Trading Strategy Considering Investors' Risk Appetite ( Appetite for Risk ) [February 7–February 11]

Last Week's Foreign Exchange Range (Volatility Range)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 115.21 | 114.17 | 115.60 | 115.20 | ▲0.01% |

| EUR/USD | 1.1140 | 1.1138 | 1.1485 | 1.1446 | +2.70% |

| EUR/JPY | 128.43 | 128.38 | 132.11 | 131.86 | +2.67% |

| USD/CNH | 6.3677 | 6.3482 | 6.3861 | 6.3576 | ▲0.16% |

| CNH/JPY | 18.0931 | 17.9422 | 18.1550 | 18.1115 | +0.10% |

Last Week's Foreign Exchange Summary

USD/JPY

- Last week's dollar/yen started at 115.21 yen per dollar. At the beginning of the week, amid a correction in dollar buying, dollar selling prevailed and the USD/JPY showed a gradual decline. When the January US ADP employment data for January came in at ▲301,000, a weak figure, the pair briefly fell to 114.17. However, viewed as a dip, subsequent gains dominated, turning higher, and by Friday it recovered to the 115 level, closing the week at 115.20 after pulling back to 115.43 supported by the US January government-sector employment data.

EUR/USD

- The euro started at 1 euro = 1.1140 dollars. Early in the week, dollar weakness led to a steady rise, with the euro climbing back toward the 1.1300 area as strength grew. In the spotlight, during the ECB Governing Council, President Lagarde signaled that she would not rule out rate hikes within the year, sending the euro sharply higher toward the upper 1.14s. The euro remained firm over the weekend, reaching a high of 1.1485 and closing at 1.1446.

USD/CNH

- The yuan started at 1 USD = 6.3677 yuan. During the Spring Festival week, activity was subdued, with the dollar selling exerting a mild downward pressure. It closed at 6.3591.

What Happened Last Week

※ Price indices and money statistics are year-on-year, GDP is quarter-on-quarter, and metrics without a specific note are month-on-month or current-month values31st

- Japan December industrial production ▼1.0%

- Eurozone Q4 GDP +0.3% (Eurozone growth is weak)

- Germany January CPI +4.9%

- Mexico INEGI releases Q4 2021 GDP at -0.1% quarter-on-quarter, following -0.4% in Q3 2021, marking two consecutive quarterly contractions,a typical recession signal.

1st

- Chinese markets observe Lunar New Year holidays (through the 6th)

- Australia December retail sales ▼4.4%

- Reserve Bank of Australia announces unwinding of quantitative easing; policy rate kept at 0.10%

- Germany December retail sales ▼5.5%

- France January CPI ▼2.9%

- Germany January unemployment rate +5.1%

- Eurozone December unemployment 7.0%

- U.S. January ISM manufacturing index 57.6 (solid)

- U.S. December JOLTS job openings 10.775M (still indicating labor shortage)

- RCEP, including Korea, comes into effect in 10 countries; Malaysia expected to join in March, finalizing a 15-country RCEP

2nd

- Japan January monetary base +8.4%

- Eurozone January CPI +5.1%

- U.S. January ADP employment ▼301,000 (weak)

- Brazilian Central Bank raises policy rate by 1.5 percentage points to 10.75%

- COVID-19 infections reach record highsEU countries ease many restrictions as vaccines spread and Omicron’s severity is lower; treating it as endemic and moving society toward normalcy

- Turkish Finance Minister Nurettin Nebati says, in an interview with Nikkei, that market-driven rate hikes by the central bank to stabilize the lira are "not conceivable"Wealth-protection measures like guaranteed time deposits to encourage lira holdings keep the currency relatively stable, but inflation remains high and risks grow if the lira falls.

3rd

- Australia December new home building approvals +8.2%

- Australia December trade balance AU$8.356b

- Eurozone December PPI +26.2% (very high price pressures)

- Bank of England raises policy rate by 0.25 percentage point to 0.50%

- U.S. previous week initial jobless claims 238,000

- U.S. Q4 2021 nonfarm productivity +6.6% (quarter-over-quarter)

- U.S. January ISM nonmanufacturing PMI 59.9 (solid)

- In New York, WTI crude futures rose above $90 per barrel for the first time since October 2014 (about 7 years and 4 months) due to tight supply and robust demand.

