Sandwich Manase's Market Topic Lecture|Part 5. Swiss Franc

Sandwich Mase covers topics that are of interest in the current market. This time, alongside the Japanese yen, the “safe-haven” currency known as the Swiss franc. We will introduce the reasons based on Switzerland’s characteristics as a country and its central bank policy.

Here is the previous article

→Sandwich Mase's Market Topic Course | Part 4. Turkish Lira / Yen

This time we will discuss the Swiss franc, considered a safe-haven currency.

It may not be a major currency in Japan, but it is occasionally a currency that draws market attention.

1. The strongest safe haven?

Switzerland is a perpetual neutral country. Unlike the Japanese Constitution's Article 9, which stipulates renunciation of war and no maintenance of armed forces, Switzerland maintains an army and, for the purpose of defense of the country, the use of force is permitted. However, due to its distance from geopolitical risks associated with war, it is regarded as a safe asset and tends to be bought.

Another feature is that Switzerland has a high share of the current account surplus in its current account. The current account measures net financial flows between residents and non-residents, and a surplus in the trade balance (one component of the current account) means exports exceed imports.

In countries with strong export industries, a currency appreciation is not welcome. Hence, the Swiss National Bank (SNB) conducted foreign exchange interventions up to early 2015 to cap the Swiss franc’s strength, setting a ceiling of 1 euro = 1.2 Swiss francs.

2. The memorable Swiss franc shock

However, on January 15, 2015, a震撼 that shook the market occurred—the “Swiss franc shock.” At the time, rumors of the European Central Bank (ECB) considering new rounds of quantitative easing were circulating. As noted above, the SNB had defended a ceiling of 1 euro = 1.2 Swiss francs through selling the franc, but QE considered by the ECB would drive strong euro depreciation, which would, in turn, put further pressure on the franc.

As a result, before the ECB decided on QE, the SNB decided that it could no longer defend the line and abolished the 1.2 CHF per euro ceiling. The result was a sharp spike in the Swiss franc—the Swiss franc shock.

Source: Prepared by the author from Bloomberg data

Figure 1 shows the EUR/CHF monthly chart. On a monthly basis, the franc appreciated by about 2000 pips, and on the day of the shock, the rate briefly rose more than 3000 pips in favor of the franc.

3. A new line of defense?

Since then, EUR/CHF has traded in a range between 1.2 and 1.05 francs. Because many point to the idea that the Swiss franc shock was caused by SNB misjudgment, the SNB has continued selling francs to prevent repeating the same mistake. The pattern of SNB interventions can be inferred from the movement of foreign exchange reserves.

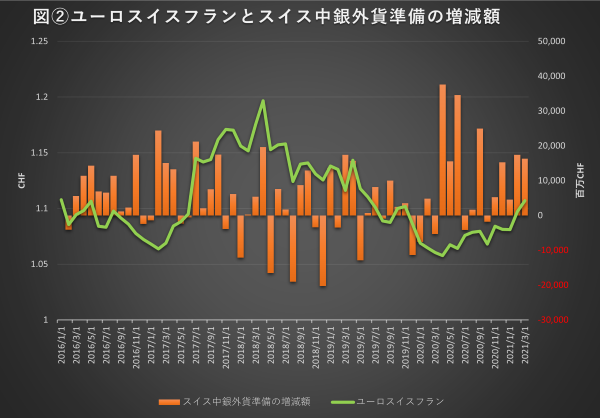

Source: Prepared by the author from Bloomberg data

Figure 2 shows the EUR/CHF chart and the changes in SNB foreign reserves, illustrating at what levels the SNB has intervened. It is evident that around the 1.05 CHF level, foreign reserves increase markedly, indicating active franc-selling interventions by the SNB at this rate.

Looking at the latest EUR/CHF, the franc appears to be weakening, suggesting SNB is taking relief.

However, if the franc strengthens again due to ongoing pressure, it would not be surprising to see the market again focus on the 1.05 CHF threshold.

Note: The content of this article is based on the author's views and is not a definitive investment recommendation. It is intended to provide information only, and does not solicit the buying or selling of any kind of product.

Certificate of Financial Planning at Level 1. Worked in financial product sales at a bank, then joined Invast Securities as a currency dealer. Currently in the Marketing Department, promoting the enjoyment of investing to the world. Widely reputed for answering financial questions instantly, and he strives daily to be a reliable, elder-brother-like figure. Also a sandwich enthusiast to the point of colleagues teasing him about never getting bored. Always handles work with a sandwich in hand. Additionally, he makes a sandwich for the next day every night before bed, a romantic trait people mistake for charm.