3/16 The Thunderous Midfield Bank Week

※ Notice before entering the article content This serialized article is free for the first month, so if you're curious, I would be happy if you check it out for just one month. It also helps my motivation if you spread it around. This week is expected to be very busy with many important events. Here is the main schedule.

□ Tuesday NVIDIA keynote Australian RBA meeting Bank of Japan meeting

□ Wednesday UK CPI & PPI FOMC

□ Thursday PMI from various countries BOE Monetary Policy Committee

□ Friday Nationwide CPI in Japan

Midweek is quite packed. Also, although I won’t touch on it, Turkey and Switzerland policy rate announcements are scheduled on Thursday, and Mexico's policy rate announcement is expected early Friday morning. The Swiss National Bank announcement may have a slight impact on the euro, so it would be prudent to be cautious.

First, Tuesday’s RBA and the BoJ should be watched. The RBA is highly likely to hold rates. Governor Lowe has indicated that if consumption slows faster than expected, there could be a rate cut, but for now there seems to be no need for concern. Market pricing already embeds the start of rate cuts in September or November. Inflation is largely close to the central bank's forecasts, so rate hikes are unlikely.

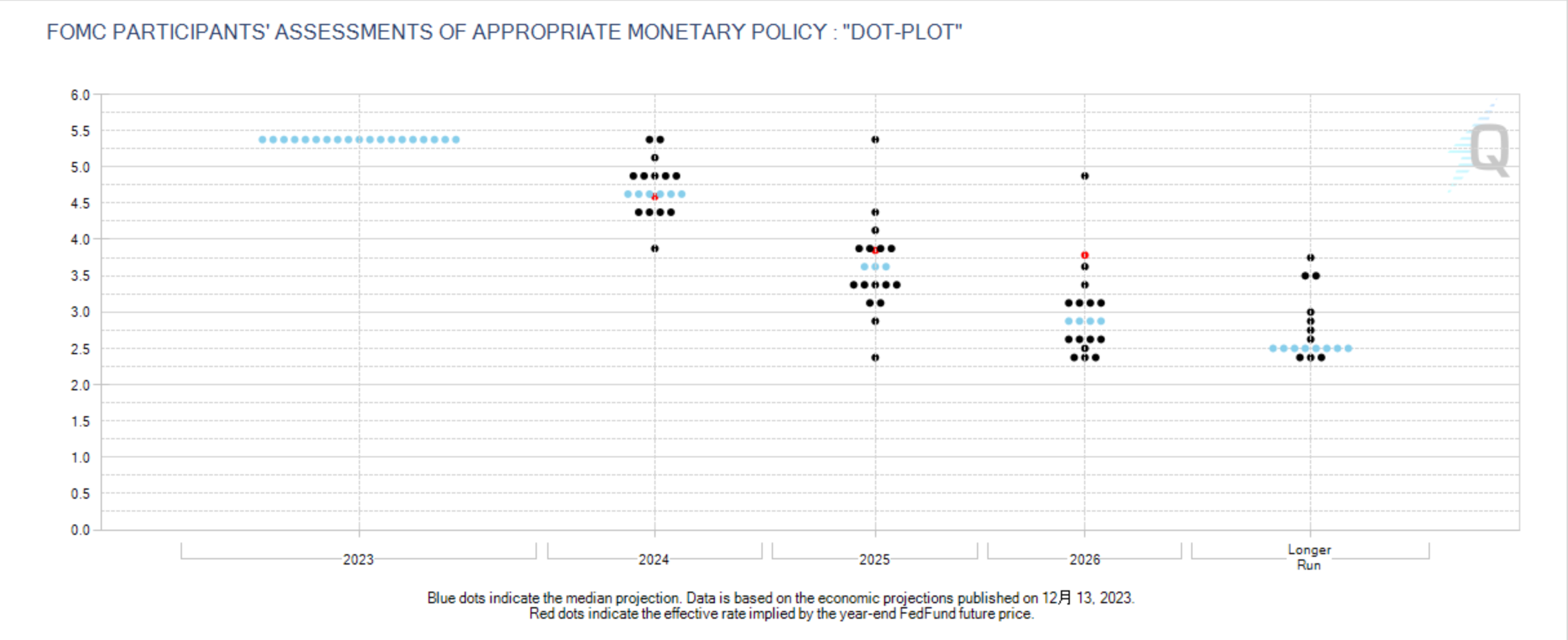

The BoJ is also likely to have already priced in a negative rate exemption, so a major yen rally seems unlikely. Even if they don’t act this month, a解除 is almost certain by April, so no major issues. The important part is normalization of easing. How much they change YCC adjustments or abolish, stop ETF purchases, and alter the framework of tightening will be key. Whether these changes happen all at once or in steps is a question. Easing policy will continue, but the remaining question is how much to raise rates after removing negative rates; consensus currently expects up to 0.25% higher. It is likely to be contained between 0.1% and 0.25%, but anything beyond that would be a surprise, so watch Governor Ueda’s press conference carefully. The FOMC, since the last mile of inflation is far away, will maintain rates for now as a policy pivot is not feasible. At the same time, economic projections will be released, and inflation forecasts are likely to be revised upwards slightly. There will also be a dot-plot release; last time the median was 4.6% with three rate cuts. If the median shifts only because two participants raise their dots, the focus will be high. It is expected that the number of cuts will decrease from three to two participants.

The longer-run neutral rate could also be revised upward from 2.5%, which could push the dollar higher if the Fed signals moving the neutral rate toward 3%. The March discussions on shrinking the balance sheet are likely to be touched upon, as Powell had referenced it before; if not announced at this meeting, it will probably appear in the minutes.

The BoE Monetary Policy Committee is unlikely to change policy rates either. Wages are falling, though the pace remains slow. Inflation, as Bailey indicated, is expected to temporarily drop to 3% in March and to around 2% by Q2 due to base effects, but this does not influence monetary policy. Even if it falls to 2%, it is expected to rise slowly again. A pivot seems unlikely until wages approach the 4% range. The market consensus for the start of rate cuts is currently Q3. In terms of the vote distribution at the last decision, two members voted for a 25bp hike (Hasker, Mann), six held (Bailey, Green, Broadbent, Pill, Ramsden), and one voted for a rate cut (Dingell). Dingell has consistently voted for rate cuts, so the vote is expected to remain with the hawks Haskel and Mann.

Regarding market moves, the Australian dollar is not likely to move much and will stay within a range; yen weakness and U.S. dollar strength, along with pound buying, will be the main directions.

U.S. interest rates have surged to 4.3%. If the scenario described above plays out, there may be room for a rise to 4.5%.

Sequencing notes aside, seasonal charts look very similar to the current situation. While fundamentals suggest not to rely on seasonality, with the presidential election and potential questions about rate cuts during congressional testimony, political pressure could arise. If this scenario occurs without changes to the dot plot, a sharp drop could be inevitable. The main scenario is as first stated, but it’s worth considering the possibility.

◇ Equity Market

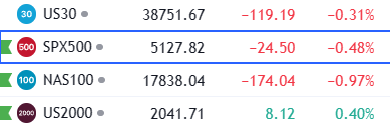

First, U.S. rates rising suggest rate cuts may be delayed, so equities are down, but sentiment hasn’t necessarily worsened markedly.

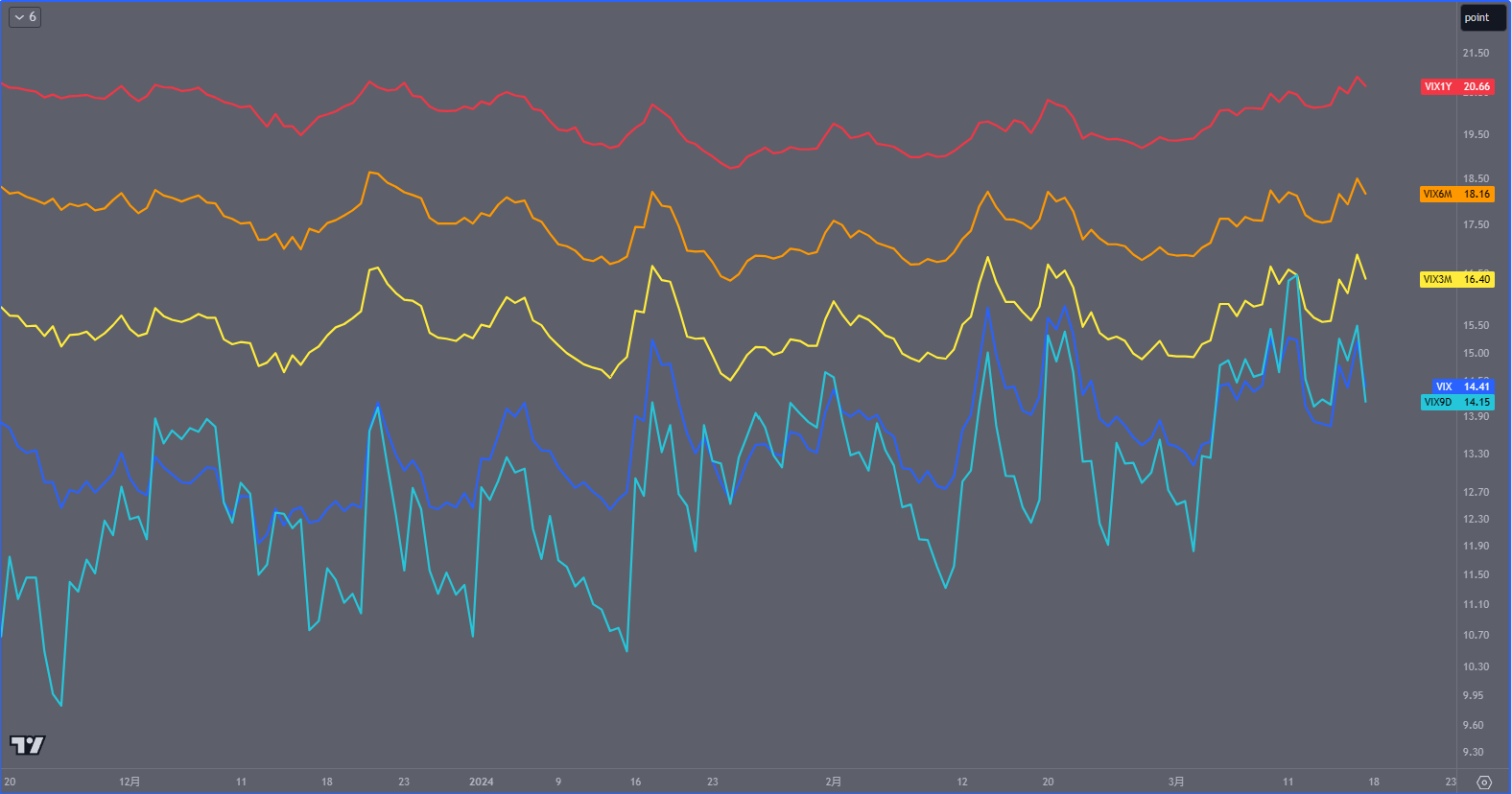

VIX stays below 16.

