Trading Strategy Considering U.S. Monetary Tightening [January 10–January 14]

Last Week's FX Range (Volatility Range)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 115.10 | 114.96 | 116.36 | 115.55 | +0.39% |

| EUR/USD | 1.1365 | 1.1272 | 1.1381 | 1.1368 | +0.03% |

| EUR/JPY | 130.86 | 130.02 | 131.63 | 131.25 | +0.30% |

| USD/CNH | 6.3599 | 6.3491 | 6.3979 | 6.3792 | +0.30% |

| CNH/JPY | 18.0935 | 18.0527 | 18.2456 | 18.1050 | +0.06% |

Last Week's FX Summary

USD/JPY

- Last week's dollar-yen moved starting at 115.10. After briefly testing 115.00 on Monday’s New York session, it held firm. On Tuesday during Asia hours, it decisively surpassed last year’s high near 115.50, then in the U.S. session breached 116.00 and reached the weekly high of 116.36 yen. On Wednesday in the U.S. session, ahead of the FOMC minutes, profit-taking dominated and the pair drifted lower. The minutes suggested early rate hikes and balance sheet reduction, and with U.S. stocks falling, the dollar-yen continued to slide, closing around 115.55 by week’s end.

EUR/USD

- The euro started at 1.1365 dollars per euro. Early in the week euro selling dominated, dipping under 1.1300 on Monday’s New York session. On Tuesday, while USD/JPY was making new highs, the euro briefly hit a weekly low of 1.1272. However, with the FOMC minutes imminent, euro buys recovered, back to the 1.1340s. After the minutes, initial euro selling and dollar buying gave way to euro gains toward the end of the week, closing near 1.1368, roughly the level at the start of the week.

USD/CNH

- The yuan began at 6.3599 per dollar. Early in the week, dollar selling and yuan strength prevailed, with the yuan falling to as low as 6.4391. Later, as the FOMC minutes circulated, dollar demand recovered, with USD/CNH rebounding toward the 6.40 area (6.3979 highs). In the end, selling pressure eased and the pair closed at 6.3792.

What Happened Last Week

Note: Price indices and monetary statistics are year-over-year, GDP is quarter-on-quarter; indicators without specific notes are month-over-month or current-month figures.3rd

- Japan, China, Australia, New Zealand, UK, Canada, Russia markets closed

- Turkey December CPI +36.1% (very strong inflation pressure)

- Eurozone December PMI manufacturing 58.0

- U.S. December PMI manufacturing 57.7

- Finland highlights NATO accession rights in a speech by President Niinistö. Russia is withholding talks with the U.S. about halting NATO expansion to support its security policy.

- Hong Kong Exchange suspended trading of Evergrande shares at company’s request, stating it would halt trading until disclosure of information

4th

- New Zealand, Russia markets closed

- China December Caixin Manufacturing PMI 50.9

- France December CPI +2.8%

- Germany December unemployment rate 5.2%

- UK December manufacturing PMI 57.9

- U.S. December ISM Manufacturing Index 58.7 (not a bad read)

- U.S. November JOLTS job openings 10.56 million

- Xi’an, Shaanxi Province, Chinareported about 42,000 people under quarantine as of the 4th due to COVID-19 spread. The city’s population is about 13 million.Since December 23 of last year, lockdowns have continued with no clear end date.

- Chinese government bans online religious proselytizing as of 2022 MarchReligious activities online via social media and fundraising will be restricted. Authorities aim to tighten control ahead of the autumn Communist Party Congress.

- In Fort de France near Marseille, France, by the 4th at least 12 people contracted a new COVID-19 variant; whether it is more infectious or deadly than Omicron remains unknown.

5th

- Russia markets closed

- U.S. December ADP employment +87k

- FOMC minutes from December 2021 suggested possible rate hikes as early as March 2022 and balance sheet reduction details.

- Kazakhstan President Tokayev accepted government resignation amid protests over LPG price spikes; capital Almaty saw government facilities attacked and presidential residence reportedly occupied.

