3/1 There is no problem with inflation

Notice before entering the article contentThis serial article is free for the first month, so if you’re curious, I would be happy if you could take a look for just one month.

Yesterday’s PCE deflator came in as market expectations, and given that CPI and PPI already suggested a slightly stronger tone, the year-over-year rate shows a slowdown, leading to a factual selloff. The slightly higher initial jobless claims also likely contributed to the dollar selling and U.S. interest rate declines.

Also, after the PCE release there was daily chair statements, the main points are as follows

- They want to avoid keeping rates at 2% inflation indefinitely- January’s PCE does not change the view that inflation is in a downward trend- Employment growth is expected to slow- To ease policy, it is necessary to confirm a slowdown in employment growth

- At present, three rate cuts this year feel appropriate

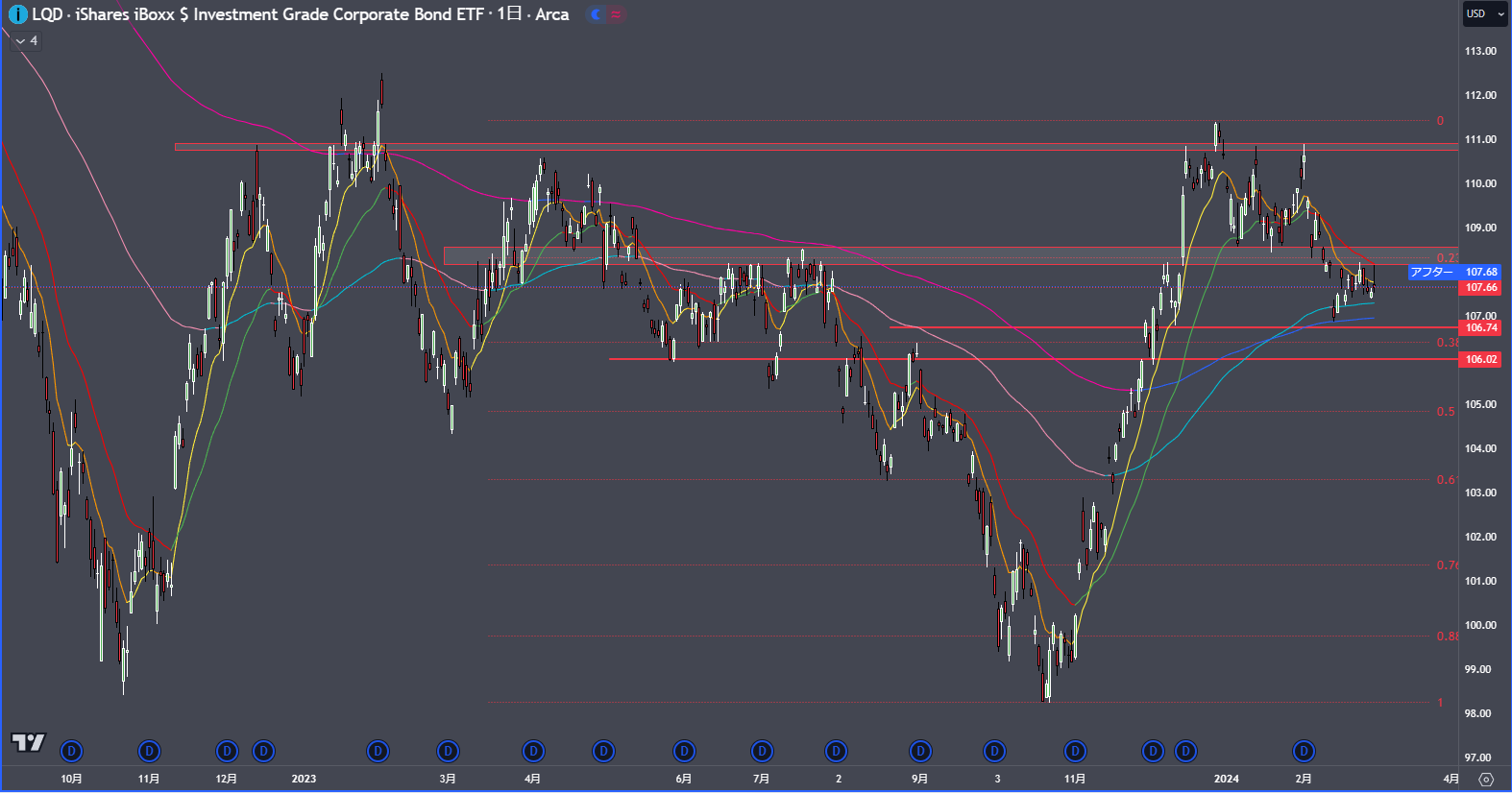

As with the CPI release and statements by officials, the path toward the inflation target remains fraught with twists and turns, and officials have not changed their view that inflation is declining.Following the release, U.S. rates fell but did not drop sharply; the range continues.The recent issuance of bonds and rising corporate bond prices have weighed on demand for U.S. Treasuries, contributing to the restraint on U.S. government bond buying.

Since upside potential is limited, a further rise is not expected at present, and the key will be the labor market direction in the coming week.Today’s ISM Manufacturing Index shows improvement in line with indicators, aligning with market expectations.

Taiwanese export orders, which have tracked ISM manufacturing sentiment, have improved significantly

New York Fed manufacturing index and Philadelphia index have also improved, creating an atmosphere of expectation

Also, today’s Taiwan PMI and Korea exports (semiconductors) results are relatively good, with a high possibility of further improvement.

◇ Foreign exchange