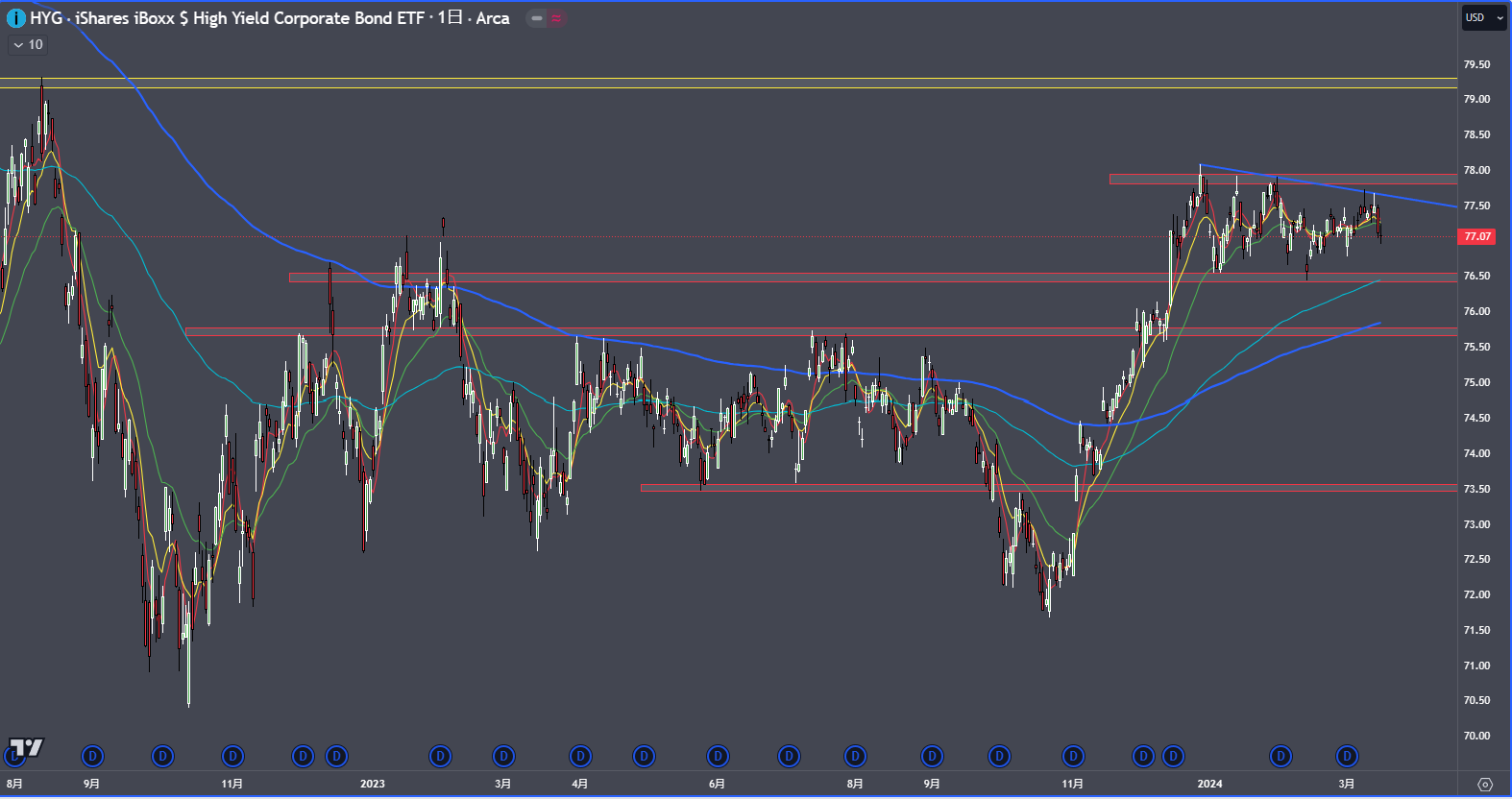

High-yield bonds remain elevated.

VIX across all tenors is stable (longer-term VIX tends to be higher; when there is recent risk, short-term VIX may overtake longer-term VIX). Therefore, near-term volatility risk is low.

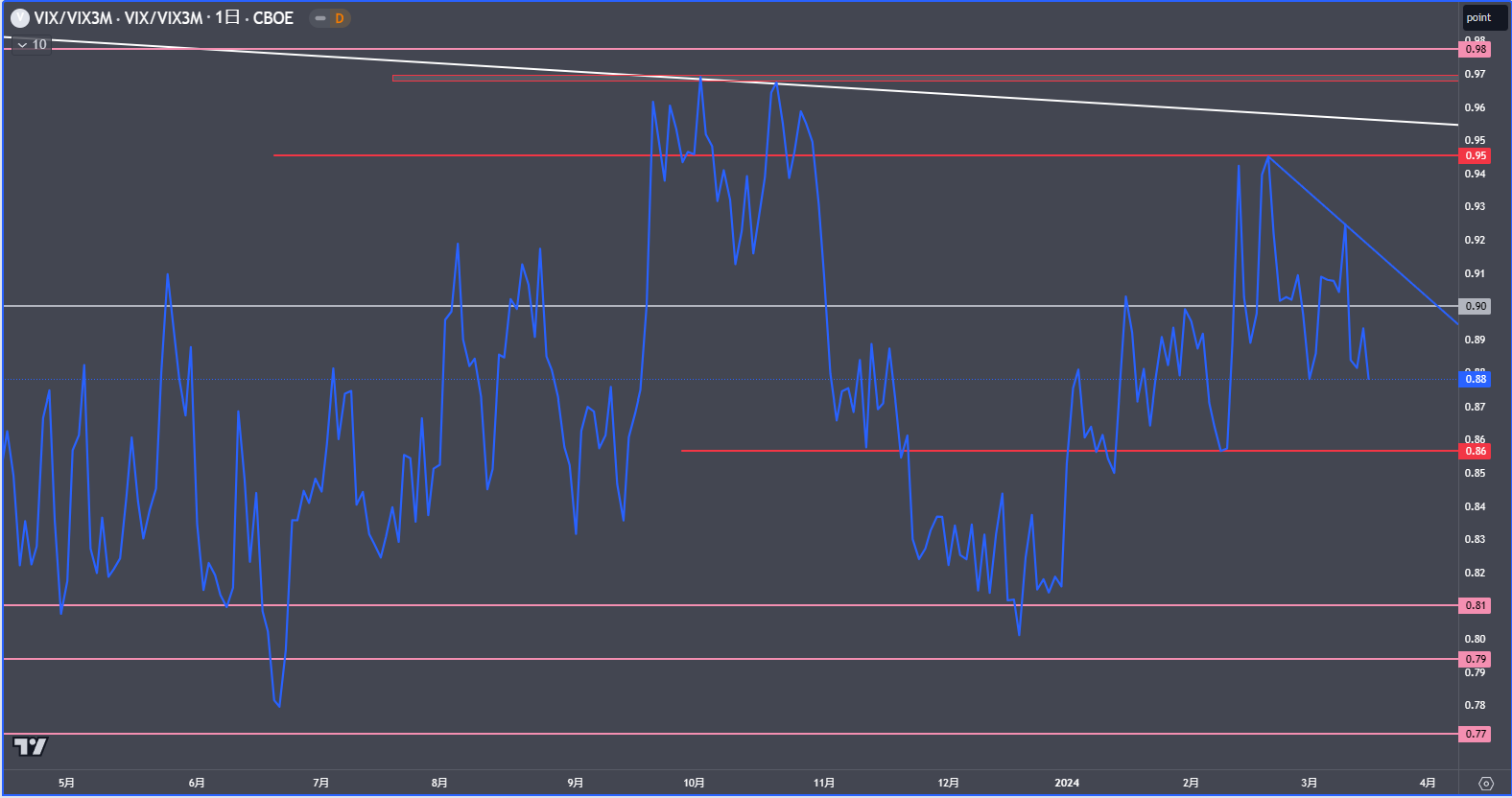

The VIX/VIX3M ratio also shows similar risk concerns are low.

Unless this area breaks, I think it’s reasonable to buy U.S. stocks on dips as part of a rebound.

Big tech remains in a slump, but excluding Tesla, others appear to be within the range of a correction. Ahead of the FOMC and with U.S. rates surging, allocations keep moving.

Even though major U.S. stock indices are down, the Russell 2000 is resisting declines, which can be read as resilience.

If talking short-term, volatility should not accelerate much right before the FOMC as rates are at a key level. A notable upcoming factor is NVIDIA’s keynote early Tuesday before the FOMC.

