Trading strategy considering high volatility and FOMC [January 24 – January 28]

Last Week's Foreign Exchange Range (Volatility)

| Opening Value | Low | High | Closing Value | Change | |

|---|---|---|---|---|---|

| USD/JPY | 114.18 | 113.60 | 115.06 | 113.68 | ▲0.44% |

| EUR/USD | 1.1413 | 1.1300 | 1.1435 | 1.1340 | ▲0.64% |

| EUR/JPY | 130.29 | 128.54 | 131.18 | 128.91 | ▲1.06% |

| USD/CNH | 6.3582 | 6.3355 | 6.3643 | 6.3386 | ▲0.31% |

| CNH/JPY | 17.9580 | 17.8962 | 18.1190 | 17.9179 | ▲0.22% |

Last Week's Foreign Exchange Summary

USD/JPY

- Last week's dollar-yen started at 114.18 yen per dollar. The early-week rebound continued, with a gradual rise. When reports suggested possible BoJ rate-hike discussions within the central bank, it was said there were “no such talks at all,” and the rate briefly climbed into the 115 yen territory. Governor Kuroda also dismissed the rumors at a press conference. However, as the rally faded and risk-off sentiment grew due to weakness in U.S. stocks, the yen strengthened. On Friday it fell below 114.00, and over the weekend it dropped to 113.60, closing at 113.68.

EUR/USD

- The euro started at 1.1413 dollars per euro. With the market broadly risk-off and dollar demand rising, the euro declined gradually. It broke below 1.1400 on Wednesday and tested lower levels, but buying interest around 1.1300 helped some recovery, closing the week near 1.1340.Even in a downtrend, it appeared to hold its ground.

USD/CNH

- The yuan started at 6.3582 per dollar. Early in the week, easing in the reserve requirement or policy anxieties kept the yuan near the 6.35 level. By the weekend, yuan buying dominated, briefly breaking below 6.35 and sliding to 6.3355, before closing at 6.3386.A trend toward yuan strength was evident.

Highlights from Last Week

※ Inflation and money supply are year-on-year comparisons; GDP is quarter-on-quarter; indicators without special notes are month-on-month or current-month figures17th

- U.S. holiday (Martin Luther King Jr. Day)

- Japan November machinery orders +3.4%

- China 10-12 quarter GDP: 2021 growth 8.1%; 2020-2021 two-year growth 5.1%

- China December retail sales +0.6%

18th

- Eurozone January ZEW Economic Sentiment Indicator 49.4 (strong)

- January New York Fed Manufacturing Index -0.7 (very weak)

- Brazil reported record daily Covid-19 cases: 132,254

- BoJ Governor Kuroda said in a press conference that future rate-hike discussions were “not being considered at all.”The Outlook Report noted a scenario where cost-push price pass-through could accelerate inflation, making the 2% inflation target seem distant.The achievement of the target is “quite distant.”

- Prime Minister Kishida spoke at the online “Davos Agenda.” He said Japan would mobilize citizens' efforts and investments to overcome weaknesses in climate, digital, and other areas of the economy, aiming to strengthen those sectors.

19th

- UK December CPI +5.4% (inflation rising rapidly)

- Germany December CPI +5.3%

- South Africa December CPI +5.9%

- US December housing starts -0.1%

- US December building permits +9.1% (US housing-related indicators generally positive)

- Canada December CPI +4.8%

- Turkey announced a currency swap deal with the UAE worth 64 billion lira (about 5400 billion yen). The lira has fallen substantially against the dollar in 2021, but President Erdogan dislikes high interest rates, and seeks to stabilize the lira via currency swaps, fiscal measures, and regulatory steps.

- WHO released results of an emergency committee on COVID-19. It advised member states to lift or ease travel restrictions related to COVID-19, citing lack of value and economic/social burdens.