- Kazakhstan extended emergency on nationwide basis amid protest spreads; CSTO troops reportedly deployed per Interfax citing national TV

- Singapore to standardize three-dose vaccination; booster required within nine months or vaccination status no longer recognized

- Hong Kong Chief Executive Carrie Lam bans entry from eight countries from 8th, dining indoors after 6 p.m., closes theme parks and bars to curb Omicron spread

- Tesla showroom in Xinjiang, China, opened late 2021; U.S. cites genocide concerns; human rights groups criticize Tesla

6th

- Russia markets closed

- China December Caixin Services PMI 53.1

- Germany December CPI +5.3% (strong inflation pressure)

- U.S. November Trade Balance -$80.2B

- U.S. initial jobless claims for the previous week 207k

- U.S. December ISM Non-Manufacturing PMI 62.0

- Central Asia's Kazakhstan raised policy rate to 3% for inflation controlThis is the sixth consecutive rate hike; aims to curb overheating due to rising food/fuel prices and commodity demand.

- North Korea announced it will not participate in the Beijing Winter Olympics, continuing political motives amid pandemic and U.S. actions

- U.S. Secretary of Defense Austin discussed with Russian Defense Minister Shoigu to de-escalate risk in Ukraine and avoid military confrontation, per Pentagon

- U.S. 10-year Treasury yield rose to about 1.75%, the highest in roughly nine months

7th

- Russia markets closed

- Tokyo December CPI in metropolitan areas +0.5%

- Germany November industrial production -0.2%

- Germany November trade balance +€12.0B

- Euro area November retail sales +1.0%

- Euro area December CPI +5.0% (high inflation pressures in eurozone)

- U.S. December employment report: Nonfarm payrolls +199k, unemployment rate 3.9% (overall solid)

- Canada December employment +547k, unemployment 5.9%

- Mexico INEGI reports December consumer price index +7.36% YoY

- St. Louis Fed President Daly said Fed should slowly tighten policy and move toward balance sheet reduction faster than previous normalization cycle; expect 1–2 rate hikes before balance sheet adjustment

- Kazakhstan protests across the country escalated, government forces detained over 3,800; Russian-led CSTO peacekeepers began to deploy

- Thailand freezes quarantine exemptions for entrants as new Omicron variant spreads

Glossary of Economic Terms

- GDP = Gross Domestic Product: high growth is good

- CPI = Consumer Price Index: many advanced economies target around 2%

- PCE = Personal Consumption Expenditures: closely related to consumer prices

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Manager Index: 50 is neutral

- ZEW = Leibniz Centre for European Economic Research: 0 is baseline

- NAHB = National Association of Home Builders: 50 is baseline

- NY Fed Manufacturing Index: 0 is baseline

- PHilly Fed Manufacturing Index: 0 is baseline

- Richmond Fed Manufacturing Index: 0 is baseline

- Chicago PMI: 50 is baseline

- University of Michigan Consumer Sentiment Index: index with 1966=100

- S&P/Case-Shiller Home Price Index: widely used "20-Ccity" index; key for housing market trends

- Pending Home Sales Index: contracts signed but not yet closed

- Euro area Consumer Confidence Index: index with 2000–2020 average set to 100

- Euro area Economic Sentiment Indicator: index with 2000–2020 average set to 100

- Consumer Confidence Index: index with 1985=100

- Japan Leading Economic Index: index with 2015=100

- Japan Coincident/Coordination: "Watchers" survey: 50 is baseline

- Japan Corporate Goods Price Index: 0 is baseline

Key Economic Indicators and Political Events

10th

- Japan Holiday (Coming of Age Day)

- U.S.-Russia Strategic Stability Dialogue (Geneva)

- 09:30 Australia November Building Permits (MoM)

- 16:00 Denmark December CPI

- 16:00 Norway December CPI

- 16:00 Turkey November unemployment rate

- 19:00 Eurozone November unemployment rate

11th

- 09:30 Australia November Trade Balance

- 09:30 Australia November Retail Sales

- 14:00 Japan November Economy Watchers

- 16:00 Turkey November current account

- 21:00 Brazil December CPI

- 24:00 Powell Chair of the Fed nominee hearing

12th

- NATO-Russia Council framework for dialogue (Brussels)

