Trading strategy considering Omicron’s mildness and the level of the Dollar Index [January 3–January 7]

Last Week's FX Range (Volatility)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 114.38 | 114.31 | 115.21 | 115.08 | +0.61% |

| EUR/USD | 1.1318 | 1.1273 | 1.1387 | 1.1368 | +0.44% |

| EUR/JPY | 129.46 | 129.35 | 131.06 | 130.82 | +1.05% |

| USD/CNH | 6.3740 | 6.3350 | 6.3794 | 6.3611 | ▲0.21% |

| CNH/JPY | 17.9426 | 17.9323 | 18.1642 | 18.0844 | +0.79% |

Last Week's FX Summary

USD/JPY

- Last week's dollar-yen around 114.38 started. With trading thin around year-end, risk-on continued at the start of the week, and USD/JPY maintained an upward path. Late Tuesday near 115, on Wednesday it jumped into the 115 range, briefly dipped to the 114.60s but quickly rebounded, and in the latter part of the week settled in the 115 range. The week closed at 115.08 after extending to 115.21.

EUR/USD

- The euro started at 1.1318 per euro. The early week was range-bound, but Wednesday saw strong dollar buying and briefly dipped below 1.1280. Later that day, amid a euro-cross rally, there was a sharp rebound to around 1.1350, with choppy moves and no clear trend. By the end of the week, euro buying resumed within the cross-yen uptrend, peaking at 1.1387 before closing at 1.1371.

USD/CNH

- The yuan began at 6.3740 per dollar. The range-bound week saw limited liquidity, but flows of substantial yuan buying emerged toward year-end, pushing briefly below 6.34. Later, some pullback left the pair at 6.3611 at close.

Last Week's Highlights

Note: Price index and money supply figures are year-on-year, GDP is quarter-on-quarter, and indicators without specific notes are month-on-month or current period values27th

- Australia, New Zealand, Canada, UK markets holiday

- Over 2,500 flights canceled globally (including about a thousand due to U.S. origin/destination), with many delays. Causes cited include spread of the Omicron variant. From Christmas Eve on the 24th for three days, global flight cancellations exceeded 6,000, sharply impacting year-end travel.

28th

- Australia, New Zealand, Canada, UK markets holiday

- China Evergrande reportedly did not make a payment on its USD-denominated bonds totaling $255.2 million

- Japan November industrial production +7.2%

- U.S. October Case-Shiller home price index +18.4% (year-over-year)

- U.S. December Richmond Fed manufacturing index 16

- Global COVID-19 vaccine doses reached 9.02 billion; as Omicron spread and developed nations push boosters, vaccine access in low-income countries, especially Africa, remains a challenge.

29th

- U.S. November Pending Home Sales +2.2%

- Russia December CPI +8.4%

30th

- U.S. initial unemployment claims 198,000 (week)

- Putin and Lukashenko to hold joint military exercises in Belarus in spring 2022

- J&J said its updated COVID vaccine booster reduced hospitalization risk by 85%

31st

- LIBOR to be discontinued

- Many countries in holiday or early close (Japan, Korea, Germany, etc.)

- China December PMI 50.3

Glossary of Economic Terms

- GDP = Gross Domestic Product: high growth is positive

- CPI = Consumer Price Index: many advanced economies target 2%

- PCE = Personal Consumption Expenditures: consumer spending; highly correlated with CPI

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Manager Index: 50 is the threshold

- ZEW = Leibniz Centre for European Economic Research: 0 is the baseline

- NAHB = National Association of Home Builders: 50 is the baseline

- New York Fed manufacturing index: 0 is the baseline

- Philadelphia Fed manufacturing index: 0 is the baseline

- Richmond Fed manufacturing index: 0 is the baseline

- Chicago PMI: 50 is the baseline

- University of Michigan Consumer Sentiment Index: indexed with 1966 = 100

- S&P/Case-Shiller Home Price Index commonly uses 20-CM House Price Index; important for gauging housing market impact on the economy

- Pending home sales index: contracts signed but not yet closed

- Euro area consumer confidence index: indexed to 100 as average 2000-2020; preliminary releases shown as MoM

- Eurozone sentiment index: indexed to 100 as average 2000-2020; releases show actual values

- Consumer confidence index: indexed with 1985 = 100

- Japan coincident index: indexed with 2015 = 100

- Japan Watchers survey: 50 is the baseline

- Japan corporate survey: 0 is the baseline

Key Economic Indicators and Political Events

3rd

- Japan, China, Australia, New Zealand, UK, Canada, Russia holidays

- 16:00 Turkey December CPI

- 18:00 Eurozone December Manufacturing PMI

- 23:45 U.S. December Manufacturing PMI

4th

- New Zealand, Russia holidays

- 10:45 China December Caixin Manufacturing PMI

- 16:45 France December CPI

- 17:55 Germany December unemployment rate

- 18:30 UK December Manufacturing PMI

- 24:00 U.S. December ISM Manufacturing PMI

- 24:00 U.S. November JOLTS

5th

- Russia holiday

- 18:00 Eurozone December Services PMI

- 22:15 U.S. December ADP Employment

- 23:45 U.S. December Services PMI

- 28:00 FOMC minutes

6th

- Russia holiday

- 10:45 China December Caixin Services PMI

- 22:00 Germany December CPI

- 22:30 U.S. November Trade Balance

- 22:30 U.S. prior week initial jobless claims

- 24:00 U.S. December ISM Non-Manufacturing PMI

7th

- Russia holiday

- 08:30 Tokyo metropolitan area December CPI

- 16:00 Germany November Industrial Production

- 16:00 Germany November Trade Balance

- 19:00 Eurozone November Retail Sales

- 19:00 Eurozone December CPI

- 22:30 U.S. December Employment Data

- 22:30 Canada December Employment

Next Week and Beyond

- Jan 17–21: World Economic Forum in Davos

- Jan 18: Bank of Japan Monetary Policy Meeting (outlook for economy and prices)