- President Biden held a White House press conference, indicating Russian President Putin is likely to invade Ukraine again in 2022. He said, “In my estimation, he will invade.” If an invasion occurs, the U.S. is considering stopping dollar settlements through Russian banks.

20th

- PBOC announced LPR: 5-year LPR down 0.05% to 4.60%; 1-year LPR down 0.10% to 3.70%

- Australia December employment: +361,000; unemployment rate 4.2% (very strong)

- Germany December PPI +24.2%

- Eurozone December CPI +5.0%

- Turkey Central Bank kept policy rate at 14.0%

- U.S. previous week initial jobless claims 286,000

- January Philadelphia Fed manufacturing index 23.2

- U.S. December existing home sales -4.6%

21st

- Japan December CPI +0.8% (some upside risk)

- U.S. December Conference Board Leading Economic Index +0.8%

Glossary of Economic Terms

- GDP = Gross Domestic Product: higher growth is good

- CPI = Consumer Price Index: many advanced economies target 2%

- PCE = Personal Consumption Expenditures: closely related to consumer prices

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Manager Index: 50 is the baseline

- ZEW = Leibniz Centre for European Economic Research: 0 is baseline

- NAHB = National Association of Home Builders: 50 is baseline

- NY Fed Manufacturing Index: 0 baseline

- Philadelphia Fed Manufacturing Index: 0 baseline

- Richmond Fed Manufacturing Index: 0 baseline

- Chicago Purchasing Managers Index: 50 baseline

- University of Michigan Consumer Sentiment Index: indexed with 1966=100

- S&P/ Case-Shiller Home Price Index: “20-CMS Home Price Index” is commonly used. Important for monitoring the housing market’s impact on the economy.

- Pending Home Sales Index: contracts signed but not yet closed, indexed

- European Consumer Confidence Index: 100 is the mean for 2000-2020; releases compare to previous month

- Eurozone Economic Sentiment Index: 100 is the mean for 2000-2020; releases are actual values

- Consumer Confidence Index: indexed with 1985=100

- Japan’s Coincident Economic Index: indexed with 2015=100

- Japan’s Tankan Survey: 50 is baseline

- Japan Corporate Sector Confidence Survey: 0 is baseline

Key Economic Indicators and Political Events

24th

- WHO Executive Board meeting (23–29)

- 07:00 Australia January Manufacturing PMI

- 17:30 Germany January Manufacturing PMI

- 18:00 Eurozone January Manufacturing PMI

- 18:30 UK January Manufacturing PMI

- 23:45 US January Manufacturing PMI

25th

- 09:30 Australia Q4 CPI

- 23:00 US September Case-Shiller US Home Price Index

26th

- Australia Holiday (Australia Day)

- 08:50 Japan December Corporate Services Price Index

- 14:00 Japan November Economy Watchers Survey

- 21:00 US MBA Mortgage Applications

- 24:00 US December New Home Sales

- 28:00 FOMC

27th

- 22:30 US Q4 2022 GDP (Quarterly, Real)

- 22:30 US December PCE Deflator (QoQ)

