Australian dollar rises, RBA policy rate decision and statements released

◎RBA Policy Rate Announcement

Announcement at 12:30 on February 5

RBA Policy Rate: 1.50% (unchanged) as expected

◎RBA Statement Release

~Summary~

“Low policy rates continue to support the Australian economy.”

“Further progress toward the goal of full employment and inflation targets is expected, but progress may be gradual.”

“Unemployment is at 5%, and the labor market remains resilient.”

“Over the next 2-3 years, unemployment is expected to fall to 4.75%.”

“Inflation remains low and stable.”

“The underlining inflation is expected to pick up over the next 2-3 years, but the pick-up will be gradual and may take somewhat longer than previously expected.”

※The original text is attached below.

◎ Outlook and Interpretation

Today, a hold was expected. Despite consensus, AUD was bought heavily.

Why?

The focus was on the statement and Governor Lowe’s remarks.

Until now, the RBA (Governor Lowe) stance was that the next policy move would be a rate hike, timing undetermined. A rate cut was not expected, but recently the probability of a rate cut by the RBA has emerged. It was thought unlikely for a rate cut at this meeting, but if a cut were to occur within the year with about a 60% chance, AUD had been selling recently.

With the rate-cut probability in view, attention turned to whether the stance might have changed in the statement or Governor Lowe’s remarks.

As a result, there was no change in stance.

According to Kanda Takuya from Gaitame.com, the probability of a rate cut within the year: 60% yesterday → 40% this morning → 29.8% after the statement.

Australian rate-cut probability (within year) fell from 60% yesterday to 40% this morning, to 29.8% after the RBA announcement.pic.twitter.com/PL2Mtprb2U

— Takuya Kanda (@KandaTakuya)February 5, 2019

I think this decline in rate-cut probability contributed to AUD buying.

◎ Why the Rate-Cut Probability?

The RBA had been signaling that the next move would be a rate hike. So why did a rate-cut probability surface?

One factor was the rate hikes by major Australian banks. One of the monetary policy tools of central banks is easing policy to boost demand and consumption. Banks raising mortgage rates before the RBA moved to tighten could be seen as a de facto tightening in effect, which worried observers.

Another issue is housing debt. Soaring house prices increase mortgage burdens and could weigh on the economy. While the RBA hesitated to tighten, banks faced difficulties in funding and profitability at low rates and moved to raise mortgage rates.

Naturally, households with mortgages faced greater financial strain.

This led to talk of rate cuts surfacing more recently.

※References

RBA rate hikes likely after 2020 as financial institutions raise mortgage rates

◎ Focus on Governor Lowe’s Remarks Tomorrow

As noted above, the probability of a rate cut is not 0%. The statement showed no stance change, but Governor Lowe’s remarks remain. We will watch housing issues and any shift in policy stance.

