Translate the following HTML to English, keep HTML format, do not use Markdown code blocks or add line breaks, and decode entities before translating: Original: ドル売りの背景と各チャートポイントを考慮したトレード戦略【1月17日~1月21日】 Translation: Trade strategy considering the back

Last Week's Foreign Exchange Range (Volatility Range)

| Opening Value | Low | High | Closing Value | Change | |

|---|---|---|---|---|---|

| USD/JPY | 115.64 | 113.48 | 115.86 | 114.20 | ▲1.24% |

| EUR/USD | 1.1353 | 1.1285 | 1.1484 | 1.1414 | +0.54% |

| EUR/JPY | 131.20 | 129.77 | 131.48 | 130.35 | ▲0.65% |

| USD/CNH | 6.3863 | 6.3403 | 6.3863 | 6.3555 | ▲0.48% |

| CNH/JPY | 18.0954 | 17.8480 | 18.1628 | 17.9602 | ▲0.75% |

Last Week's Foreign Exchange Summary

USD/JPY

- Last week's dollar/yen began at 115.64. When Powell, Chair of the Federal Reserve, signaled a expectation of balance sheet reduction later in the year, markets had priced in too much early balance sheet tightening and dollar selling surged. Dollar selling dominated, and on Wednesday the pair fell below 115 to around 114.50, then continued lower. Into the weekend, despite reports of possible early rate hikes by the Bank of Japan (unverified), there was further selling and it briefly reached 113.48, but buying recovered and the week closed at 114.20.

EUR/USD

- The euro started at 1.1353 dollars per euro. Early in the week it faced resistance at the 1.1370 range top and briefly dropped to 1.1285. However, as the dollar sold off following Powell's remarks, the euro recovered, surpassed the upper bound 1.1370 and moved beyond 1.14, reaching as high as 1.1484 by the weekend. The weekend closed at 1.1416 as dollar buying resumed.

USD/CNH

- The yuan started at 6.3863 per dollar. The yuan gradually recovered; it slipped to the 6.37s on Tuesday and the 6.36s on Wednesday, and on Friday briefly dipped below 6.3403. The weekend closed at 6.3579.

Events of Last Week

Note: Price and money statistics are year-over-year for price indices; GDP is quarter-on-quarter; indicators without specific notes are month-on-month or current-month figures.10th

- Japan: Coming-of-age holiday

- Australia: November building approvals (MoM) +3.6%

- Denmark: December CPI +3.1%

- Norway: December CPI +5.3%

- Turkey: November unemployment 11.2%

- Euro-area: November unemployment 7.2%

- US and Russia governments agreed to continue talks on the tense Ukraine situation. The gaps over the European security framework proposed by Russia in December 2021 remain unresolved, and further discussions with NATO et al. will proceed from the 12th onward.

11th

- Australia: November trade balance AUD 9.423 billion (strong)

- Australia: November retail sales +7.3% (strong)

- Japan: November in-dex: Leading index 103, Coincident index 93.6

- Turkey: November current account -$2.681 billion

- Brazil: December CPI +10.06%

- Government announced re-entry for foreigners with residence permits from 11 African countries including South Africa, and also Zimbabwe, Namibia, DRC. Previously entry was largely refused. Effective from 0:00 on the 12th.

- Powell, Fed Chairtestified before the Senate committee, saying "Inflation is a serious threat" and signaled proceeding with monetary tightening to curb it.Among Fed officials, discussion of starting rate hikes in March is gathering momentum, and a path toward shrinking assets via quantitative tightening (QT) in the second half of the year is being outlined.

12th

- Japan: November international balance of payments — current account +$89.73 billion; trade balance -$43.13 billion (trade deficit persists)

- China: December CPI +1.5% (inflation cooling)

- China: December PPI +10.3% (inflation cooling)

- Japan: December Economy Watchers Survey — DI (Current) 56.4; DI (Expected) 49.4

- India: December CPI +5.59%

- US: December CPI +7.0% (Inflation remains high)

- Russia: December CPI +8.4%

- US: December monthly budget deficit -$2.13 billion

- The Federal Reserve (Fed) released the Beige Book, noting that the economy expanded moderately in late 2021 and that supply chain bottlenecks and labor shortages continued to constrain growth, while inflation and wages continued to rise.