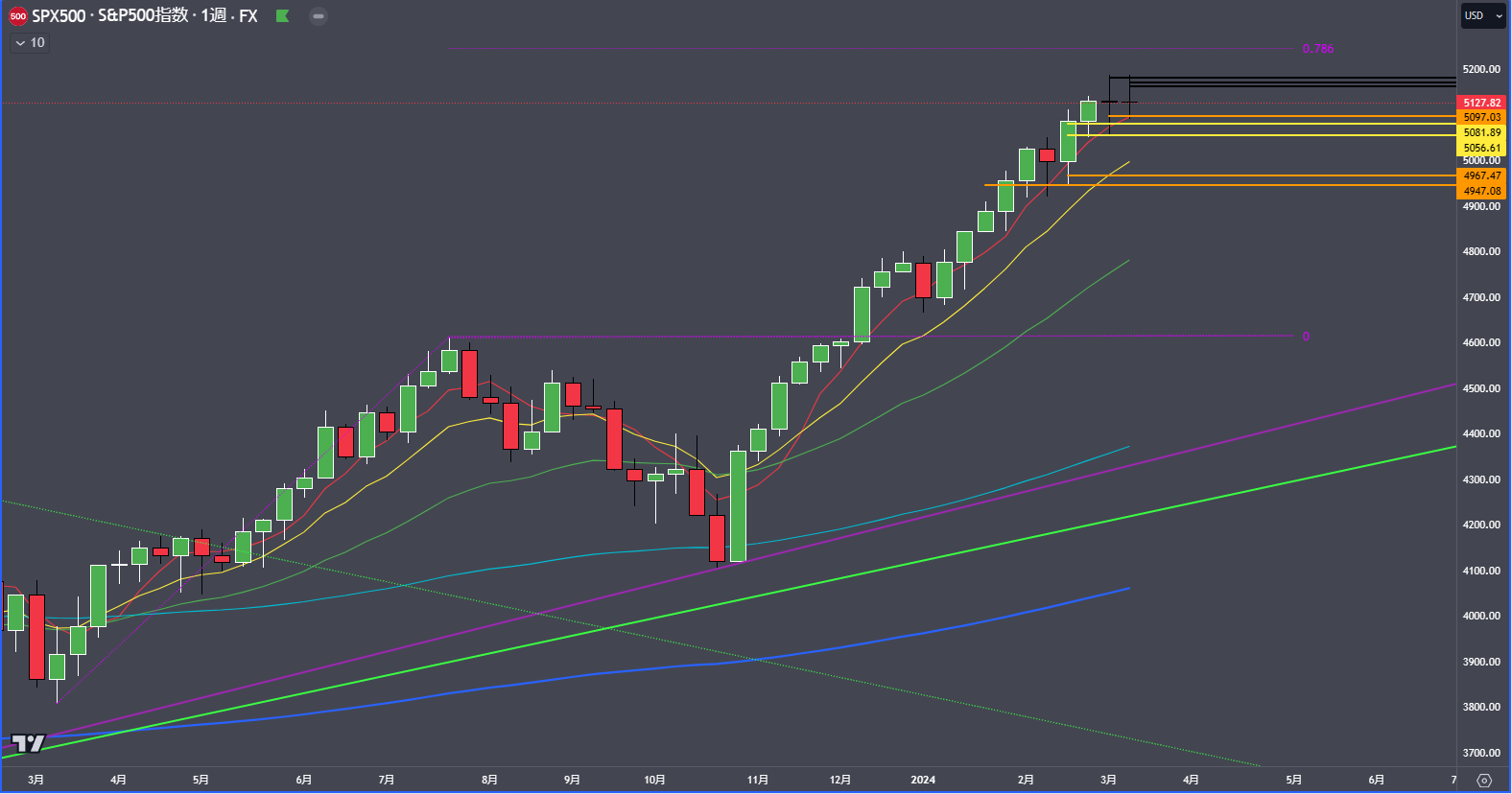

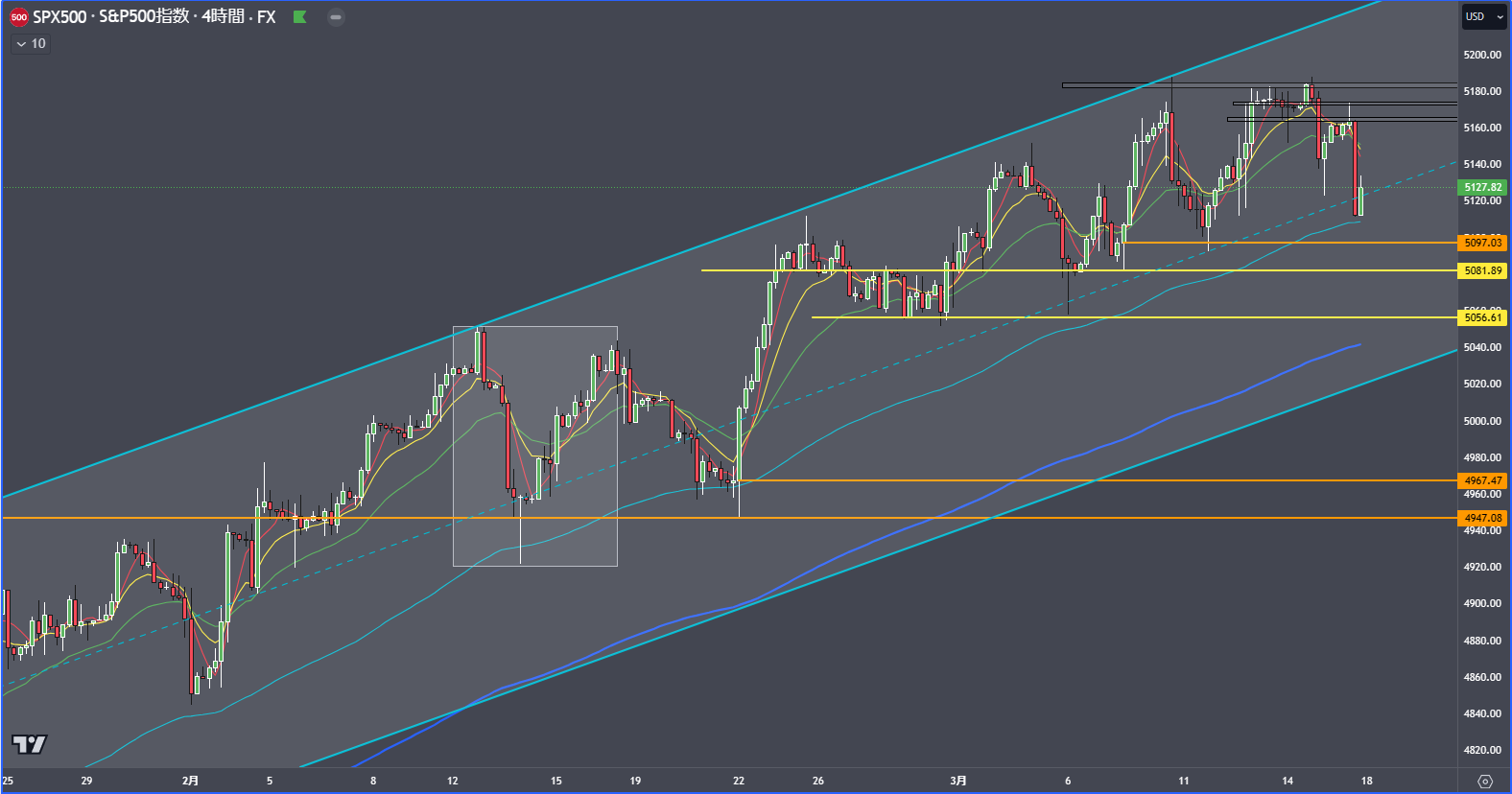

S&P500 weekly chart has closed with two consecutive crosses. This can be seen as a pullback/winding-down signal.

Support levels are at 5100, 5080, and 5060; breaking 5050 would make buying less attractive, so I’d look to add on price action around those levels.

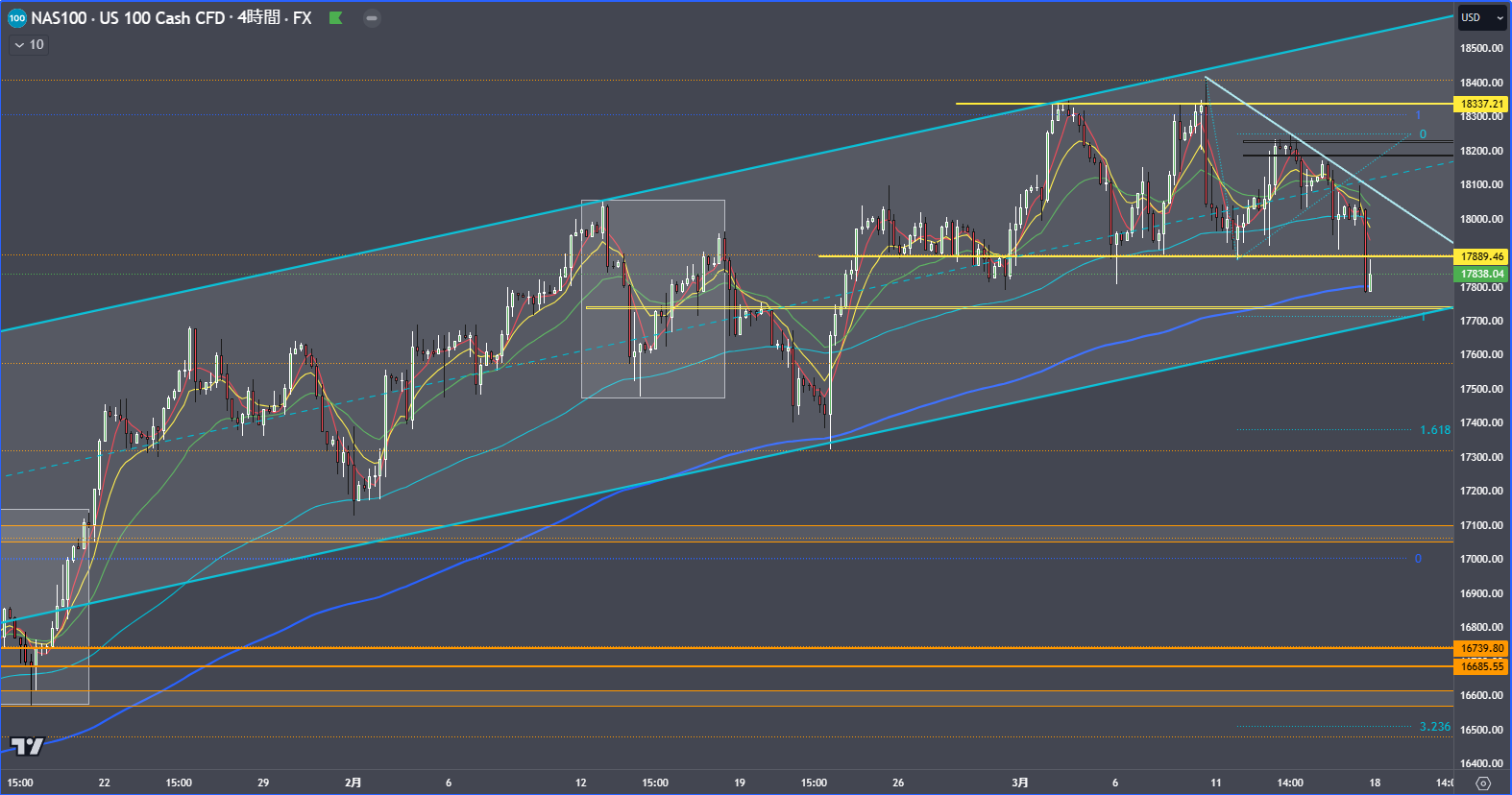

I bought NASDAQ-100 at 17900 with Friday’s trade, but it broke, so I cut losses for now. Tech leaders are heavy; NVIDIA could drive moves, but S&P500 might be more durable and carry less risk.