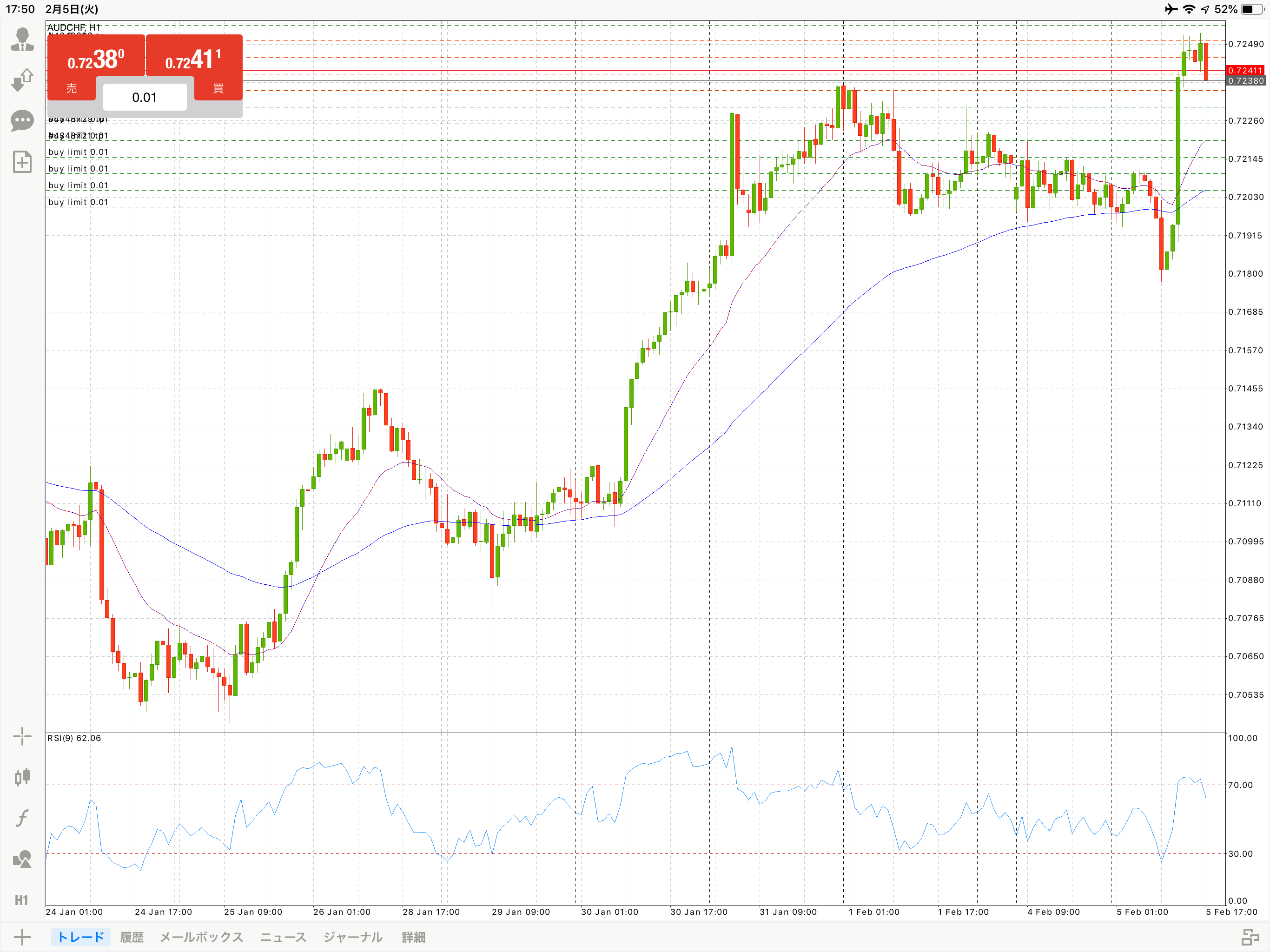

◎ Post-Announcement Repeat Chart

Using an EA on AUD/CHF for repeats.

Recently, with the rate-cut probability appearing, AUD fell. It went below the expected range, but today’s movement has returned to the expected range.

AUD/CHF 5-minute chart AUD/CHF 1-hour chart

AUD/CHF 1-hour chart

AUD/CHF Daily chart

AUD/CHF Daily chart

AUD/CHF Weekly chart

AUD/CHF Weekly chart

From here, I hope it will drift within the expected range...

◎ Original RBA Statement

Statement by Philip Lowe, Governor:

Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy grew above trend in 2018, although it slowed in the second half of the year. Unemployment rates in most advanced economies are low. The outlook for global growth remains reasonable, although downside risks have increased. The trade tensions are affecting global trade and some investment decisions. Growth in the Chinese economy has continued to slow, with the authorities easing policy while continuing to pay close attention to the risks in the financial sector. Globally, headline inflation rates have moved lower due to the decline in oil prices, although core inflation has picked up in a number of economies.

Financial conditions in the advanced economies tightened in late 2018, but remain accommodative. Equity prices declined and credit spreads increased, but these moves have since been partly reversed. Market participants no longer expect a further tightening of monetary policy in the United States. Government bond yields have declined in most countries, including Australia. The Australian dollar has remained within the narrow range of recent times. The terms of trade have increased over the past couple of years, but are expected to decline over time.

The central scenario is for the Australian economy to grow by around 3 per cent this year and by a little less in 2020 due to slower growth in exports of resources. The growth outlook is being supported by rising business investment and higher levels of spending on public infrastructure. As is the case globally, some downside risks have increased. GDP growth in the September quarter was weaker than expected. This was largely due to slow growth in household consumption and income, although the consumption data have been volatile and subject to revision over recent quarters. Growth in household income has been low over recent years, but is expected to pick up and support household spending. The main domestic uncertainty remains around the outlook for household spending and the effect of falling housing prices in some cities.

The housing markets in Sydney and Melbourne are going through a period of adjustment, after an earlier large run-up in prices. Conditions have weakened further in both markets and rent inflation remains low. Credit conditions for some borrowers are tighter than they have been. At the same time, the demand for credit by investors in the housing market has slowed noticeably as the dynamics of the housing market have changed. Growth in credit extended to owner-occupiers has eased to an annualised pace of 5½ per cent. Mortgage rates remain low and there is strong competition for borrowers of high credit quality.

The labour market remains strong, with the unemployment rate at 5 per cent. A further decline in the unemployment rate to 4¾ per cent is expected over the next couple of years. The vacancy rate is high and there are reports of skills shortages in some areas. The stronger labour market has led to some pick-up in wages growth, which is a welcome development. The improvement in the labour market should see some further lift in wages growth over time, although this is still expected to be a gradual process.

Inflation remains low and stable. Over 2018, CPI inflation was 1.8 per cent and in underlying terms inflation was 1¾ per cent. Underlying inflation is expected to pick up over the next couple of years, with the pick-up likely to be gradual and to take a little longer than earlier expected. The central scenario is for underlying inflation to be 2 per cent this year and 2¼ per cent in 2020. Headline inflation is expected to decline in the near term because of lower petrol prices.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.