- Russia's Southern Military District announced more than 10,000 troops participated in drills on the Crimea and other southern regions; conducted firing and tank exercises across 20+ training grounds, Tass reported.

- NATO held talks with Russia on the Ukraine situation. After the talks, NATO Secretary General Jens Stoltenberg acknowledged substantial differences, but emphasized the need for ongoing dialogue.

13th

- Japan: December M2 money stock YoY +3.7%

- US: December PPI +9.7%

- US: Initial jobless claims for week ending December 31: 230k

- Fed Governor Lael Brainard testified before U.S. Senate committee, saying the high inflation is a major concern and that the next steps would bring policy rate back toward a normal level as asset purchases end in March. She and other officials indicated a rapid pace of tightening was likely.

- CSTO peacekeeping forces deployed in Kazakhstan began withdrawal

14th

- China: December trade balance $944.6 billion (second-biggest ever)

- Japan: December domestic corporate goods price index +8.5%

- Sweden: December CPI +3.9%

- EU: November trade balance -€150 million

- US: December retail sales -1.9% (slight weakness)

- US: December industrial production -0.1% (slight weakness)

- US: January University of Michigan consumer sentiment 68.8 (weak)

- Federal Reserve Bank of New York President Williams said in a virtual talk that "the next step to tighten policy is to gradually raise the policy rate from its current very low level toward a normal level," noting signs of a strong labor market.

Glossary of Economic Terms

- GDP = Gross Domestic Product: higher growth is considered good

- CPI = Consumer Price Index: many advanced economies target around 2%

- PCE = Personal Consumption Expenditures: closely related to consumer prices

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Managers' Index: 50 is the benchmark

- ZEW = Leibniz Centre for European Economic Research: 0 is the baseline

- NAHB = National Association of Home Builders: 50 is the benchmark

- NY Fed manufacturing index: 0 is the baseline

- Philadelphia Fed manufacturing index: 0 is the baseline

- Richmond Fed manufacturing index: 0 is the baseline

- Chicago Purchasing Managers Index: 50 is the baseline

- University of Michigan Consumer Sentiment Index: indexed to 1966 = 100

- S&P/ Case-Shiller Home Price Index widely used: 20-Ccity home price index; important for monitoring housing's impact on the economy

- Pending home sales index: contracts signed but not yet closed

- European Consumer Confidence Index: indexed to 100 for 2000–2020 average

- European Economic Sentiment Index: indexed to 100 for 2000–2020 average

- Consumer Confidence Index: indexed to 100 for 1985

- Japan: Economic Watchers' Indicators: 50 is the baseline

- Japanese Corporate Confidence Survey: 0 is the baseline

- Japanese Coincident Economic Index: indexed to 100 for 2015

Notable Economic Indicators and Political Events

17th

- US holiday (Martin Luther King Jr. Day)

- Davos Forum (January 17–21)

- 08:50 Japanese November Machinery Orders

- 11:00 China Q4 2022 domestic product (Q4 10-12)

- 11:00 China December Retail Sales

18th

- Time TBD: Bank of Japan Monetary Policy Meeting

- 15:30 BOJ Governor Kuroda's regular press conference

- 19:00 Euro Area January ZEW Economic Sentiment

- 22:30 January NY Fed Manufacturing Index

19th

- 16:00 UK December CPI

- 16:00 Germany December CPI

- 17:00 South Africa December CPI

- 22:30 US December housing starts

- 22:30 US December building permits

- 22:30 Canada December CPI

20th

- People's Bank of China to announce LPR (Loan Prime Rate)