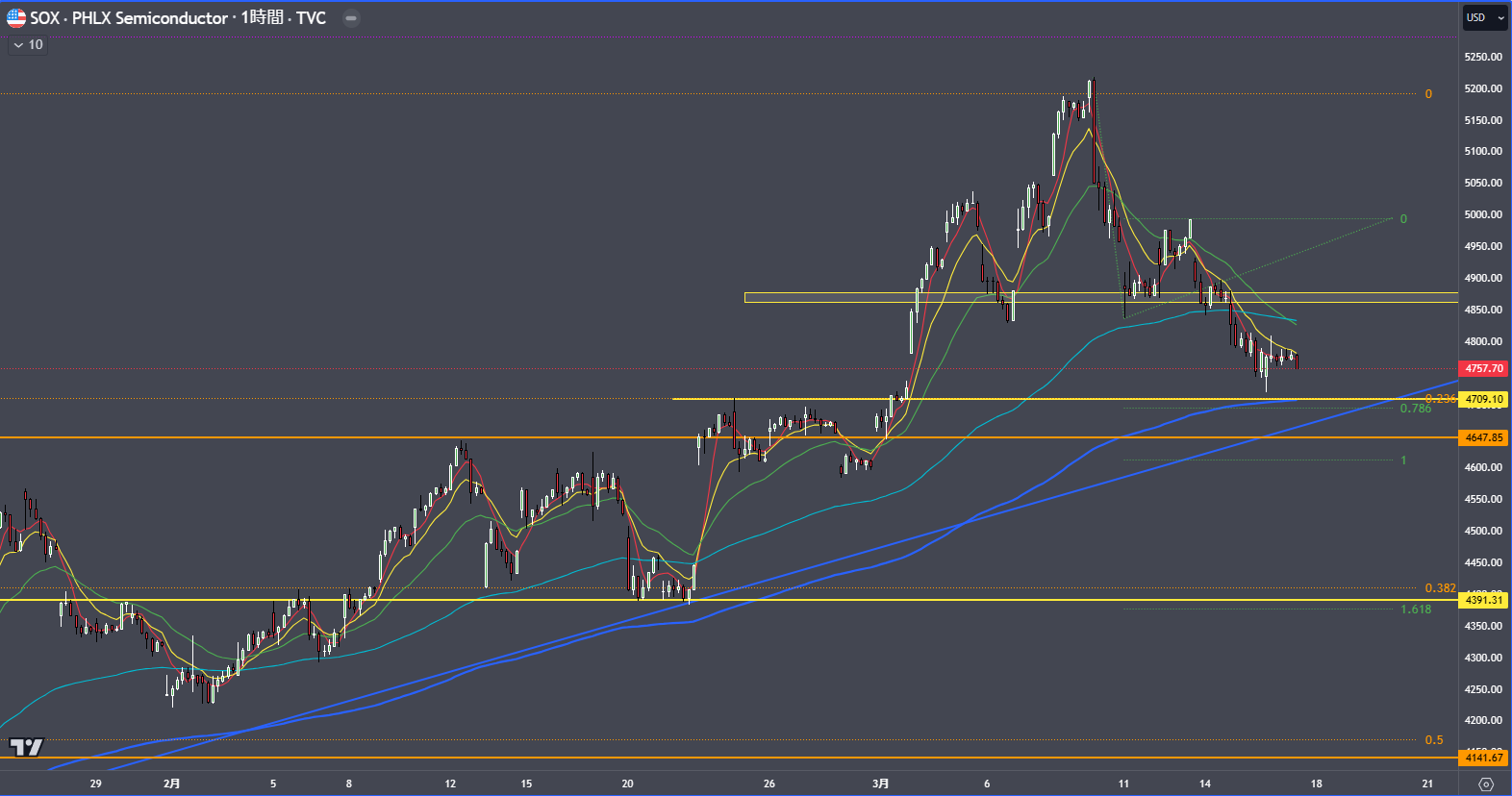

SOX index has heavy resistance around 4709, expecting a move up to that level.

Nikkei stock average is holding up better due to BOJ policy adjustments and weaker yen, relative to U.S. stocks.

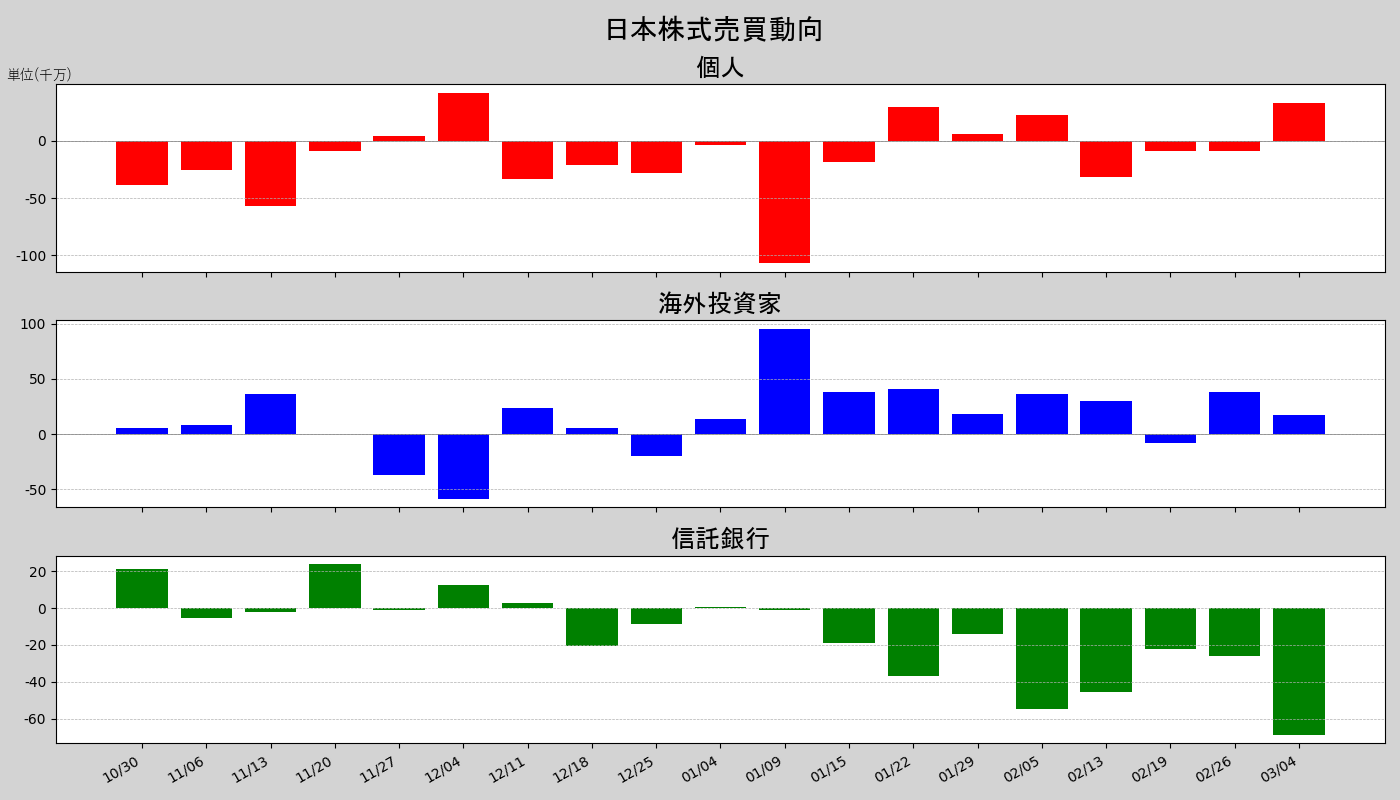

The recent decline is likely due to news about removing negative rates and GPIF selling (trust banks are outsourced by GPIF). The 40,000 level is a psychological barrier, and with the Bank of Japan’s negative rate removal potentially in play and year-end rebalancing, this looks like a rebalance scenario.

Meanwhile, foreign investors and dealers have been net buyers, and sentiment remains positive. The impact of negative rate removal is expected to be limited, so buying is reasonable.

The market is currently around the range center, awaiting a pullback toward around 38,400.

The Dow-Nikkei spread is capped by the channel upper bound, with a neck-line and short-term E-calculation overlap suggesting a rebound to around 120 could be expected, so I’d anticipate a pullback to that range.

The U.S.-dollar-denominated Nikkei is rebounding from the channel lower bound. If it breaks the short-term downtrend line and steadies, it would be easier to buy.

◇ Commodity Markets

In considering oil trends, Israel’s invasion of Rafah will be crucial. Allies are calling for a ceasefire, but the prime minister has not indicated acceptance.

Israel prepares for Rafah civilian “evacuation” — Prime Minister approves plan - Bloomberg

After Hamas submits its response, Israel’s delegation decided to head to Doha for further negotiations on hostage trade, but negotiations are likely to be protracted.