28th

- 16:00 Germany Q4 GDP

- 22:30 US December PCE Deflator

Beyond Next Week

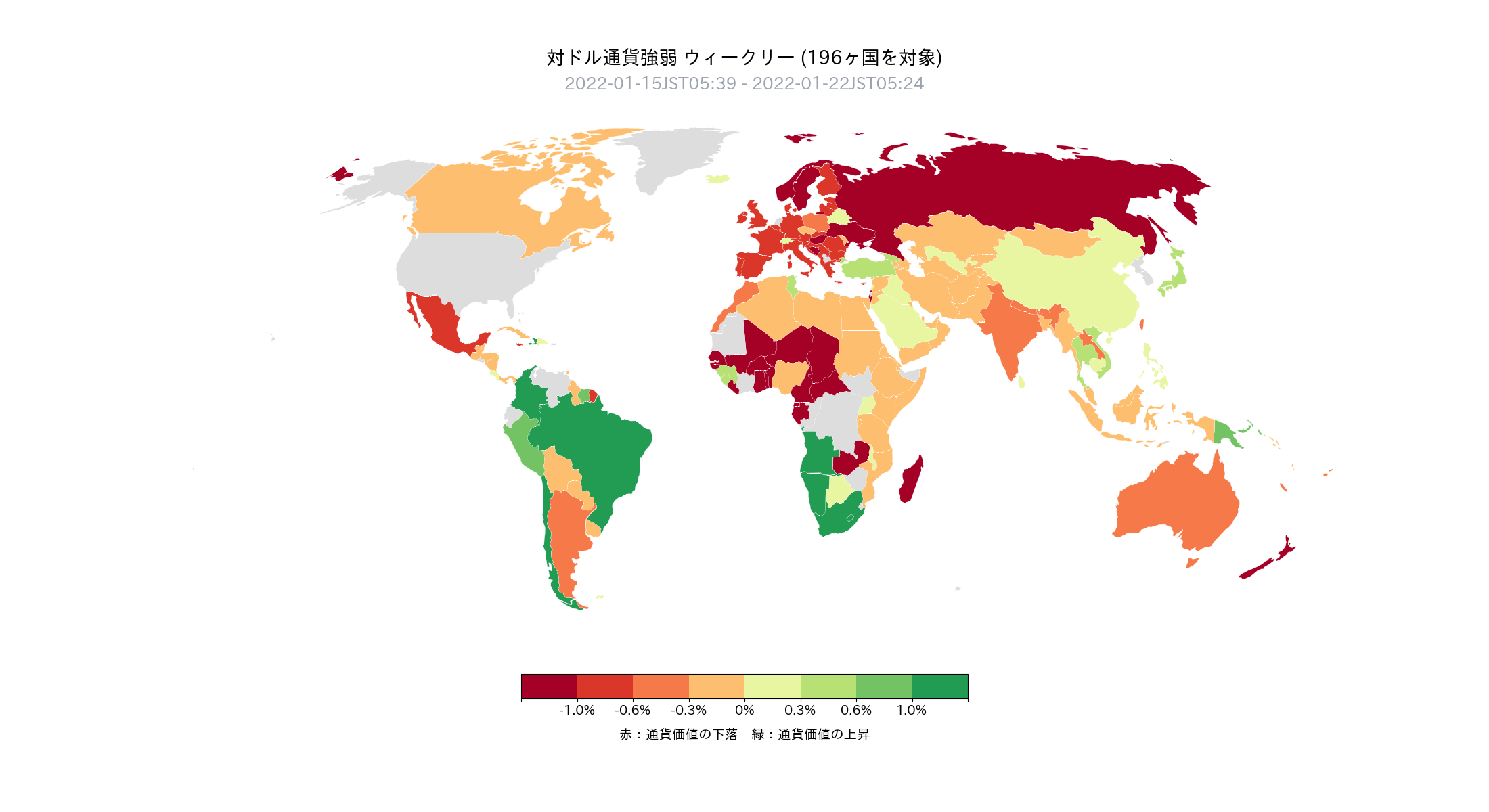

Currency Strength Last Week

- Last week the dollar strengthened (151/196 countries)

- U.S. stocks fell and risk-off mood intensified, with the dollar being bought against various currencies

- Against the backdrop of Russia-Ukraine issues, European and Nordic currencies weakly moved

- For currencies such as Turkey and South Africa where selling had run its course, buying to cover was favored

- In summary, last week’s currency strength/weakness was as followsEmerging market currencies that have seen selling run its course > Japanese yen > Chinese yuan > U.S. dollar > Euro > Russian ruble

Global Macro Environment—Latest

- The risk-off mood continues to prevail in the market

- Main reasons are expectations of earlier U.S. rate hikes and balance sheet normalization

- Furthermore, Russia’s Ukraine progression plan casts a shadow over European currencies