- 09:30 Australia December employment statistics

- 16:00 Germany December PPI

- 19:00 Eurozone December CPI

- 20:00 Turkey central bank policy rate

- 22:30 US week ending initial jobless claims

- 22:30 January Philadelphia Fed Manufacturing Index

- 24:00 US December Existing Home Sales

21st

- 08:30 Japan December CPI

- 08:50 BoJ meeting minutes

- 24:00 US December Leading Economic Index

Beyond Next Week

- January 26: FOMC

- February 3: ECB

- February 4: Beijing Winter Olympics opening

- March 5: National People's Congress

- March 10: ECB

- March 16: FOMC (with Economic Projections)

- March 18: BoJ Monetary Policy Meeting

- April 14: ECB

- April 28: BoJ Monetary Policy Meeting (outlook for economy and inflation)

- May 4: FOMC

- June 9: ECB

- June 15: FOMC (with Economic Projections)

- June 17: BoJ Monetary Policy Meeting

- July 21: BoJ Monetary Policy Meeting (outlook for economy and inflation)

- July 21: ECB

- July 27: FOMC

- September 8: ECB

- September 21: FOMC (with Economic Projections)

- September 22: BoJ Monetary Policy Meeting

- October 27: ECB

- October 28: BoJ Monetary Policy Meeting (outlook for economy and inflation)

- November 2: FOMC

- November 8: US midterm elections

- December 14: FOMC (with Economic Projections)

