Trading strategy considering dollar-buying pressure and risk sentiment [January 31–February 4]

Last week's FX range (variation range)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 113.67 | 113.49 | 115.69 | 115.24 | +1.38% |

| EUR/USD | 1.1343 | 1.1121 | 1.1345 | 1.1143 | ▲1.80% |

| EUR/JPY | 128.92 | 128.24 | 129.24 | 128.41 | ▲0.40% |

| USD/CNH | 6.3410 | 6.3235 | 6.3762 | 6.3670 | +0.41% |

| CNH/JPY | 17.9296 | 17.9209 | 18.1651 | 18.0865 | +0.88% |

Last week's FX market summary

USD/JPY

- Last week's USD/JPY started at 113.67. After a dip-stopper move earlier in the week, the USD/JPY remained solid at the start of the week. As the FOMC meeting approached, expectations for earlier tightening supported dollar buying, lifting USD/JPY back into the 114 area.At the notable FOMC, Powell signaled discussions on a March rate hike and balance sheet reduction, further tilting the market toward dollar buying.During the day on Thursday, USD/JPY breached 115, and by Friday rose to 115.69, closing the week at 115.24.

EUR/USD

- The euro started at 1.1343 against the dollar. Ahead of the FOMC, euro selling dominated as dollar strength prevailed, dipping below 1.1300 on Wednesday. With the FOMC in focus, the market shifted toward dollar buying, strengthening euro selling,and Thursday night clearly broke below the key support at 1.1210.By Friday it fell to 1.1121, then rebounded slightly to close at 1.1143.

USD/CNH

- The yuan started at 6.3410 per dollar. Following the week’s trend, yuan-buying dominated until the FOMC, with dollar selling and yuan buying pushing the pair to as low as 6.3235. After the FOMC, dollar strength pushed it above the 6.35 resistance, briefly to 6.3762, before closing at 6.3670.

What happened last week

※ Price indices and money statistics are year-on-year except where noted; GDP is quarter-on-quarter; indicators without special notes are month-on-month or current-month values24th

- Australia January Manufacturing PMI 55.3

- Germany January Manufacturing PMI 60.5

- Eurozone January Manufacturing PMI 59.0

- UK January Manufacturing PMI 56.9

- US January Manufacturing PMI 55.0

25th

- Australia December quarter CPI +3.5% (above the 2–3% target, signaling rising rate hikes)

- US November Case-Shiller Home Price Index +1.0%

- US January Conference Board Consumer Confidence 113.8

- US January Richmond Fed Manufacturing Index 8.0

- IMF cut its 2022 real GDP growth forecast to 4.4% from 4.9% in October 2021, citing prolonged high inflation in the US and COVID-19 containment in China; the report also notes geopolitics in Eastern Europe and East Asia with potential risk.Additionally, Germany's Chancellor Scholz and France's Macron warned Moscow that Russia would pay a high price if it invades Ukraine.

- Germany's Chancellor Olaf Scholz and France's President Emmanuel Macron warned that Russia would pay a high price if it resumes invasion of Ukraine.

- Chinese President Xi Jinping hosted an online meeting with leaders of five Central Asian countries to mark the 30th anniversary of diplomatic ties. With Central Asia central to the Belt and Road Initiative, China seeks to counter Russia's influence amid regional unrest such as in Kazakhstan.

26th

- Japan December Services CPI +1.1%

- US MBA Mortgage Applications -7.1%

- US December New Home Sales 810k

- FOMC kept near-zero policy rate and signaled future hikes.Per the December 2021 schedule, the Fed reiterated asset purchases would continue to taper and end by early March, with inflation running high and labor markets solid.The Fed also clarified the balance sheet reduction would begin after rate hikes. The committee published a set of principles guiding future decisions; the higher-level principle is that the federal funds rate is the primary tool to adjust monetary policy, and balance-sheet reduction would occur after rate hikes.

- Chile’s central bank hiked for the fifth consecutive meeting, raising the policy rate from 4.25% to 5.5% (increase of 1.25 percentage points to 1.5 percentage points).

- Bank of Canada kept the target for the overnight rate at 0.25%, noting significant improvement in the labor market and signaling further rate hikes; a March rate hike is possible.