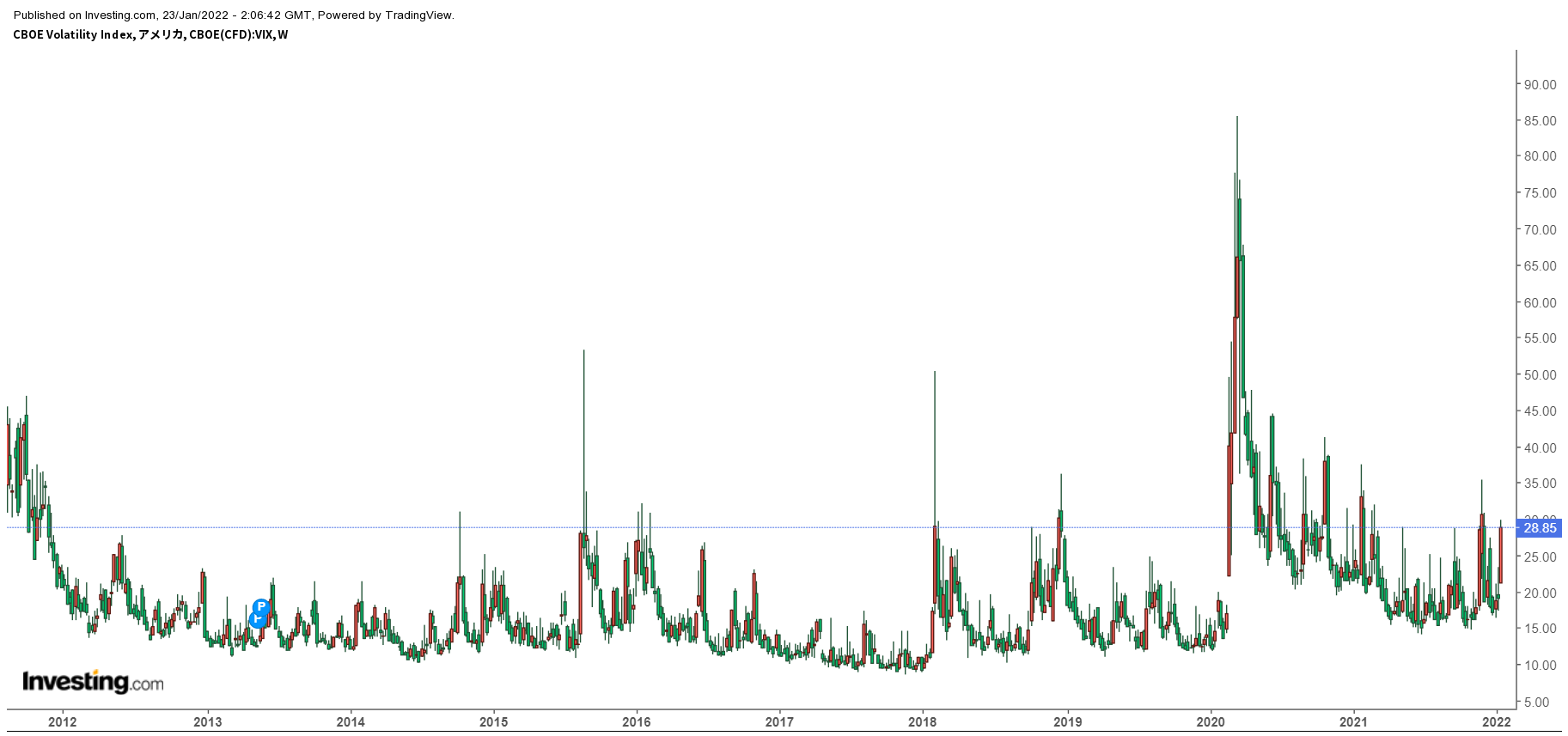

- As a resultInvestors’ risk appetite deteriorated markedly, with NASDAQ-100 fear index in the 30s and S&P 500 fear index in the 20sHowever, we believe it will not rise to such extreme levels this time