- December 15: ECB

- December 20: BoJ Monetary Policy Meeting

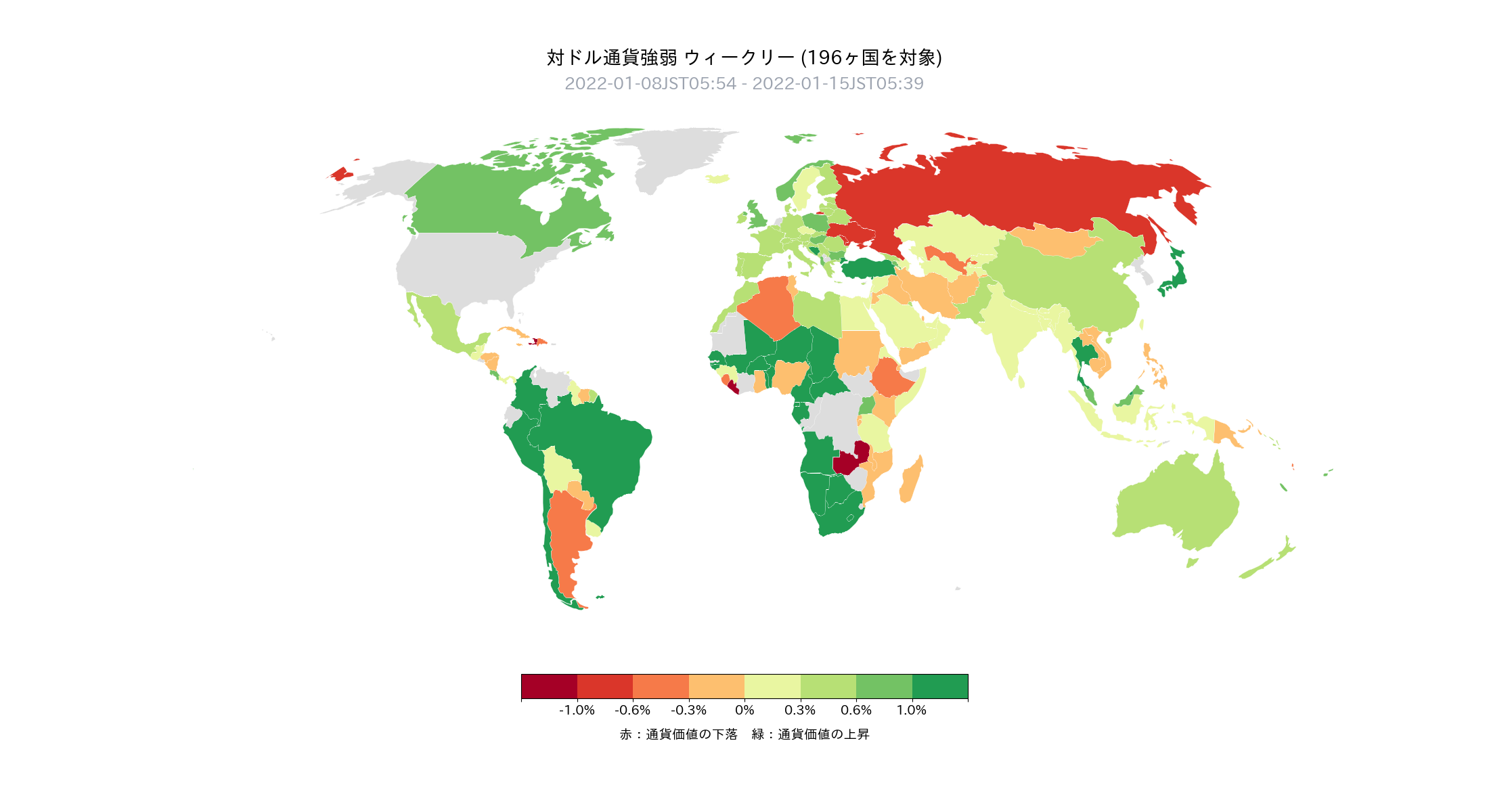

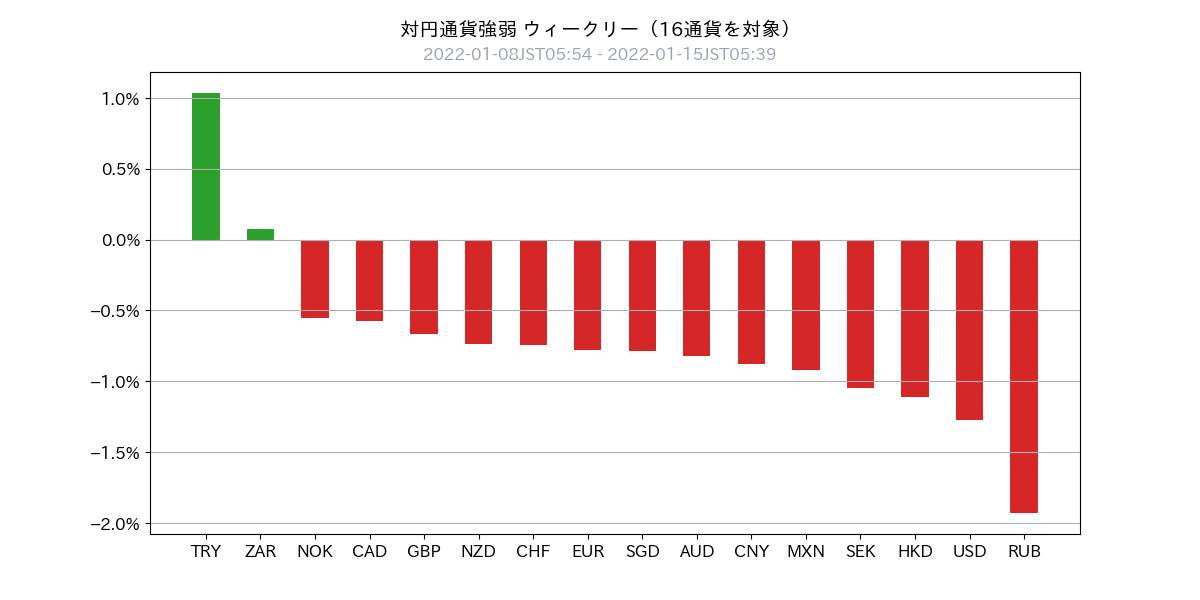

Last Week's Currency Strength

- Last week, the dollar was sold off across 147/196 countries. This was supported by inflation-control factors such as Powell's remarks that balance sheet reduction will come later in the year, and signs of easing in Chinese price increases. United States economic data also appeared weak, contributing to the trend.