27th

- US December Durable Goods Report -0.9%

- US prior week Initial Jobless Claims 260k

- US Q4 2021 GDP +6.9% (strong upside surprise)

- US Q4 PCE Core (Preliminary) +4.9%

28th

- Tokyo December CPI for metropolitan area +0.2%

- Australia December Producer Prices Index (PPI) +3.7%

- Germany Q4 GDP +24.0%

- US Q4 Employment Cost Index +1.0%

- US December PCE Deflator +5.8%

- Colombia central bank raises policy rate by 1 percentage point to 4%

- On the global stage, the yuan surpassed the Japanese yen to become the world’s fourth-largest reserve currency as of December 2021, due to ongoing yuan strength and increased overseas yuan-denominated bond investment.This marks the first time since August 2015, a 6 year 4-month period, that the yuan led the top reserve currency rankings. Background factors include continued yuan strength and foreign investment in yuan-denominated bonds.

Glossary of Economic Terms

- GDP = Gross Domestic Product: High growth is favorable

- CPI = Consumer Price Index: Many developed nations target around 2%

- PCE = Personal Consumption Expenditures: Personal consumption, highly correlated with consumer prices

- PPI = Producer Price Index: Influences CPI

- PMI = Purchasing Manager Index: 50 is the baseline

- ZEW = Leibniz Centre for European Economic Research: 0 is the baseline

- NAHB = National Association of Home Builders: 50 is the baseline

- Federal Reserve Bank of New York manufacturing index: 0 is baseline

- Philadelphia Fed manufacturing index: 0 is baseline

- Richmond Fed manufacturing index: 0 is baseline

- Chicago PMI: 50 is baseline

- University of Michigan Consumer Sentiment Index: indexed with 1966 = 100

- S&P/ Case-Shiller Home Price Index uses the 20-City Composite; important for gauging housing market impact

- Housing Permits Index: indexes the number of homes under contract but not yet settled

- Eurozone Consumer Confidence: indexed with 2000–2020 average set to 100

- Eurozone Economic Sentiment Indicator: indexed with 2000–2020 average set to 100

- Consumer Confidence Index: indexed with 1985 as 100

- Japan Leading Index: indexed with 2015 as 100

- Japan Watchers' Confidence Survey: 50 is baseline

- Japanese Corporate Leading Indicators: 0 is baseline

Key Economic Indicators and Political Events

31st

- 08:50 Japan December Industrial Production

- 19:00 Eurozone Q4 GDP

- 22:00 Germany January CPI

1st

- China春节 holiday begins (China is off until the 6th)

- 09:30 Australia December Retail Sales

- 12:30 Australia Reserve Bank policy rate announcement

- 16:00 Germany December Retail Sales

- 16:45 France January CPI

- 17:55 Germany January Unemployment Rate

- 18:00 Eurozone December Unemployment Rate

- 24:00 US January ISM Manufacturing PMI

- 24:00 US December JOLTS Job Openings

2nd

- 08:50 Japan January Monetary Base

- 19:00 Eurozone January CPI

- 22:15 US January ADP Employment

- 30:30 Brazil Central Bank Policy Rate

3rd

- 09:30 Australia December Building Approvals

- 09:30 Australia December Trade Balance

- 19:00 Eurozone December PPI

- 21:00 Bank of England Rate Decision

- 21:45 European Central Bank Policy Rate

- 22:30 Lagarde press conference

- 22:30 US Previous Week Initial Jobless Claims

- 22:30 US Q4 Nonfarm Productivity

- 24:00 US ISM Non-Manufacturing PMI

4th

- Opening ceremony of the Beijing Winter Olympics

- 09:30 Australia RBA Quarterly Monetary Policy Statement

- 16:00 Germany December Manufacturing New Orders

- 19:00 Eurozone December Retail Sales

- 22:30 Canada January Employment

- 22:30 US January Employment Report

Going forward

- March 5: National People's Congress

- March 10: ECB

- March 16: FOMC (with dot plot)

- March 18: Bank of Japan Policy Meeting

- April 14: ECB

- April 28: BOJ Policy Meeting (with economic and price outlook)

- May 4: FOMC

- June 9: ECB

- June 15: FOMC (with economic projections)

- June 17: BOJ Policy Meeting

- July 21: BOJ Policy Meeting (with economic and price outlook)

- July 21: ECB

- July 27: FOMC

- Sept 8: ECB

- Sept 21: FOMC (with economic projections)

- Sept 22: BOJ Policy Meeting

- Oct 27: ECB

- Oct 28: BOJ Policy Meeting (with economic and price outlook)

- Nov 2: FOMC

- Nov 8: US midterm elections

- Dec 14: FOMC (with economic projections)

- Dec 15: ECB

- Dec 20: BOJ Policy Meeting

Last Week's Currency Weakness/Strength

- Dollar buying continued last week (134/196 countries).After the FOMC, the market reacted with dollar buyingand is showing that trend.