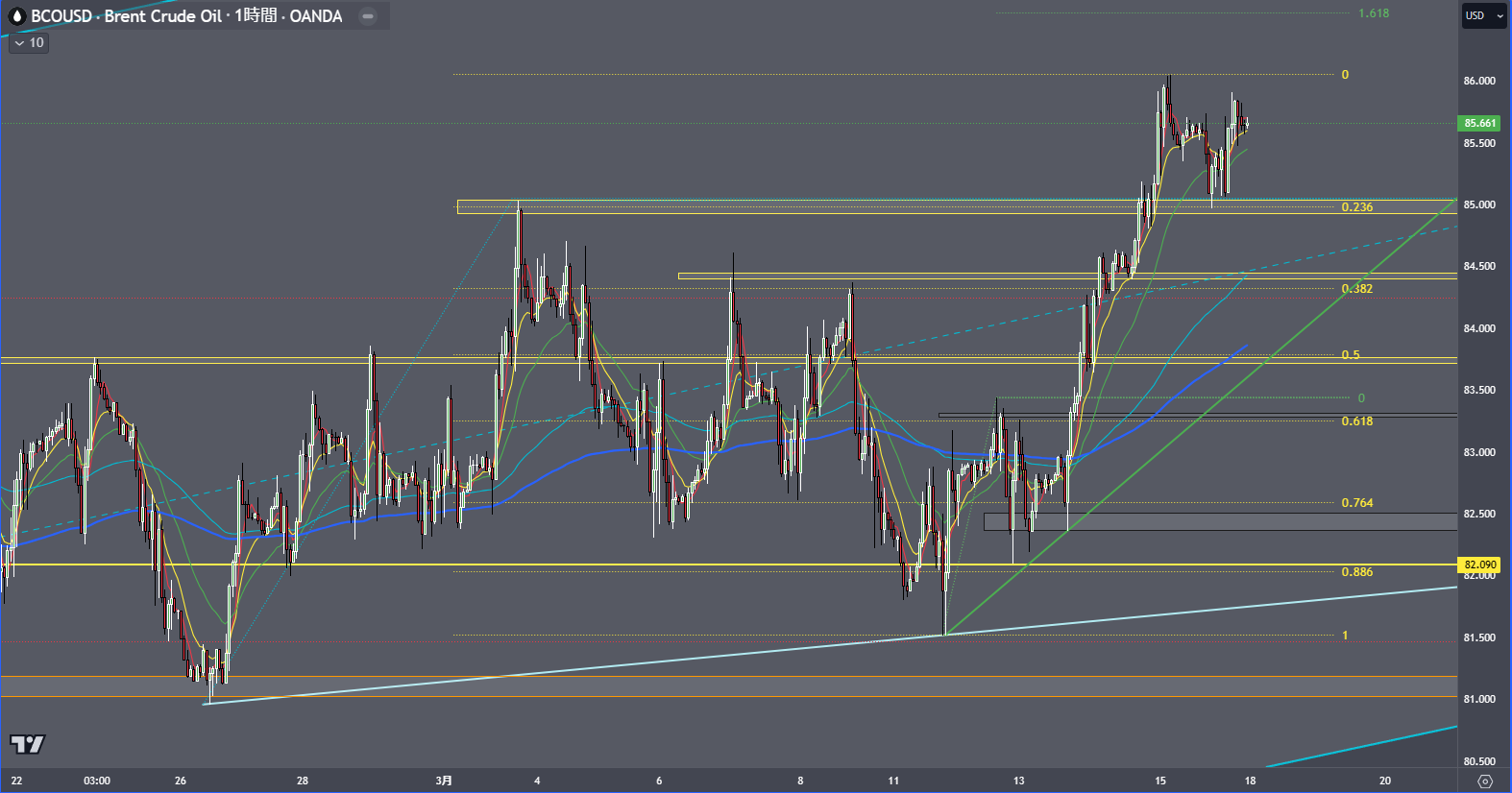

Chart-wise, Brent oil appears more straightforward than WTI. If prices continue pressing lower, expect a downward trend with supports around 84.5.

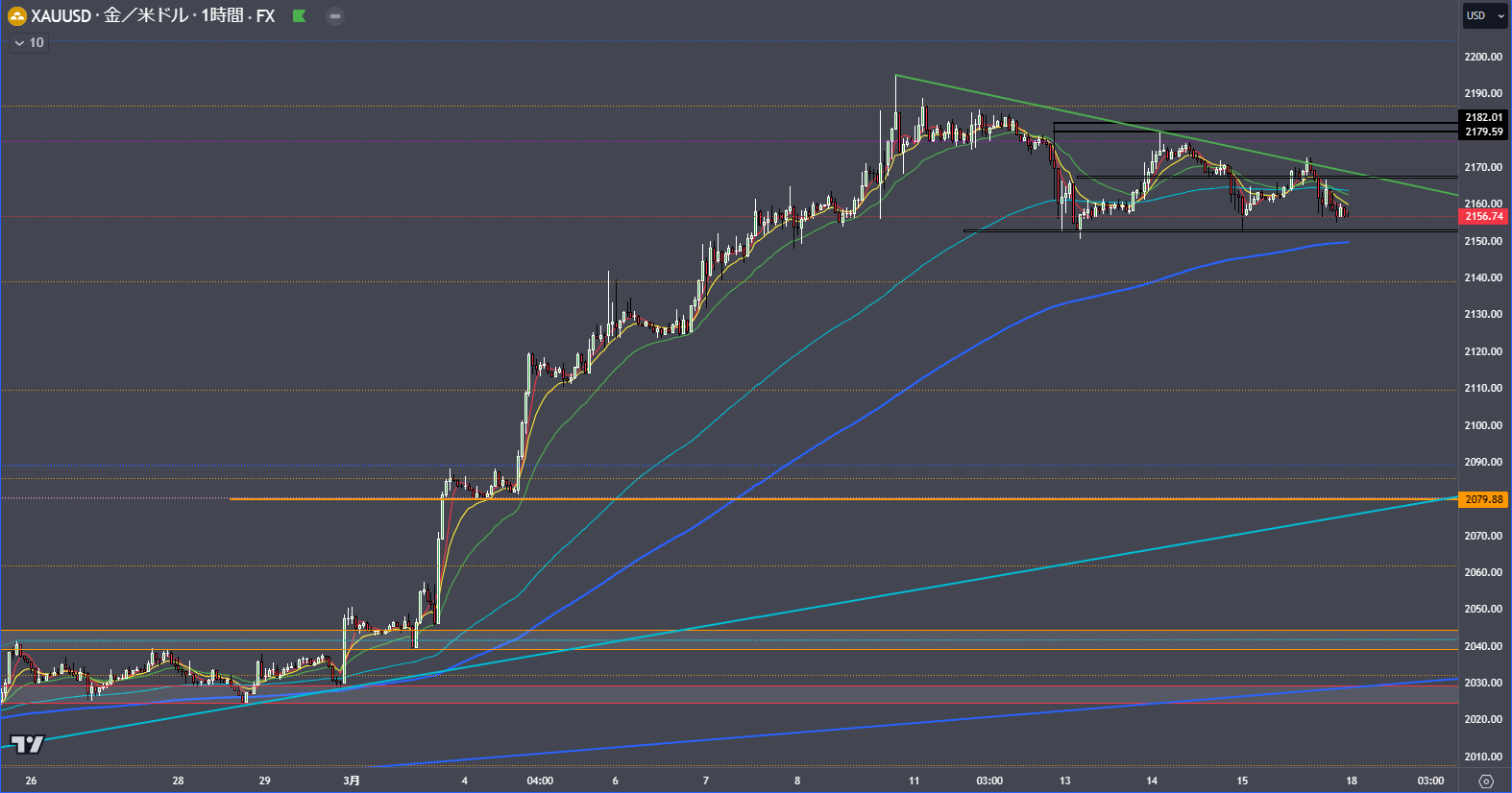

Gold is forming a disinflationary trend as predicted.

In futures, prices are closing near the lower bound, suggesting a higher likelihood of further declines when fundamentals are considered; thus, be cautious.

There may be ongoing pullbacks, but the gold ETF has been heavily accumulating, so shorting may be unwise.

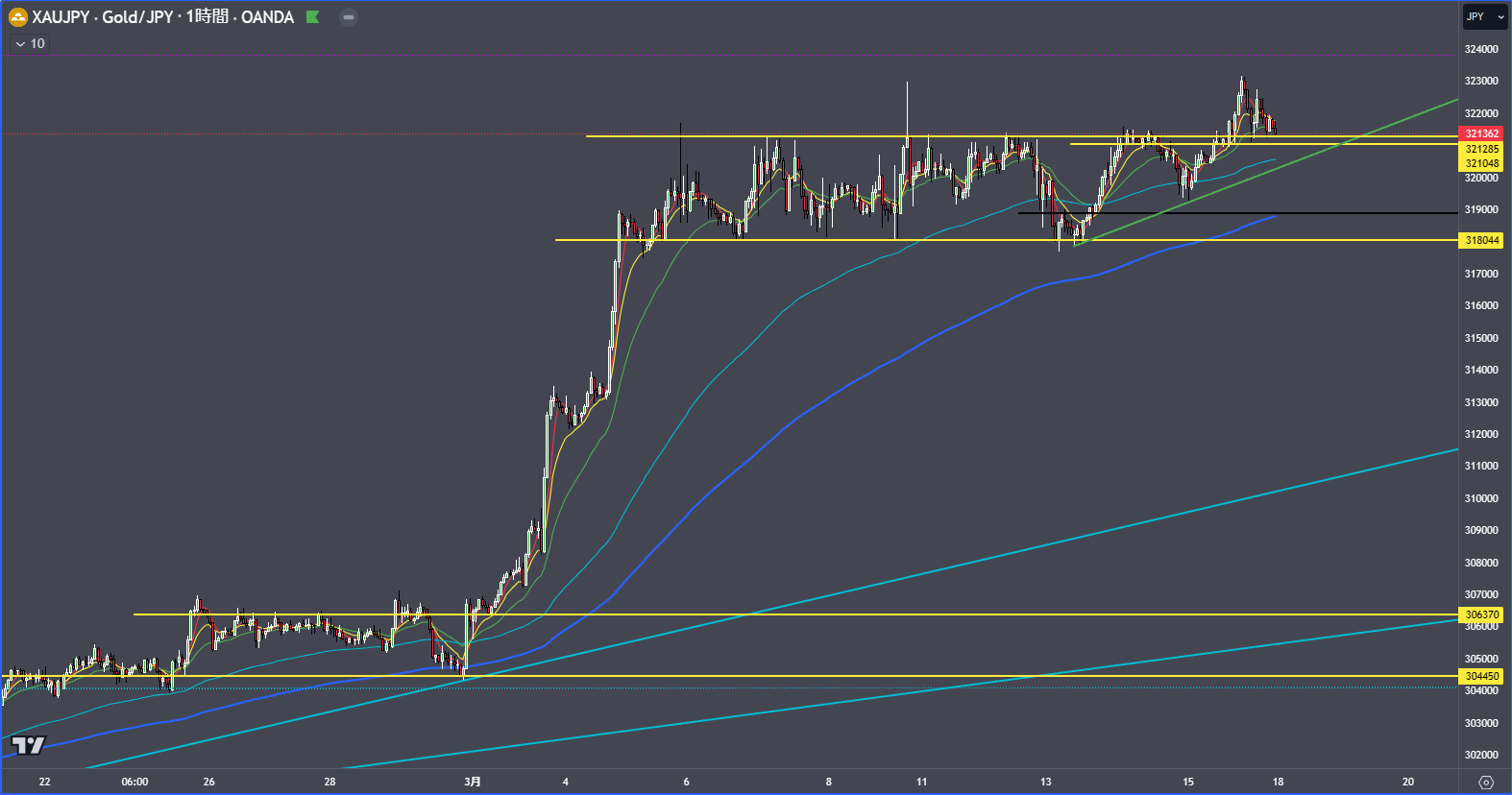

If buying, continue to target yen-denominated gold. With the range broken and a roll reversal in play, monitor closely from the open. Use the range’s full-length expansion as a take-profit target.

