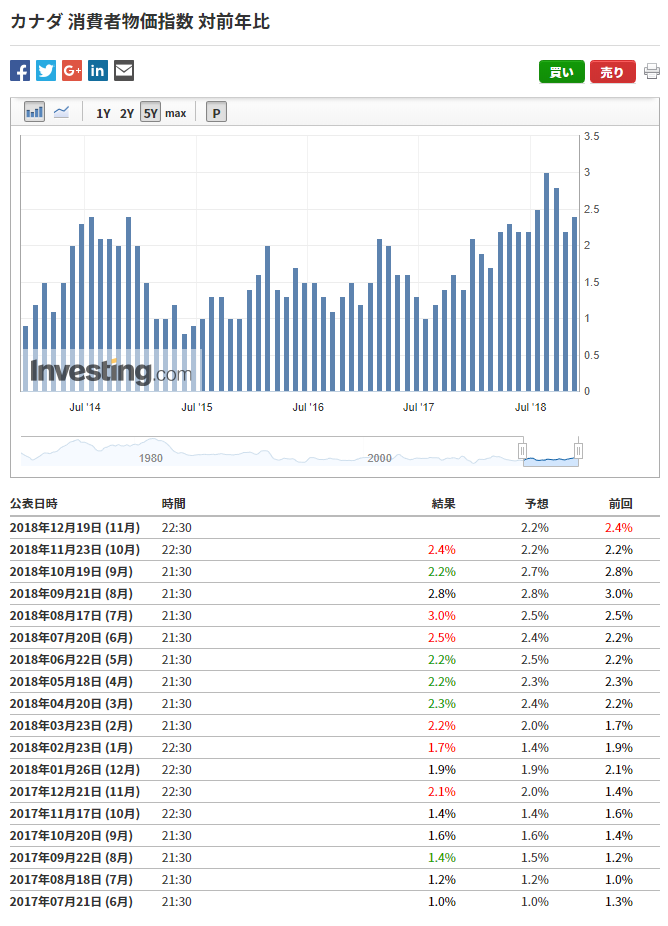

3)Canada Employment Statistics

On Friday, Canada’s employment numbers and unemployment rate will be released. The focus is on the unemployment rate. It has approached the 5% level; can it move into the lower half of the 5% range? This is being watched. It will influence the outlook for rate hikes in the coming years. We’re looking for solid figures.

Canadian Dollar Levels and Strategies

CAD/CHF Daily Chart

CAD/JPY Daily Chart

USD/CAD Daily Chart

The Canadian dollar sits in a neutral position when viewed against the Swiss franc, the yen, and the US dollar. It can move in either direction for buying or selling the CAD. Therefore, a simple strategy of following the trend is probably fine.

If the policy rate is hiked, buy CAD.

If the rate is held and the economic and rate-hike outlook is revised downward, sell CAD.

If OPEC agrees to a production cut and crude oil prices rise, buy CAD.

This seems like a good strategy to me.

If results differ, I’d prefer to take a wait-and-see approach.

October Bank of Canada Policy Rate Announcement article

On October 24, the Bank of Canada announced a 0.25 percentage point rate hike to 1.75%. This increase was widely anticipated by officials and marks the fifth hike since a rate increase began in July 2017, bringing the policy rate to its highest level in the past nine years.

The Bank cited a solid global economic outlook and the easing of North American trade policy uncertainty due to the USMCA agreement as factors for the rate hike. However, it also noted that US-China trade tensions weigh on global growth and commodity prices. Regarding business investment and exports, the outlook was revised higher to reflect USMCA and LNG Canada’s final investment decision in British Columbia, but downwards pressure remained due to recent declines in commodity prices and the reduced competitiveness from US tax reforms. The Bank said it will continue to monitor these developments. Household spending was expected to remain supported by income growth, even as it adjusts with higher interest rates and housing-market policy.

The Bank of Canada projected 2018 growth of 2.1% and 2020 growth of 1.9%, and inflation is expected to return to the 2.0% target by the end of 2020 after temporary spikes from gas prices and minimum wage. The central bank indicated it would raise the policy rate to the neutral range of 2.5–3.5% to reach the target.

Benjamin Reitz, an economist at Scotiabank, commented, “Considering the lowest neutral rate is 2.5%, it’s clear the central bank would like to see a few more hikes. We at Scotiabank forecast three hikes in 2019—in January, April, and July.” (Montréal Bank Economic Analysis Report, October 24).