- BOE raises rates further; ECB signals possible hikes later this year; major central banks begin to adjust policies after easing during the pandemic.

- French President Macron and Russian President Putin held talks on the ongoing Ukraine tensions; both sides agreed to continue negotiations on Ukraine and other issues.

- NATO Secretary General Stoltenberg warned of Russian troop movements to Belarus, with up to 30,000 troops considered, raising tensions surrounding Ukraine.

- Turkish Statistics Institute reports January CPI up 48.69% year-on-year, accelerating from 36% the previous month; highest since April 2002.

4th

- RBA Quarterly Monetary Policy Statement

- Germany December new orders in manufacturing +2.8%

- Eurozone December retail sales ▼3.0%

- Canada January employment: unemployment 6.5%, new hires ▼200,000

- U.S. January employment: unemployment 4.0%, nonfarm payrolls +467,000 (overall strong; dollar strengthened)

- Xi Jinping and Vladimir Putin met in Beijing; Xi expressed support for Russia's stance on Ukraine, while Putin appeared to endorse China's stance on Taiwan; both criticized Western security strengthening and signaled a tougher stance against democracies.

- The 17-day Beijing Winter Olympics opened. Despite COVID-19 concerns and human rights criticisms, the opening ceremony aimed to celebrate and unify domestically, though some delegations chose not to smile during the parade.

Glossary of Economic Terms

- GDP = Gross Domestic Product: higher growth is positive

- CPI = Consumer Price Index: many advanced economies target 2%

- PCE = Personal Consumption Expenditures: closely correlated with consumer prices

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Manager Index: 50 is the neutral point

- ZEW = Leibniz Centre for European Economic Research: 0 is the baseline

- NAHB = National Association of Home Builders: 50 is neutral

- NY Fed manufacturing index: 0 is the baseline

- Philly Fed manufacturing index: 0 is the baseline

- Richmond Fed manufacturing index: 0 is the baseline

- Chicago Purchasing Managers Index: 50 is the baseline

- University of Michigan Consumer Sentiment Index: indexed to 100 in 1966

- S&P/ Case-Shiller Home Price Index: “20-C city house price index” is widely used; key for housing market trends

- Pending Home Sales Index: counts contracts not yet closed for housing

- European Consumer Confidence Index: index around 100 with 2000-2020 average; released as a month-over-month figure

- Eurozone Economic Sentiment Index: index around 100 with 2000-2020 average; released as actuals

- Consumer Confidence Index: indexed to 100 in 1985

- Japan Coincident Economic Index: indexed to 100 in 2015

- Japan Mood Watch Survey: 50 is the neutral

- Japan Corporate Services Confidence Survey: 0 is the neutral

Notable Economic Indicators and Political Events

7th

- U.S.-Germany Summit (Washington)

- German-French foreign ministers visit Ukraine

- 10:45 China January Caixin Services PMI

- 14:00 Japan December Confidence Index

- 16:00 Germany December Industrial Production

- 24:45 Lagarde ECB President speaks at Economic and Monetary Affairs (ECON)

8th

- 08:50 Japan December International Balance of Payments

- 14:00 Japan January Economy Watchers Survey

- 22:30 U.S. December Trade Balance

9th

- 08:50 Japan January M2 money stock

- 16:00 Germany December Trade Balance

- 24:00 U.S. December Wholesale Trade

10th

- 08:50 Japan January Domestic Corporate Goods Price Index

- 17:30 Riksbank (Sweden) policy rate

- 22:30 U.S. January Consumer Price Index

- 22:30 Previous week's initial unemployment claims

- 28:00 Mexico Bank, policy rate

11th

- Japan Holiday (National Foundation Day)

- IEA Oil Market Report for February

- 16:00 UK Q4 Domestic Product

- 16:00 UK December Industrial Production

- 19:30 Russia Central Bank policy rate

- 24:00 U.S. February University of Michigan Consumer Sentiment Index (preliminary)