◇ Currency Markets

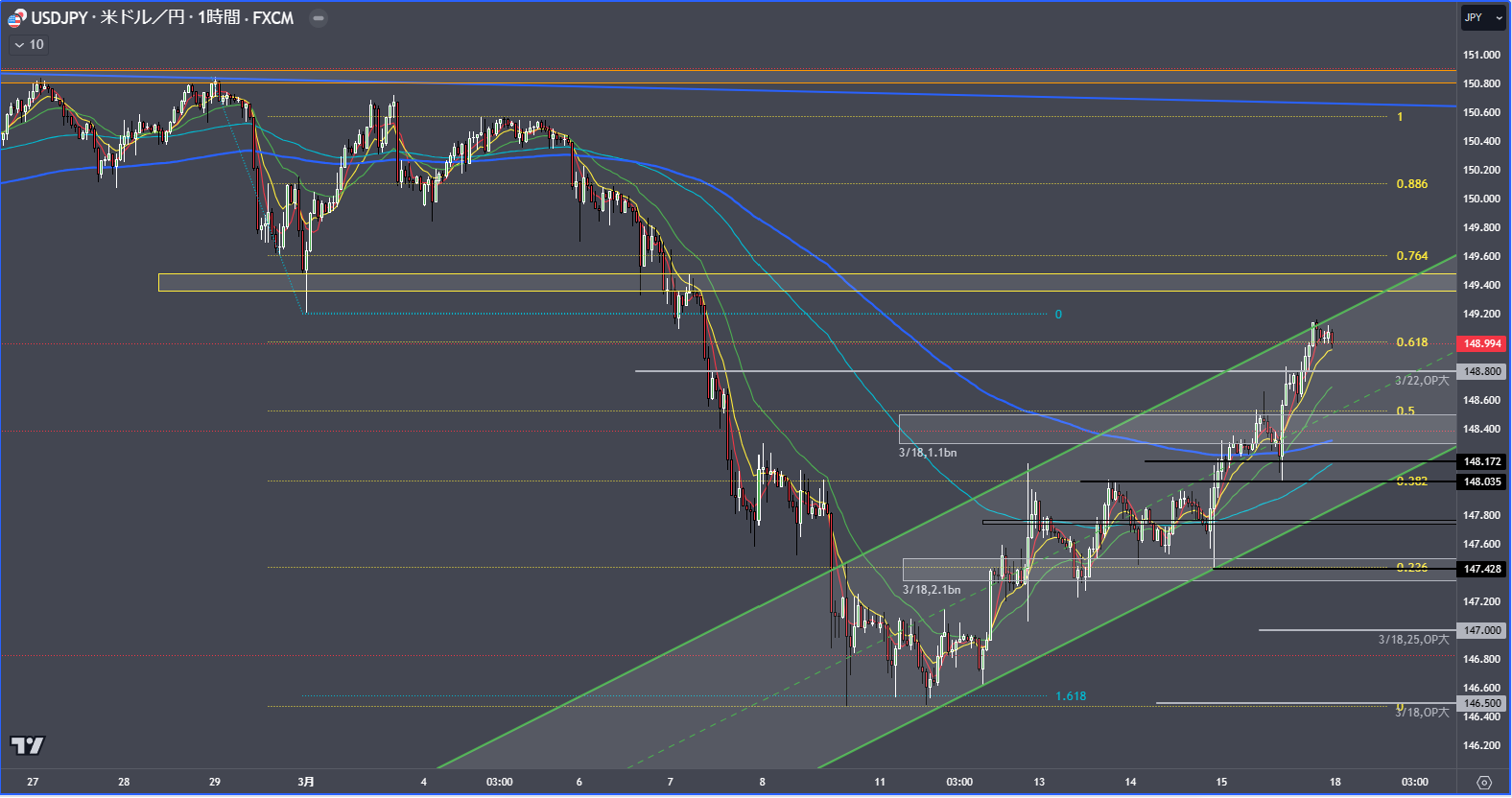

USD/JPY is likely to see profit-taking ahead of the BoJ meeting. There are sizable options around 148.8 and 148.4, so expect a choppy area near those levels. If it pulls toward 148, buying could be considered, but given limited yen buying and unclear one-year downside, wait for a correction before acting.

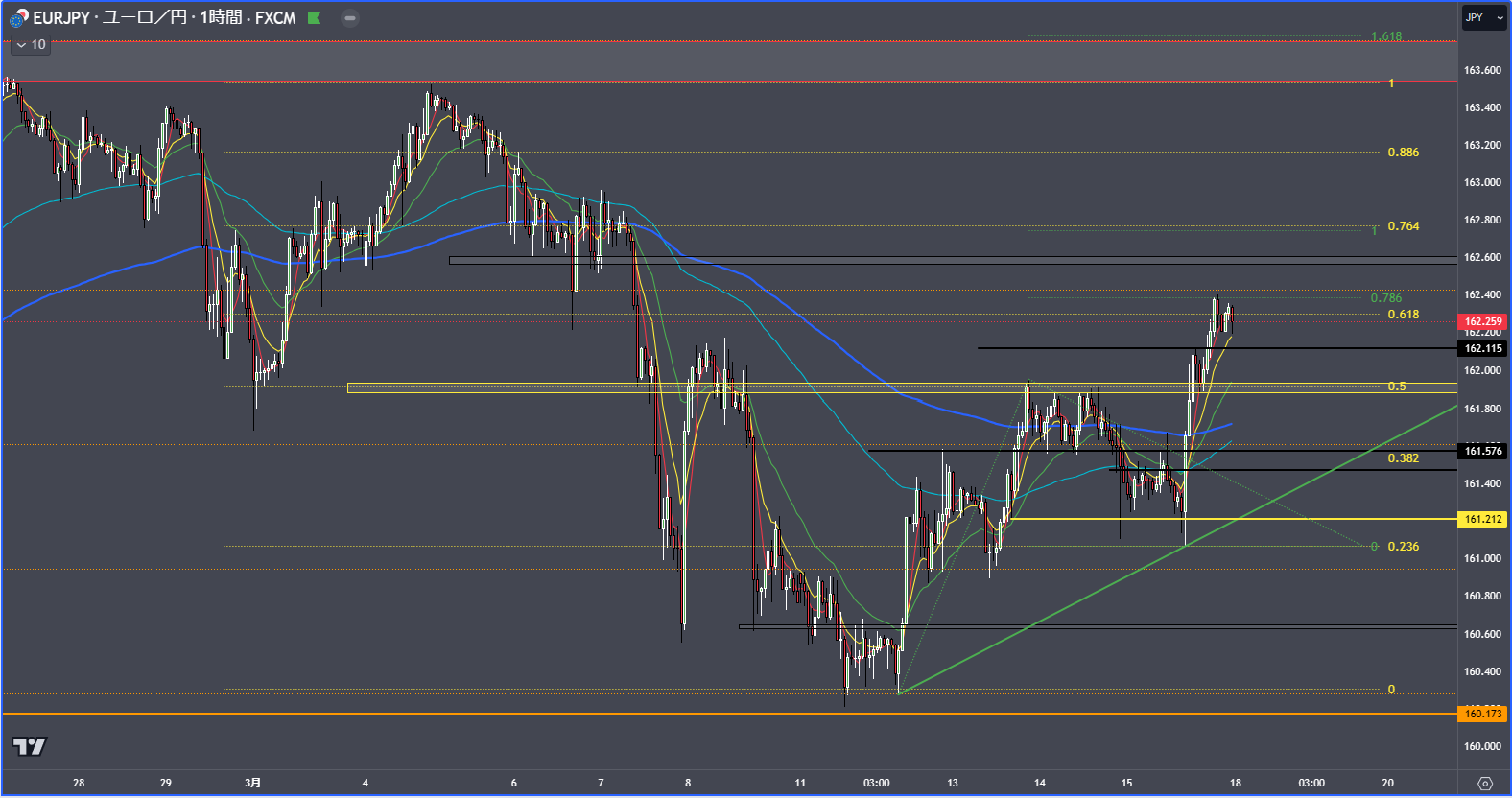

EUR/JPY had been expected to range, but has risen to new highs. I want to wait for a minor retrace to 161.9 before going long.

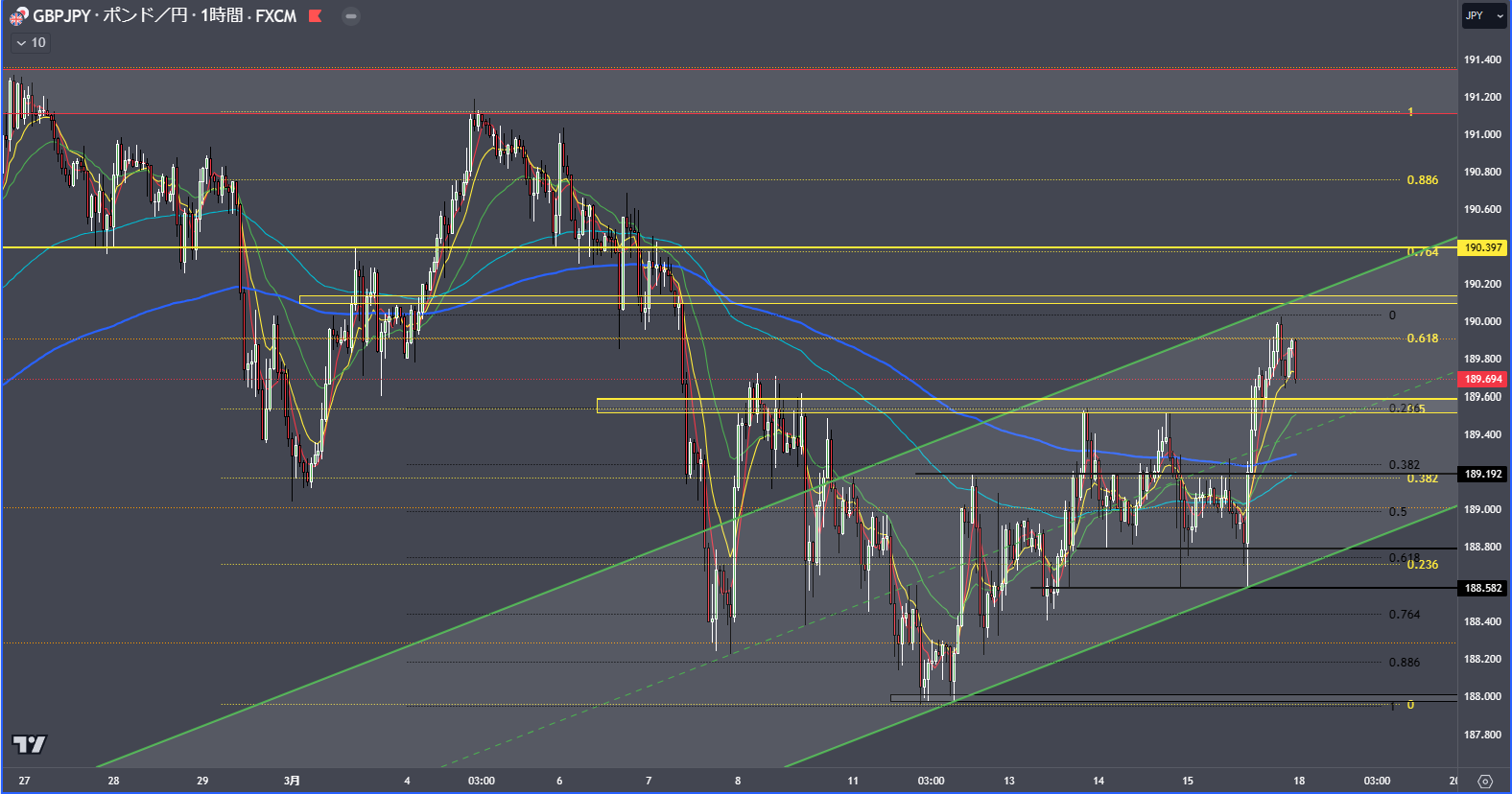

Similarly, I see potential for a long in GBP/JPY. Watch for a possible minor retrace to 189.6–189.5. If it breaks below, around 189.2 or 188.8 would make buying harder.

