EA without backtesting

Geko is here.

I am explaining portfolio creation in a series.

This time, I will explain my own portfolio exclusion criteria.

The exclusion criteria are as follows.

- Those with negative forward performance

- Those without backtesting

- Those with a short backtesting period

This time,

2. Those without backtesting

about that.

To begin with, not only EA but when developing a product, some criteria are necessary.

Something produced without criteria cannot be said to be “development” or “production”; it would be nothing but a haphazard creation.

In EA development, the criterion is whether the program seems capable of yielding profit, and the evaluation basis for that is backtest data.

In other words, an EA without backtest data is nothing more than a system created haphazardly, with no performance evaluation.

Could you entrust your valuable asset management to such a product?

To put it simply, it’s like boarding a plane that has undergone no testing at all and entrusting your life to it.

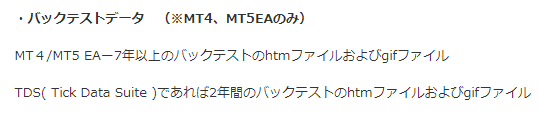

Fortunately, all the EA listings on Gogojan come with backtests attached.

(See below)

There is a difference between my opinion and the backtest period, but that will be saved for next time.