Next Week and Beyond

- March 5: National People's Congress

- March 9: South Korea presidential election

- March 10: ECB

- March 16: FOMC (with economic projection data)

- March 18: Bank of Japan Monetary Policy Meeting

- April 14: ECB

- April 28: BoJ Monetary Policy Meeting (with outlook for economy and prices)

- May 4: FOMC

- June 9: ECB

- June 15: FOMC (with economic projection data)

- June 17: BoJ Monetary Policy Meeting

- July 21: BoJ Monetary Policy Meeting (with outlook for economy and prices)

- July 21: ECB

- July 27: FOMC

- September 8: ECB

- September 21: FOMC (with economic projection data)

- September 22: BoJ Monetary Policy Meeting

- October 27: ECB

- October 28: BoJ Monetary Policy Meeting (with outlook for economy and prices)

- November 2: FOMC

- November 8: U.S.-China midterm elections

- December 14: FOMC (with economic projection data)

- December 15: ECB

- December 20: BoJ Monetary Policy Meeting

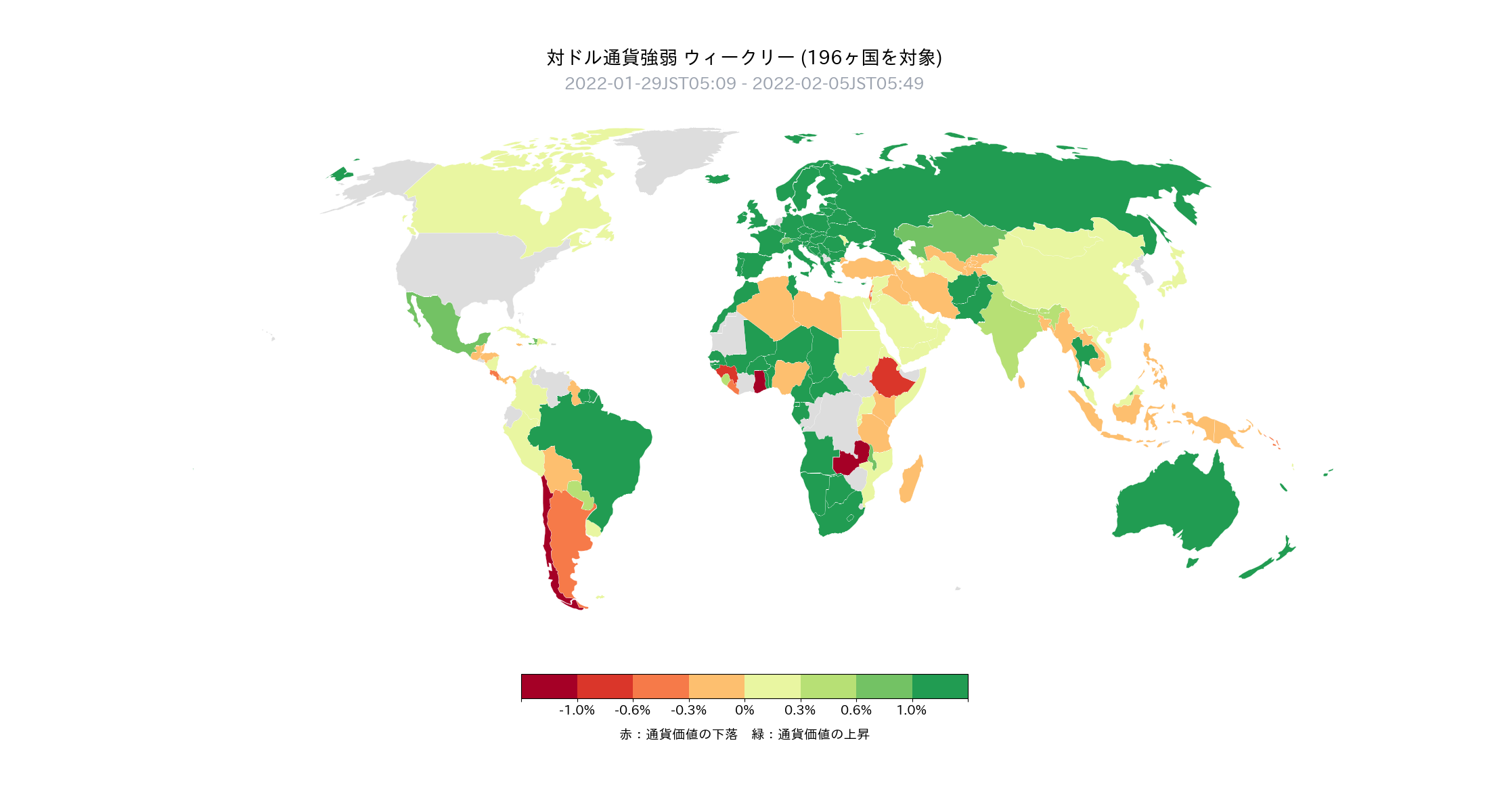

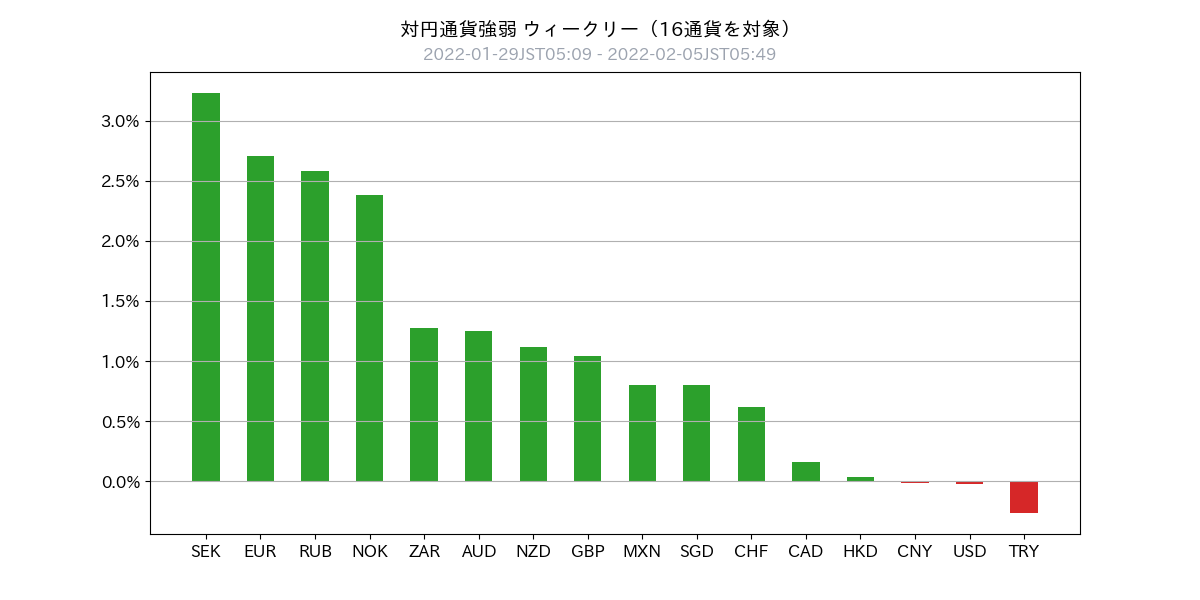

Last Week's Currency Strength

- Last week, dollar selling was dominant (149/196 countries).It was a corrective phase for the dollar purchases that had been advancing unilaterally.

- Among major currencies, the euro was bought especially heavily. The ECB's Lagarde taking a stance that does not rule out a rate hike within the year attracted buying.

- Scandinavian currencies and the Russian ruble were also bought back,likely reflecting expectations for progress in the Ukraine situation.

- In summary, last week's currency strength/weakness was as followsEuro > Scandinavian currencies and the Russian ruble > British pound > yen > US dollar and yuan

Global Macro Environment (Latest)

- Perhaps due to the Winter Olympics, there was a somewhat optimistic mood in the stock market over the past week(S&P 500 fear index fell from 27.66 to 23.22)

- However, with the UK indicating a rate hike and the euro area showing a willingness to hike within the year,it was a week that reminded us of a global tightening cycle.