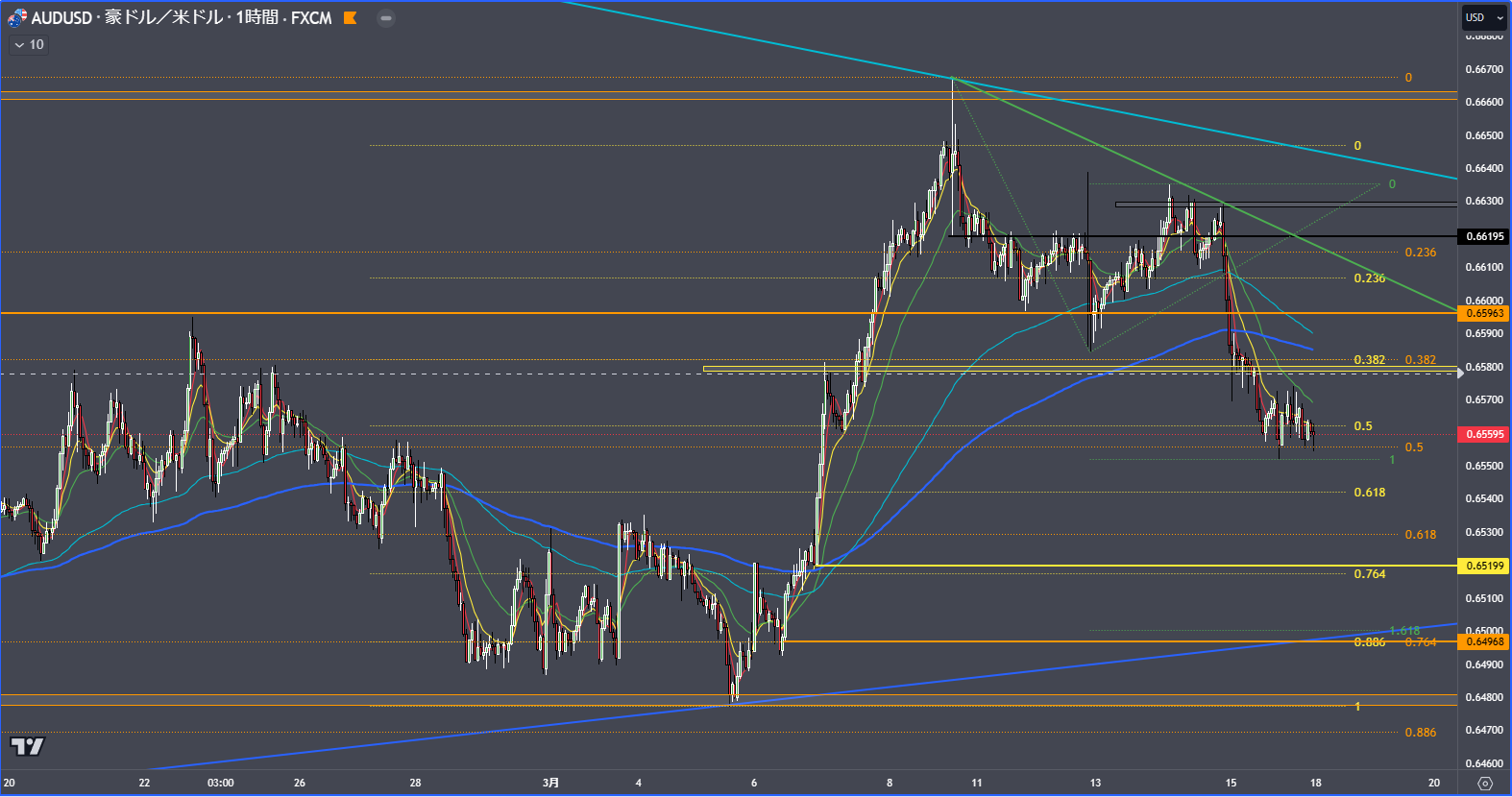

AUD/JPY remains a selling bias. The key level to sell is around 0.658; if it breaks higher, 0.6595 becomes the target. Seeing the two-lines, a break higher would indicate a downtrend continuation.

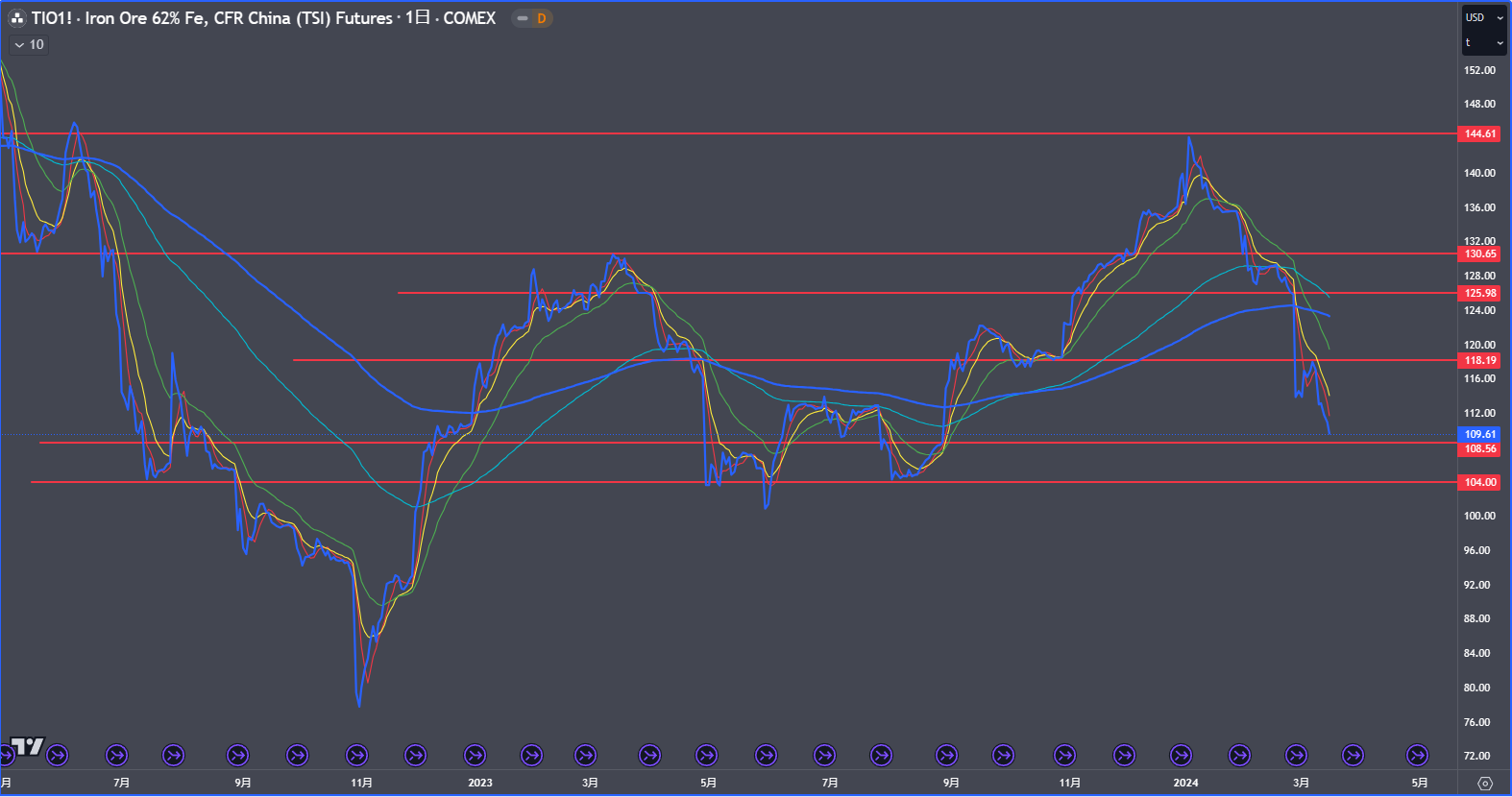

One reason for selling AUD is the sharp fall in iron ore, since Australia is a major iron ore exporter, impacting the currency.