- A L-shaped shock like Lehman or Omicron could push it to the 80s, but we judge that won’t happen this time

- The reason is that the shock stems from financial normalization, not from a deteriorating economy, which is a major difference

- Therefore we are approaching the bottom with a sense that the market is nearing a trough

- Fear indices above 30 are often a buying opportunity, but we should consider 40–50 as a worse-case scenario

- Attached below is a 10-year chart of the S&P 500 fear index, showing that 40–50 has been a buying zone

- Additionally, regarding Japan’s monetary policy, it has not been a major focus until now, but given rising prices we expect it to attract more attention and will watch carefully

- We will continue to watch the U.S. Democratic Build Back Better bill

Global Macro Environment—Supplement

- 89% of futures market participants expect the U.S. rate hike to begin in March this year (25 bps), up from last week

- A 50 bps rate hike is unlikely in the near term.If I were a policymaker, I would consider it a foolish move that could overly impact the market.

- U.S. rate hike expectationsCenter around five hikes next yearas the baseline

- However, the pace of hikes beyond that is expected to ease

- The daily new COVID-19 cases (7-day moving average) continue to surge (attached chart: Daily New Cases)

- The daily new deaths (7-day moving average) have also turned upward(attached chart: Daily New Cases)

Chart Analysis

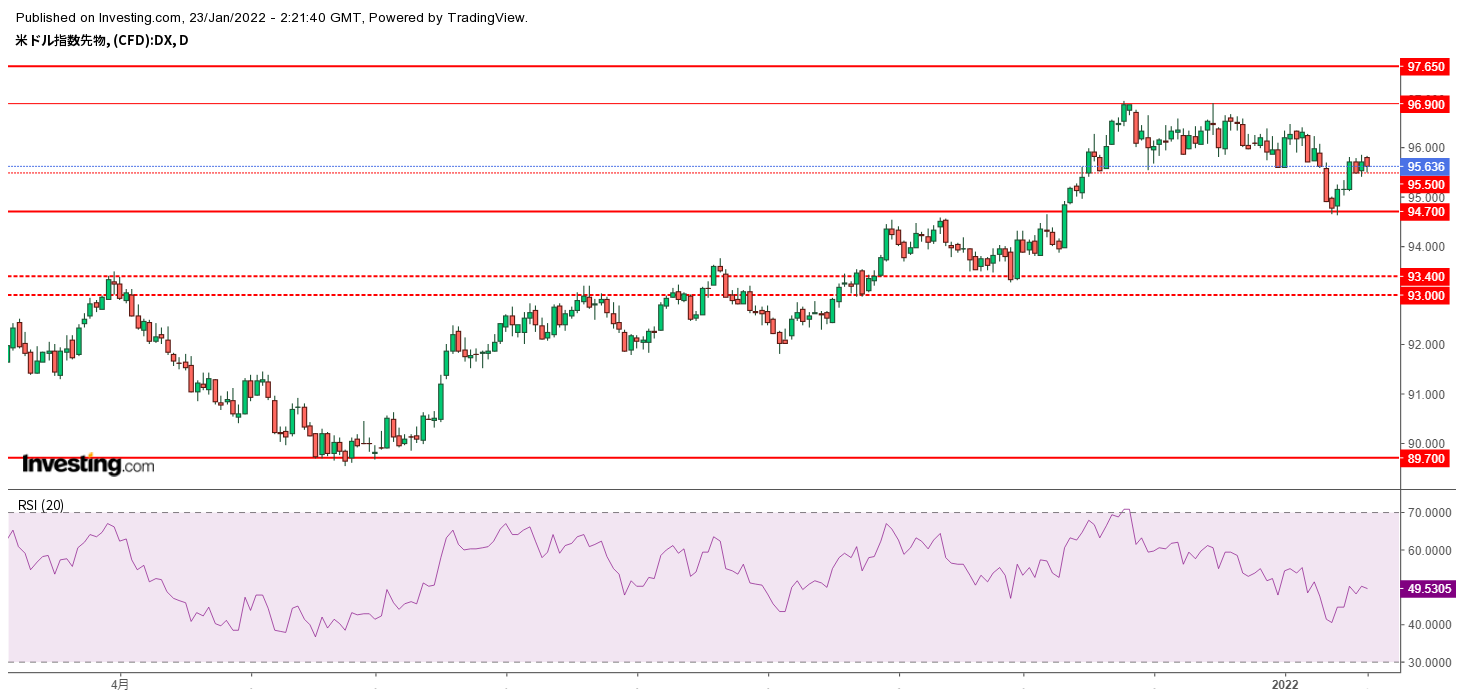

USD Index (Daily)

- Dollar Index is an overall gauge of dollar strength (basket components: EUR57.6%, JPY13.6%, GBP11.9%, CAD9.1%, SEK 4.2%, CHF 3.6%)

- After finding support at 94.70, it broke above the prior support at 95.50 and closed at 95.64

- First, expect the 94.70–96.90 range to continue

USD/JPY Medium-Term (Daily)

- Near-term focus is whether it rebounds at 113.50

- If it breaks below, the cushions are 113.50 and 112.70

- In particular, 112.70 is notable as the retracement level of the move from 109.00 to the recent high of 116.35

- If it clearly breaks below 112.70, we will exit long positions

USD/JPY Short-Term (Intraday)

- First, watch whether it can hold at 113.50 this week

- Since the dollar-yen showed signs of a bottoming on the week’s end, there may be some rebound potential at the start of next week