- What remains for market participants is likely the two questions: the pace of the FED's shrinking of its balance sheet and the Ukraine issue.

- Regarding the expectation of earlier FED tightening, it is anticipated that attention will focus on statements from FED officials by the FOMC on March 16.

- As for the Ukraine issue, considering talks among Eurasian leaders and officials and the Olympic period, it is reasonable to think the situation will not deteriorate much for the time being. Against that backdrop, a bit of calm is returning to the market, it feels.

- Next week has no major events, so it may be a week where market participants' sentiment can be reflected straightforwardly.

- At this point, I feel a bit pessimistic, so I intend to approach risk assets with a buy-on-dip strategy

- Additionally, while not much attention was paid to Japan's monetary policy before, given inflation, I expect more focus from now on and will monitor carefully

- We will continue to watch the U.S. Democratic Party (Build Back Better) bill

Global Macro Environment (Supplementary)

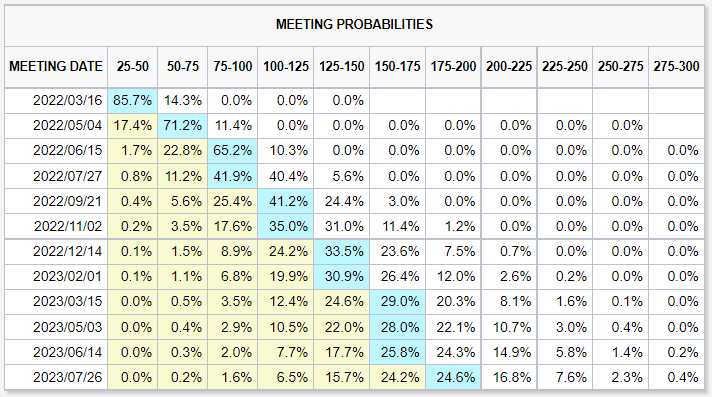

- About 85.7% of participants in the interest-rate futures market expect the U.S. rate hike to begin in March this year (25bps)

- Some participants (14.3%) expect a 50bps hike in March this year (slightly higher than last weekend)

- Rate hike expectations for this year center around five increases, unchanged (the rate-hike pricing is now broadly shared and may not be a major driver)