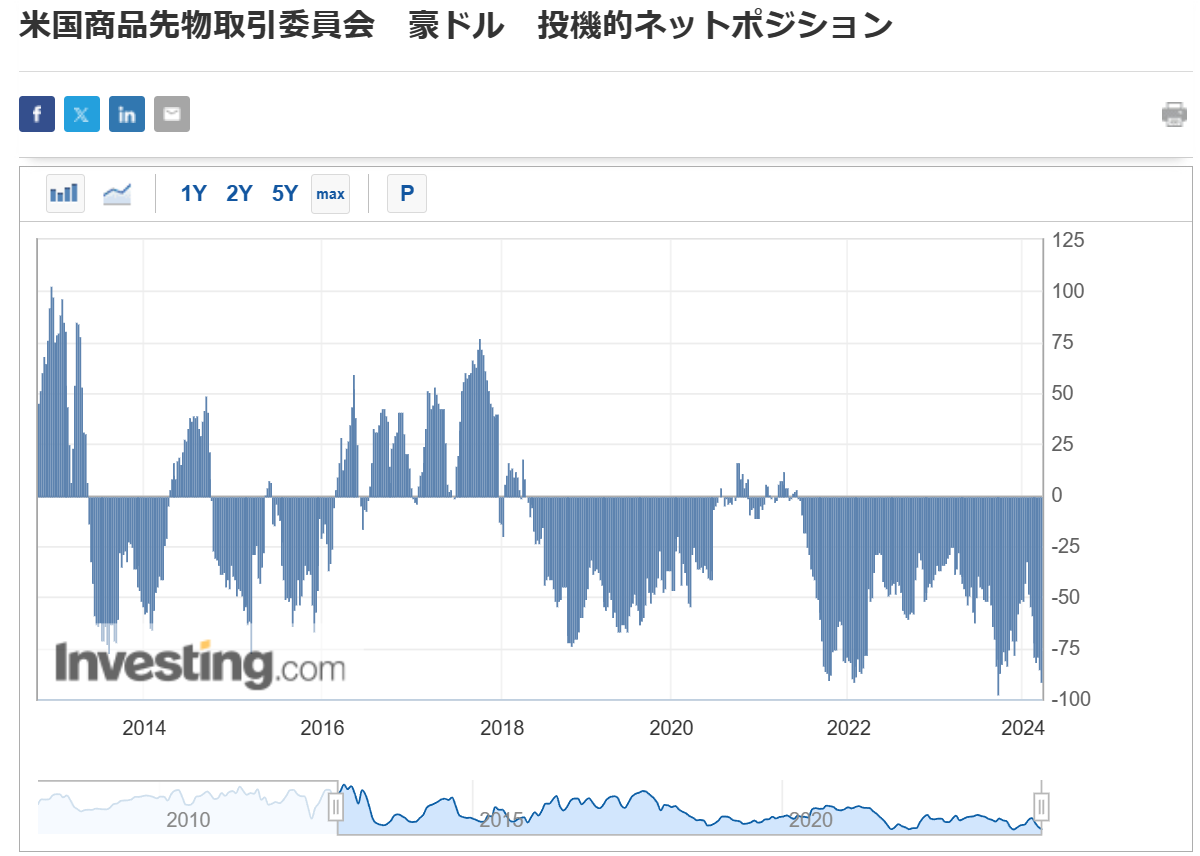

Note: The RBA meeting is on Tuesday, but speculative net shorts are at a low and have been heavily sold; shorts could be covered at the announcement. It’s better to close light positions before the meeting.

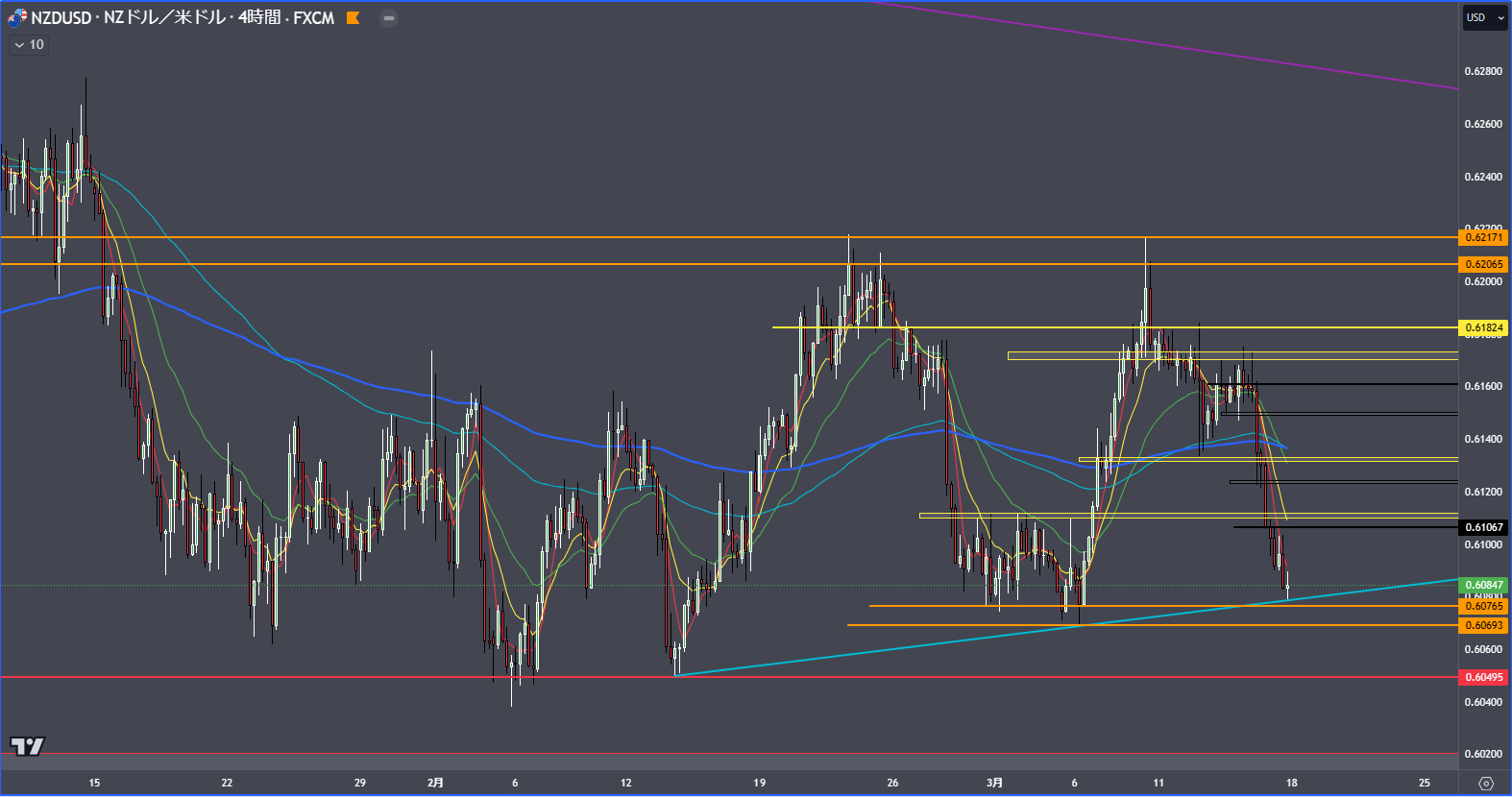

NZD has fallen to the lower bound and remains weak, as Finance Minister Willey signaled a significant downgrade of growth projections in the upcoming budget, depressing the NZD.

With the current lower bound, you may wait for a rebound to 0.611 or wait for a break and then look for a minor retrace.

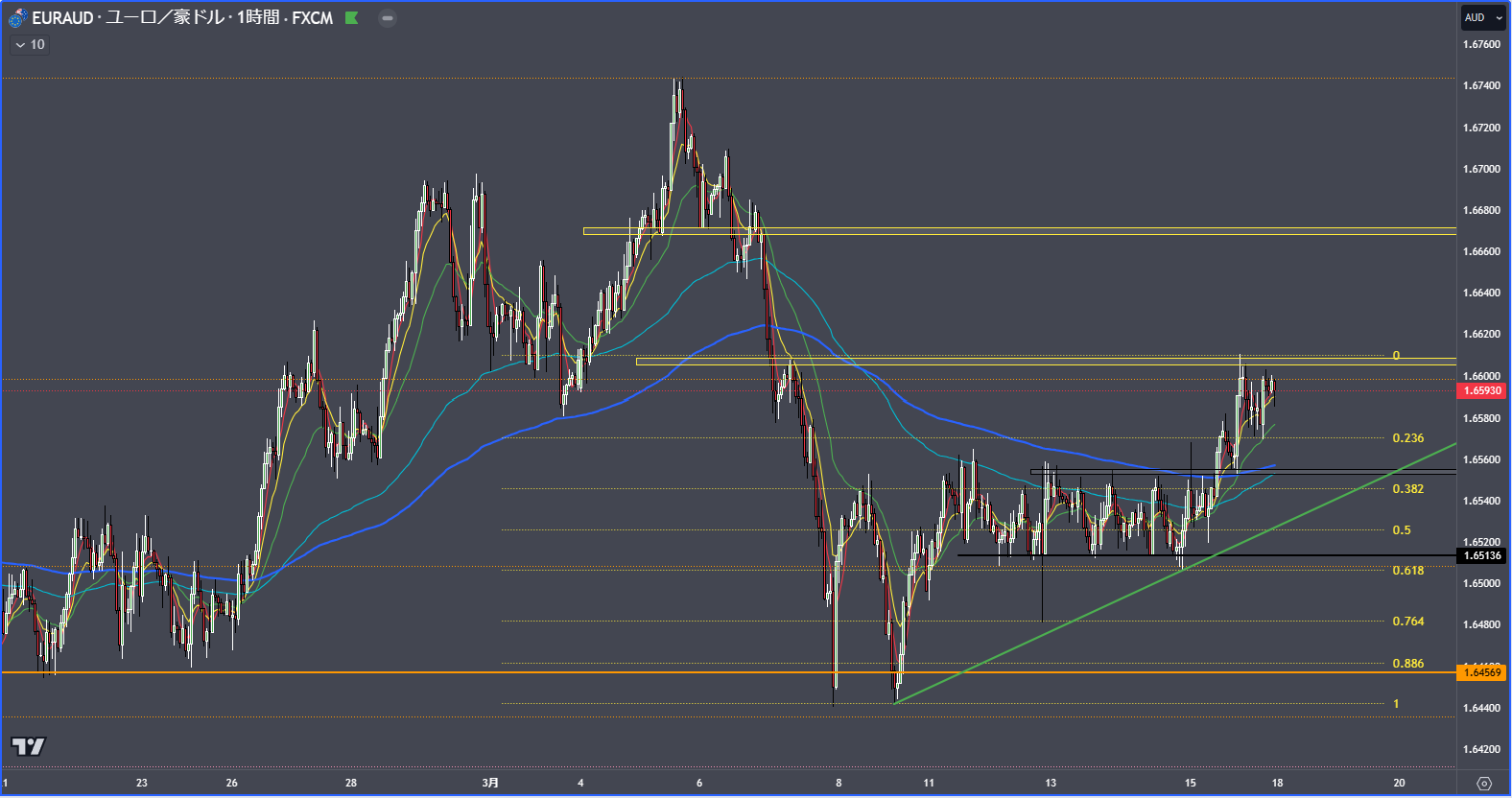

EUR/NZD long as predicted at 1.6555, with take-profit around 1.66.

I aim to stay long, either re-entering at 1.6555 or waiting for a roll reversal after new highs, keeping in mind the RBA meeting. If the meeting appears to unwind, it may be wise to skip.

※ This article does not constitute investment advice or solicitation. It is for information purposes only. However, none of the information provided guarantees certainty or usefulness. The author bears no responsibility for losses incurred by readers. Please understand the above and use the information at your own risk.