- With the dollar being sold, so-called emerging market currencies such as the Brazilian real, South African rand, and Turkish lira were bought firmly

- Russia continued to be pressured by geopolitical factors such as the deteriorating Crimea situation and confrontations with NATO, influenced by those events

- In advanced economies, oil-producing countries like Norway and the United Kingdom, as well as New Zealand, that have raised rates, were bought

- The yen was temporarily favored, but emerging market currencies were being bought, appearing unusual

- In summary, last week's currency strength was as followsEmerging markets such as Turkey and South Africa > Oil-producing countries of Norway & UK > Japanese yen > New Zealand that tightened policy > Euro > Chinese yuan > US dollar > Russian ruble

Global Macro Environment (Latest Version)

- Attention-grabbingIn the testimonies of the Fed Chair and Vice Chair to Congress, it was confirmed that inflation measures are prioritized, that early rate hikes are likely, and that balance-sheet reduction is expected in the latter part of the year.

- Looking at global economic indicators, there is evidence that China’s price pressures are easing and US economic indicators show a mild plateau.

- In such an environment, US stock markets have been soft, FX has seen dollar selling, and emerging market currencies have been bought back.

- This is not a “risk-off” market where participants fear something, but rather a situation where extreme expectations of US rate hikes and monetary easing have faded

- From here, will there be a renewed focus on a “strong America,” or will the focus shift to other topicsA time to assess the marketseems likely

- Japanese monetary policy has not been a major focus until now, but given price increases, attention is expected to rise, and we should watch carefully

- We will continue to monitor the U.S. Democratic Build Back Better bill

Global Macro Environment (Supplement)

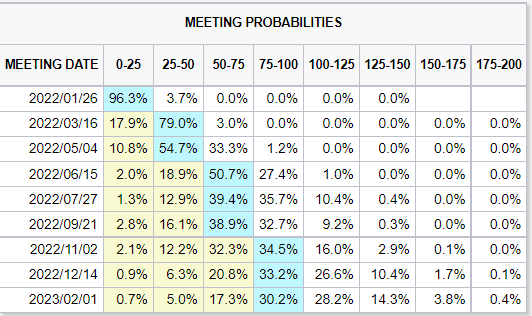

- 79% of interest-rate futures market participants expect US rate hikes to begin by March this year (up from last week)

- US rate-hike expectationscentered on three hikes next yearwith a lower likelihood of further hikes priced in beyond the near term

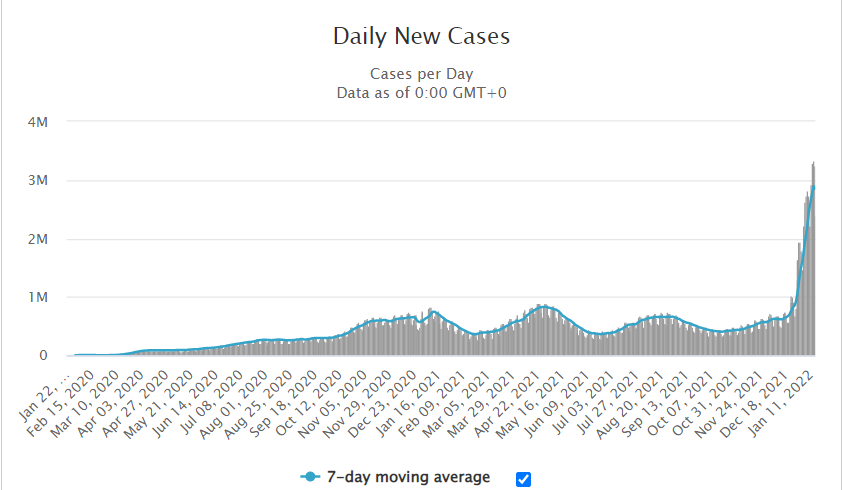

- The trend of new coronavirus cases (7-day moving average) is still rising rapidly (attached chart Daily New Cases)