- 08:50 Japan November International Balance of Payments

- 10:00 Kuroda speaks, BoJ Governor

- 10:30 China December CPI

- 10:30 China December PPI

- 14:00 Japan December Economy Watchers

- 21:00 India December CPI

- 22:30 U.S. December CPI

- 25:00 Russia December CPI

- 28:00 U.S. December Budget Balance

- 28:00 Fed regional economic reports

13th

- 08:50 Japan December Money Stock M2 YoY

- 22:30 U.S. December PPI

- 22:30 U.S. Previous week's initial jobless claims

- 24:00 Brainerd FOMC Vice Chair nomination hearing

14th

- 12:00 China December Trade Balance

- 08:50 Japan December Domestic Corporate Goods Price Index

- 17:30 Sweden December CPI

- 19:00 Euro area November Trade Balance

- 22:30 U.S. December Retail Sales

- 23:15 U.S. December Industrial Production

- 24:00 U.S. January University of Michigan Consumer Confidence

Week Ahead

- Jan 17–21: Davos World Economic Forum

- Jan 26: FOMC

- Feb 3: ECB

- Feb 4: Beijing Winter Olympics opening

- Mar 5: NPC (National People's Congress)

- Mar 10: ECB

- Mar 16: FOMC (with Economic Projections)

- Mar 18: BoJ Monetary Policy Meeting

- Apr 14: ECB

- Apr 28: BoJ Monetary Policy Meeting (with Economic/Inflation Outlook)

- May 4: FOMC

- Jun 9: ECB

- Jun 15: FOMC (with Economic Projections)

- Jun 17: BoJ Monetary Policy Meeting

- Jul 21: BoJ Monetary Policy Meeting (with Economic/Inflation Outlook)

- Jul 21: ECB

- Jul 27: FOMC

- Sep 8: ECB

- Sep 21: FOMC (with Economic Projections)

- Sep 22: BoJ Monetary Policy Meeting

- Oct 27: ECB

- Oct 28: BoJ Monetary Policy Meeting (with Economic/Inflation Outlook)

- Nov 2: FOMC

- Nov 8: U.S.-China midterm elections

- Dec 14: FOMC (with Economic Projections)

- Dec 15: ECB

- Dec 20: BoJ Monetary Policy Meeting

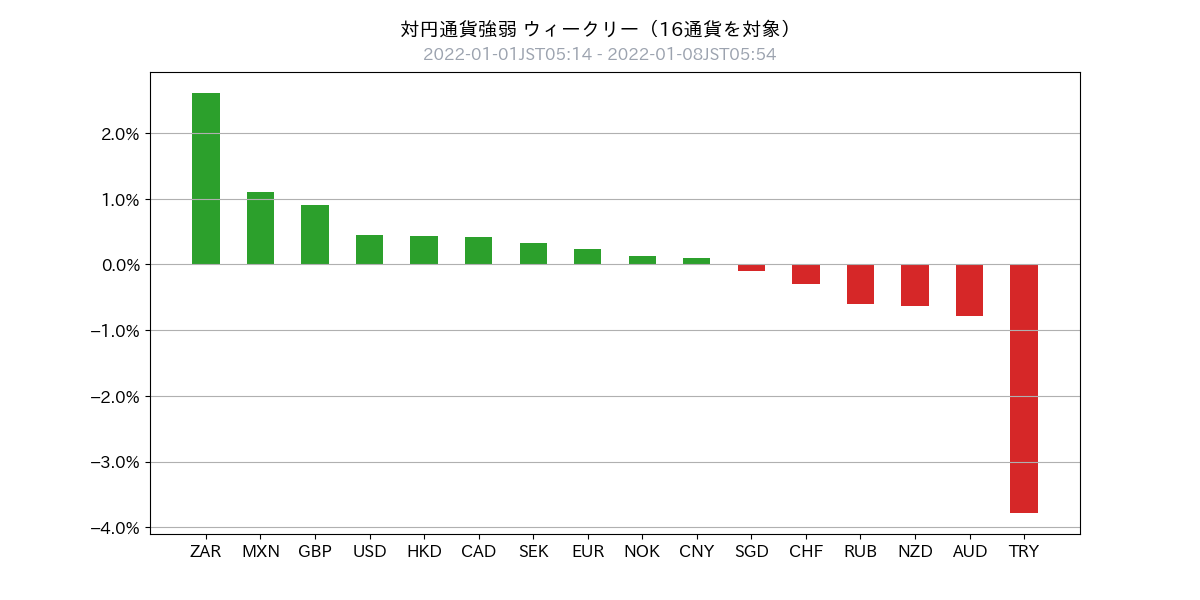

Last Week's Currency Strength

- Last week, currencies moved in a patchwork fashion

- Russia saw selling pressure, perhaps due to the tense Crimea situation and protests in Kazakhstan