- Among major currencies, the euro was sold off the most. In addition to dollar strength, issues such as Russia and Ukraine also cast a shadow.

- With USD/JPY rising sharply, cross-yen remained broadly firm.

- However currencies with独自 monetary policy, such as the South African rand and Australian dollar, saw selling pressure prevail.

- In summary, last week's currency strength/weakness was as followsUSD > CNY > JPY > EUR > SAR and AUD

Global Macro Environment (Latest)

- Equity markets continue to exhibit high volatility and unstable conditions.

- Specifically, last week the S&P 500 fear index briefly rose to 38.94.

- However, as the week ended, it calmed somewhat and fell to 27.66.

- Two main reasons market participants remain fearful are: expectations of early FED tightening and the Ukraine issue

- Regarding early tightening expectations, the FED's stance was clarified after last week's FOMC, suggesting a clearing of some ambiguity.

- Regarding Ukraine, a high-level meeting is planned in Berlin on February 9, so a rapid deterioration before then is unlikely.

- Against this backdrop, there seems to be a bit more calm returning to the market- or so it feels.

- Therefore, next week may lean toward a risk-off rebound.

- Additionally, Japanese monetary policy has not been much in focus so far, but given rising prices, attention is expected to increase, so we should monitor carefully.

- We will also continue to watch the U.S. Democratic Build Back Better bill.

S&P 500 Fear Index

Global Macro Environment (Supplement)

- About 87.6% of participants in the interest-rate futures market expect the first rate hike in the U.S. in March this year (25 bps).

- A portion (12.4%) expect a 50 bps rate hike in March this year.

- The rate-hike expectations arecentered around five hikes next year.

- However, beyond that, the pace of rate hikes is expected to slow.

- There are signs of a plateau in new COVID-19 cases (7-day moving average) (attached chart Daily New Cases).

- On the other hand, the 7-day moving average of new COVID-19 deaths has turned upward, which is noteworthy(attached chart Daily New Cases).

- While it is important to be mindful of rate hikes, we must also pay attention to the underlying factor of COVID.We should monitor it as well.

Market participants' FOMC rate-hike expectations, excerpt from CME Group

COVID-19 new cases, excerpt from Worldmeters

COVID-19 new deaths, excerpt from Worldmeters

Chart Analysis

USD Index (Daily)

- Dollar Index is a gauge of overall dollar strength (basket composition: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Broke above 96.90 resistance and surged upward