EUR/USD Medium-Term (Daily)

- It has returned below the 1.1370 resistance

- The green trend line initially broke above but has returned downward again

- Need to determine whether the downtrend has endedand should consider the possibility of further downdrafts driven by dollar strength

EUR/USD Short-Term (Intraday)

- The 1.1370 resistance remains in focus

USD/CNH Medium-Term (Daily)

- Clear break below 6.3500

- Continuing to hold long USD/CNH is prudent

USD/CNH Short-Term (Intraday)

- Buying USD and selling CNH around 6.35 could work

This Week’s Toda Trading Strategy

Overall Policy

- Overall risk-off environment with high market volatility

- ThereforeAim to take small profits both on the upside and downside to capture weekly gains

- Consider starting to position in risk assets such as equities and crypto, as the bottom may be near

USD/JPY

- Last Friday close: 113.68

- View: range-bound

- Expected range: 112.50–115.00

- Current position: USD/JPY around zero

- As a precaution against further downside, plan to buy on dips

- If it clearly breaks below 112.70, exit long USD/JPY

EUR/USD, EUR/JPY

- Last Friday close: EUR/USD 1.1340

- View: EUR/USD sideways, EUR/JPY sideways

- Expected range: EUR/USD 1.1210–1.1480

- Current positions: EUR/USD ± 0 EUR/JPY ± 0

- Be mindful of 1.1370 and the aforementioned trendline

- If it breaks upward, follow with a buy

CNH/JPY, USD/CNH

- Last Friday close: USD/CNH 6.3386

- View: USD/CNH flat to down, CNH/JPY flat to up

- Projected range: USD/CNH 6.2500–6.3800

- Current positions: USD/CNH ± 0.0 CNH/JPY ± 2.0

- Maintain CNH buying

- If it clearly breaks above 6.35, consider exiting

Important Notes

All content published in this newsletter is strictly for information purposes and may not be reproduced or copied without permission. The accuracy of the information is not guaranteed by our company or the information providers, and the contents may change due to changes in economic conditions. Users should use the published information at their own risk and consult professionals in law, accounting, and taxation for individual matters. If users suffer damages from using this information, our company and the information providers shall not be liable for any damages regardless of the cause.

× ![]()