- Australia faced selling pressure, perhaps due to the diverging monetary policy stance with the United States

- Mexico, where inflationary pressures are rising, showed buying strength

- South Africa, where Omicron had peaked, was also bought back

- In advanced economies, Britain, where Omicron had peaked, was also bought

- In summary, last week's currency strength was as followsCountries where Omicron peaked > US Dollar > Euro > Renminbi > Japanese Yen > Russian Ruble > Australian Dollar > Turkish Lira

Global Macro Environment (Latest)

- Last week, concerns about early rate hikes by the Fed and balance sheet reduction led to a decline in US stocks

- Bond yields rose sharply, with 5-year bonds at 1.50% and 10-year bonds at 1.76% (bond sell-off)

- As the Fed heads toward asset reduction, investor risk appetite becomes clearer, and markets are unlikely to see assets rise uniformly as before

- As a result, market difficulty appears to have heightened significantly

- On the other hand, the Omicron variant's impact has been relatively straightforward on the market

- It is notable that currencies whose impact has peaked are being repurchased

- The Turkish Lira continues to fall, which remains a risk-off factor to watch

- The outlook for the U.S. Democratic Party's Build Back Better act is another element of uncertainty

- Returning to fundamentals, it is important to carefully examine monetary policy and trade on the basis of those differences

Global Macro Environment (Supplement)

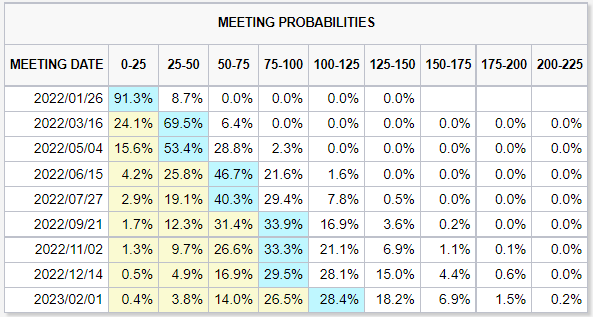

- About 70% of participants in the interest rate futures market expect the U.S. rate hike to begin in March this year (up from last week)

- Meanwhile, expectations for U.S. rate hikes arethree times next yearas the central tendency (last week it was four hikes, so the overall rate-hike pricing has declined; rather, balance sheet reduction is considered)

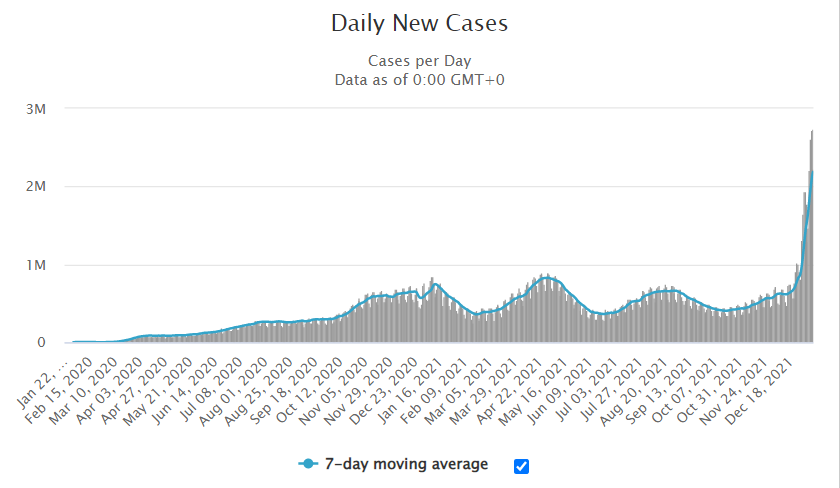

- The number of new COVID-19 cases (7-day moving average) continues to rise sharply (attached chart Daily New Cases)