- In the near term, dollar buying momentum seems likely to strengthen

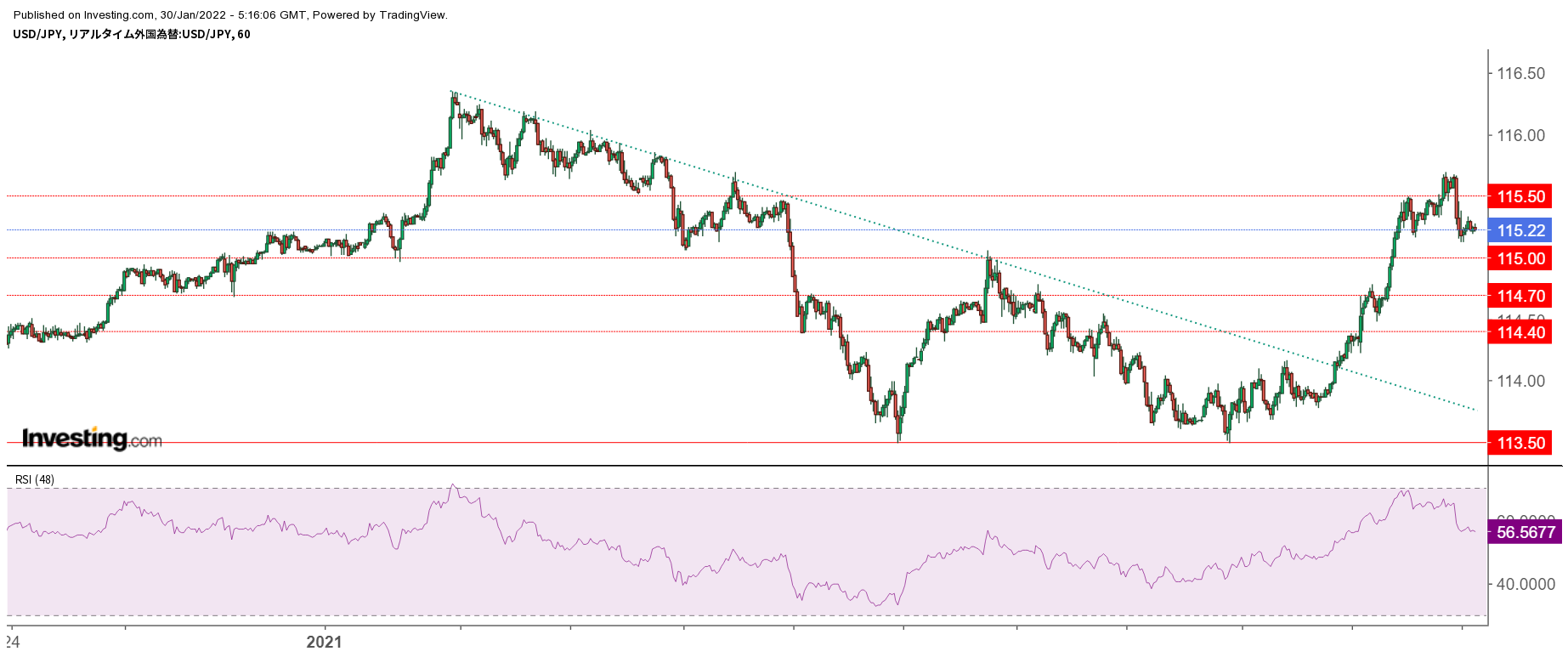

USD/JPY Medium-Term (Daily)

- The downside is gradually being raised, approaching last year's high of 116.35 yen

- If it breaks above, there is a high likelihood of a rapid move

USD/JPY Short-Term (Intraday)

- After breaking above the green trendline, it clearly moved higher

- First, watch whether 115.00 yen holds as support this week

- Continuing to follow the upside would be prudent

EUR/USD Medium-Term (Daily)

- Downward trend (green line) is continuing

- Break below 1.1210 support strengthens the downward momentum

EUR/USD Short-Term (Intraday)

- In the short term, technical indicators (RSI) suggest oversold conditions, but be wary of a potential continued decline

USD/CNH Medium-Term (Daily)

- After breaking below 6.35, there is a rebound, but the trend remains downward

- Deemed as temporary yuan weakness

USD/CNH Short-Term (Intraday)

- If a rebound continues, the upside targets are near 6.3790 and then 6.4000

This Week's Toda's Trading Strategy

Overall Policy

- Be mindful that volatility could remain elevated

- By watching moves in equities and cryptocurrencies, gauge market participants' sentiment

- Assume the forex market will continue with dollar buying

- Use dips to buy dollars and take partial profits on declines

USD/JPY

- Last Friday's close: 115.24

- View: ranging to upside

- Expected range: 114.70–116.35

- Current position: USD/JPY +2.0

- Maintain dollar-buying posture

- Continue dip-buying strategy

EUR/USD, EUR/JPY

- Last Friday's close: EUR/USD 1.1143

- View: EUR/USD flat to down, EUR/JPY flat

- Expected range: EUR/USD 1.1050–1.1210

- Current positions: EUR/USD ± 0 EUR/JPY ±0

- Sell on rallies

- At the start of the week, discuss overall positions and lean toward euro selling and dollar buying

CNH/JPY, USD/CNH

- Last Friday's close: USD/CNH 6.3386

- View: USD/CNH flat, CNH/JPY flat to higher

- Expected range: USD/CNH 6.2500–6.4000

- Current positions: USD/CNH ± 0.0 CNH/JPY ± 2.0

- Maintain yuan buying

- If USD/CNH decisively breaks above 6.40, consider exiting

Important Notes

All content published in this newsletter is prohibited from being reproduced or copied without permission. This newsletter is prepared solely for information purposes and does not guarantee its accuracy by our company or the information providers; content may change due to changes in economic conditions. Use the information at your own risk and consult professionals in law, accounting, and taxes for individual matters. If a user incurs damages from using this information, our company and the information providers do not bear liability for any reason.

× ![]()