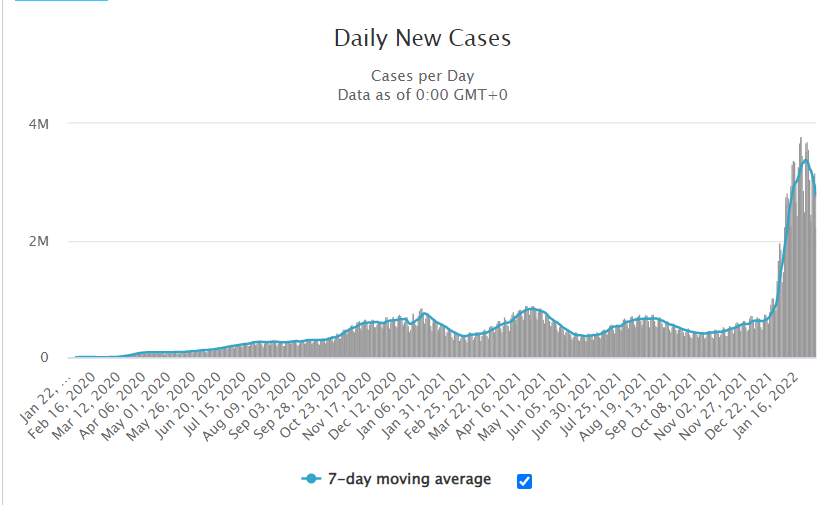

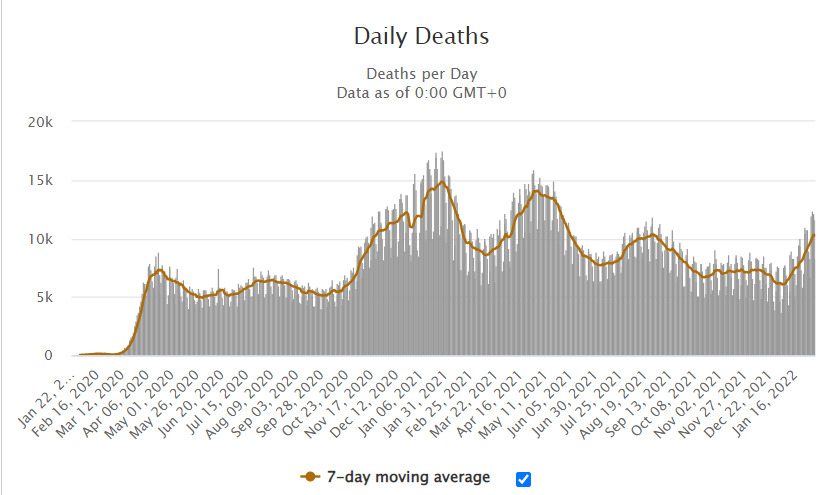

- The trend in new COVID-19 cases (7-day moving average) shows a tendency to level off (attached chart Daily New Cases)

- On the other hand, the trend in new COVID-19 deaths (7-day moving average) has turned upward, which warrants caution (attached chart Daily New Cases)

- If the number of new infections starts to decline, deaths will likely stabilize soon, so monitoring the trend in infections remains necessary.

Chart Analysis

USD Index (Daily)

- DXY is an index of overall dollar strength (basket composition: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Adjusted just before 97.65

- At around 94.70, one would want to start buying dollars

USD/JPY Mid-term (Daily)

- The upward move on a daily basis continues to be tested

- Expecting a move to test last year's high of 116.35 yen

USD/JPY Short-term (Hourly)

- On the upper green trendline, it is somewhat higher

- Would like to buy on dips around the lower green trendline

EUR/USD Mid-term (Daily)

- Clearly broke above the long-standing downtrend (green line); going forward, selling easily could hurt

EUR/USD Short-term (Hourly)

- Recently, the nearby high around 1.1480 is acting as resistance, so if it breaks above, I want to follow with a buy

- The downside target is around 1.1370, which could be a buying opportunity

USD/CNH Mid-term (Daily)

- The downtrend appears to continue

USD/CNH Short-term (Hourly)

- Trading around 6.35 with unclear direction

- Will watch for the PBOC's short-term liquidity operation after the Spring Festival

This Week's Toda's Trading Strategy

Overall Policy

- The dollar is cheap, so a buy-on-dip approach is desired

- Would like to hold long USD/CNY, but monitor central bank actions at the start of the week

- The yen is biased to selling

- Will monitor risk assets and buy on significant declines while watching for risks

USD/JPY

- Last Friday's close: 115.20

- View: range-bound to higher

- Expected range: 114.50–116.50

- Current position: USD/JPY long 2.0

- Watching the dollar index and the USD/JPY trendline (hourly, green) to guide buy-on-dip entries

EUR/USD, EUR/JPY

- Last Friday's close: EUR/USD 1.1446

- View: EUR/USD range-bound to higher; EUR/JPY higher

- Expected range: EUR/USD 1.1370–1.1530

- Current positions: EUR/USD ±0, EUR/JPY ±0

- If it drops to around 1.1370, would like to enter long

- Since dollar is considered oversold, if buying, consider EUR/JPY

CNH/JPY, USD/CNH

- Last Friday's close: USD/CNH 6.3576

- View: USD/CNH range-bound to lower; CNH/JPY range-bound to higher

- Expected range: USD/CNH 6.2500–6.4000

- Current positions: USD/CNH ±0.0, CNH/JPY ±2.0

- Maintain yuan buying

- If USD/CNH clearly breaks above 6.40, consider exiting

Please Note

Unauthorized reproduction or copying of any content published in this newsletter is prohibited. This newsletter is prepared solely for informational purposes, and its accuracy is not guaranteed by us or the information providers; the content may change due to changes in economic conditions. Users should use the information at their own risk and consult professionals in law, accounting, taxation, and other relevant areas for individual matters. If users suffer damages from using this information, we and the information providers do not bear any liability for such damages, regardless of cause.

× ![]()