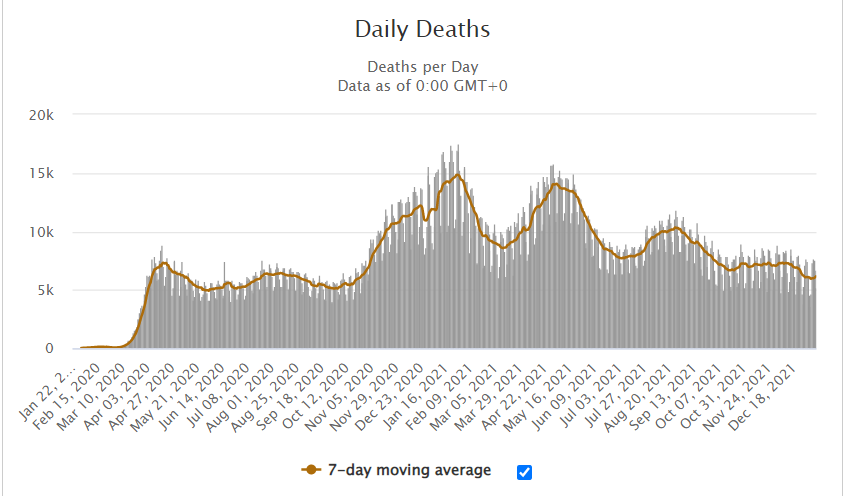

- Conversely, the trend in new COVID-19 deaths (7-day moving average) is downward, indicating overall reduced impact from COVID (attached chart Daily New Cases).

Market participants' FOMC rate-hike expectations, excerpt from CME Group

New COVID-19 infections, excerpt from Worldometers

New COVID-19 deaths, excerpt from Worldometers

Chart Analysis

USD Index (Daily)

- Dollar Index = a gauge of overall dollar strength (basket composition: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Continuing in a dollar-strengthening environment, it remains in a range of 95.50 to 96.90

- The current level is near the lower end of the range, viewed as a dollar pullback

USD/JPY Medium-Term (Daily)

- Broke above the 2021 high of 115.50

- Next target is the 2016 high of 118.60

- The primary driver is yen weakness; focus on the Bank of Japan's moves

- Fundamentally, it is preferable to enter on a buying trend

USD/JPY Short-Term (Intraday)

- Backed by 115.50 and 115.00, look to buy on dips to hold long positions

EUR/USD Medium-Term (Daily)

- It remains on a downside path, trading in a range of 1.1210–1.1370

- Recent activity shows buying pressure, but momentum is lacking

- Continue to target a decisive breakout above 1.1370 and go long on the euro

EUR/USD Short-Term (Intraday)

- 1.1370 has temporarily been breached, but a full breakout above is premature

- Consider placing stops around 1.1410 and focus on downside moves

USD/CNH Medium-Term (Daily)

- Range of 6.3500–6.4250 continues

- In the medium-to-long term, the yuan remains strong

USD/CNH Short-Term (Intraday)

- Ultimately upside move from about 6.35

- Currently trading in a narrow range of 6.3790–6.4000

- Range-bound trading is prudent

This Week's Toda Strategy

Overall Policy

- Focusing on a “dollar-buying” stance for currencies

- Continue to sell at the top of the range and buy at the bottom

- Reassess equities and other risk assets from individual names and rethink from a clean slate

USD/JPY

- Last Friday close: 115.55

- View: range-bound to slightly higher

- Expected range: 115.00–116.50

- Current position: USD/JPY around zero

- At the start of the week, enter by buying first

- Would like to add to longs around the 115.00 level

- As a core position, plan to hold about 2.0 lots long

EUR/USD, EUR/JPY

- Last Friday close: EUR/USD 1.1368

- View: EUR/USD is flat to down, EUR/JPY flat

- Expected range: EUR/USD 1.1280–1.1410

- Current positions: EUR/USD ±0, EUR/JPY ±0

- Expect a rebound near 1.1370, so start building a short position at the start of the week

- Place a stop at 1.1410 and aim for a downside move with favorable risk-reward

- For downside protection, consider partial take-profit around 1.1300

CNH/JPY, USD/CNH

- Last Friday close: USD/CNH 6.3792

- View: USD/CNH flat to up, CNH/JPY flat to up

- Expected range: USD/CNH 6.3500–6.4250

- Current positions: USD/CNH ± 0.0, CNH/JPY ± 0.0

- Around 6.40 and 6.4250, shorting on a near-term basis may work

- However, as U.S. interest rates rise, the U.S.–China rate gap may narrow, reducing the attractiveness of the yuan (high yield)

- Thus, adopt a wait-and-see approach

Notes

× ![]()