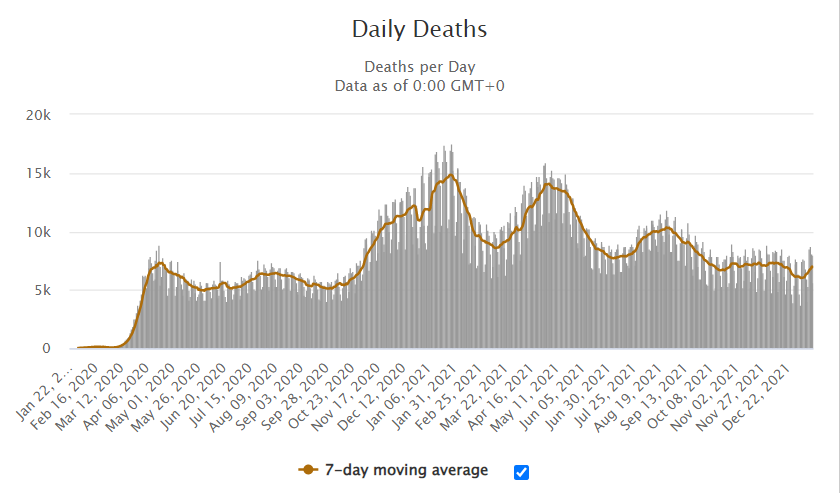

- The trend of new coronavirus deaths (7-day moving average) is starting to rise slightly (attached chart Daily New Cases)

Market participants' FOMC rate-hike expectations, excerpt from CME Group

New COVID-19 cases, excerpt from Worldmeters

New COVID-19 deaths, excerpt from Worldmeters

Chart Analysis

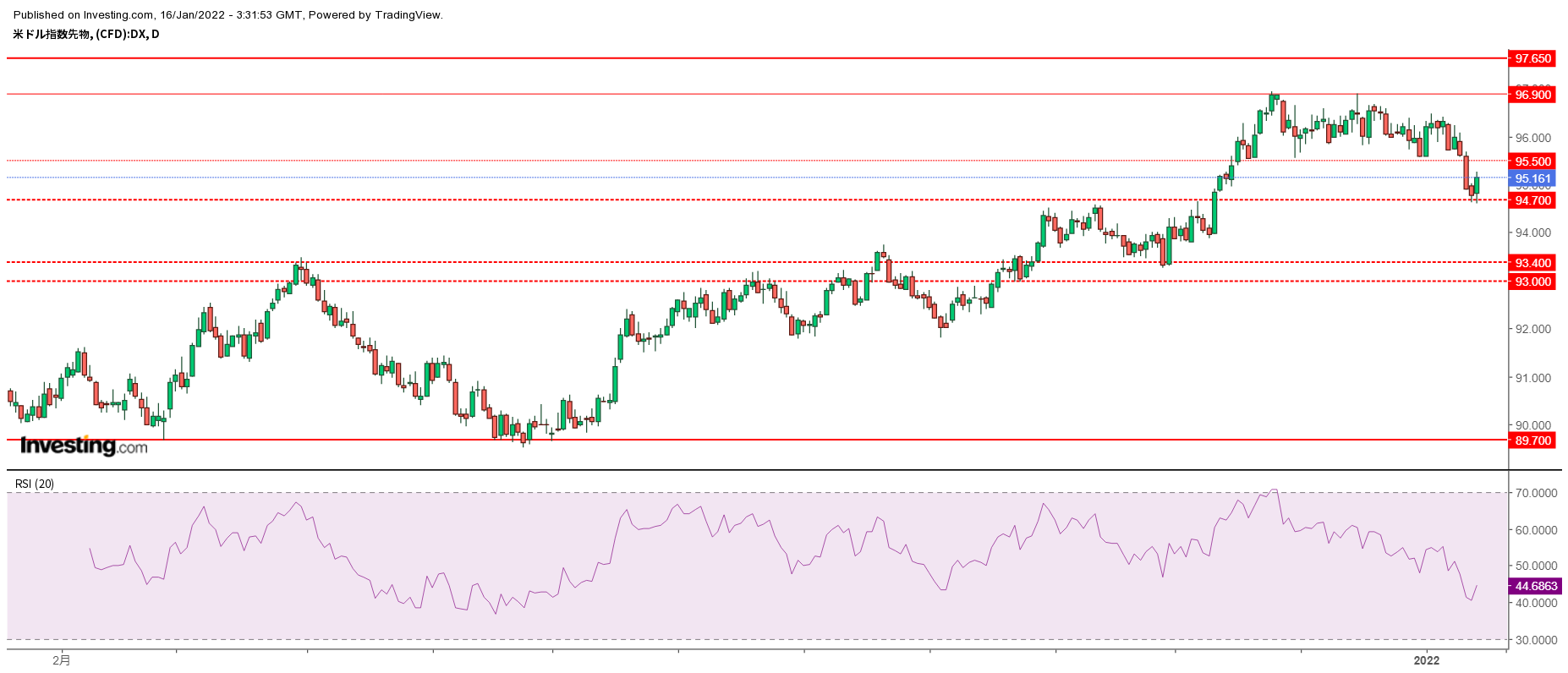

USD Index (Daily)

- Dollar Index is an indicator of overall dollar strength (basket composition: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Broke the 95.50 support and found support at 94.70 (initial expectation: 94.70–95.50 range)

- Monday's session expected to see a dollar rebound

USD/JPY Mid-term (Daily)

- Dropped sharply below 115.50, 115.00, and 114.40

- Rebounded at 113.50

- If 112.70 is clearly breached to the downside, we will exit long positions

USD/JPY Short-term (Hourly)

- First, watch whether 114 is held this week

- A sharp reversal is unlikely, but a gradual bottoming and return to an uptrend is expected

EUR/USD Mid-term (Daily)

- Clear breakout above 1.1370 resistance

- Pay attention to the possibility of breaking above the green trendline

- It is safe to assume the downtrend has ended for now

EUR/USD Short-term (Hourly)

- Buy-and-hold around 1.1400 appears to be a straightforward strategy

- Regardless of whether it rises, the bottom is likely to be solid

USD/CNH Mid-term (Daily)

- Range of 6.3500–6.4000 continues

- On a daily basis, it has tested below 6.35 several times, indicating strengthening yuan depreciation pressure

USD/CNH Short-term (Hourly)

- In the short term, near the lower end of the range, so watch for rebounds

This Week's Todo's Trading Strategy

Overall Policy

- Market does not seem to be in risk-off mode

- FX: “buy euro, buy yuan, sell yen”

- US stocks: buy-the-dip approach

- Cut losses early, sell at the top of the range, buy at the bottom

USD/JPY

- Last Friday's close: 114.20

- View: sideways to slightly higher

- Expected range: 113.50–115.50

- Current position: USD/JPY +3.0

- Be wary of further downside while maintaining dollar-long exposure

- If 112.70 clearly breaks to the downside, exit dollar-long positions

EUR/USD, EUR/JPY

- Last Friday's close: EUR/USD 1.1414

- View: EUR/USD range-bound to higher; EUR/JPY range-bound to higher

- Expected range: EUR/USD 1.1370–1.1530

- Current positions: EUR/USD ± 0; EUR/JPY ± 0

- Breakout above the range to the upside suggests buying into the start of the week

- If it reverses and falls below 1.1370 again, exit early

CNH/JPY, USD/CNH

- Last Friday's close: USD/CNH 6.3555

- View: USD/CNH sideways to down, CNH/JPY sideways to up

- Expected range: USD/CNH 6.3000–6.4000

- Current positions: USD/CNH ± 0.0; CNH/JPY ± 2.0

- Strong yuan buying pressure, expect dips below 6.35 and hold yuan-buying positions

- If 6.40 is breached to the upside, exit

Important Notices

Unauthorized reproduction or copying of any content published in this newsletter is prohibited. This newsletter is prepared solely for information provision, and its accuracy is not guaranteed by us or the information sources. The published content may change due to changes in economic conditions. Use the information at your own risk and consult professionals in law, accounting, and tax for individual matters. If users suffer damages from using this information, our company and the information sources are not liable for compensation regardless of cause.

× ![]()