- Jan 26: FOMC

- Feb 3: ECB

- Feb 4: Beijing Winter Olympics opens

- Mar 5: National People's Congress

- Mar 10: ECB

- Mar 16: FOMC (with economic projections)

- Mar 18: BoJ Monetary Policy Meeting

- Apr 14: ECB

- Apr 28: BoJ Monetary Policy Meeting (outlook for economy and prices)

- May 4: FOMC

- Jun 9: ECB

- Jun 15: FOMC (with economic projections)

- Jun 17: BoJ Monetary Policy Meeting

- Jul 21: BoJ Monetary Policy Meeting (outlook for economy and prices)

- Jul 21: ECB

- Jul 27: FOMC

- Sep 8: ECB

- Sep 21: FOMC (with economic projections)

- Sep 22: BoJ Monetary Policy Meeting

- Oct 27: ECB

- Oct 28: BoJ Monetary Policy Meeting (outlook for economy and prices)

- Nov 2: FOMC

- Nov 8: U.S. midterm election results

- Dec 14: FOMC (with economic projections)

- Dec 15: ECB

- Dec 20: BoJ Monetary Policy Meeting

Currency Strength Last Week

- Dollar selling was dominant last week as well (117/196 countries)

- But the dollar/yen rose due to even stronger-selling yen

- Cross yen strengthened across the board, supported by a risk-on mood

- In some emerging markets such as Russia and South Africa, selling dominated

- The Turkish lira rebounded and rose on government deposit-protection measures, but recently selling has regained the lead(Risk-off factors)

- In summary, last week's currency strength was as followsCurrencies> Euro > CNY > USD > JPY > Russia & South Africa > Turkish lira

Global Macro Environment (Latest)

- Risk-on environment continued last week

- Underlying reasons include the effectiveness of existing vaccines against Omicron and the weakness of Omicron’s virulence

- Therefore, the basic assumption is that risk-on will continue into the New Year

- However, the renewed selling of the Turkish lira is a risk-off factor to monitor

- Uncertainty about the fate of the U.S. Build Back Better Act is another element of uncertainty

- Another theme is “inflation”

- We will continue to watch inflation pressures and the resulting differences in monetary policy

Global Macro Environment (Supplement)

- About half of participants in the interest-rate futures market expect the U.S. rate hike to begin in March next year

- Expectations for a U.S. rate hikecentered on four hikes next yearin total

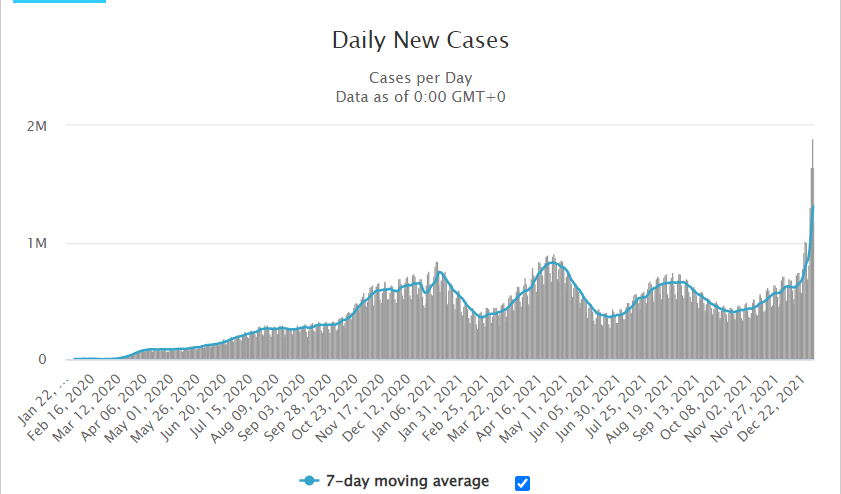

- The daily new COVID-19 cases (7-day moving average) are rising sharply (attached chart Daily New Cases)

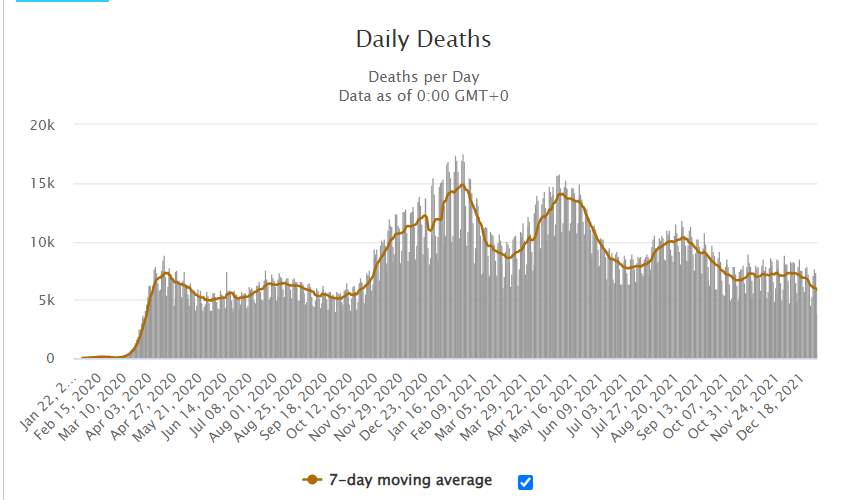

- Meanwhile, the trend of new COVID-19 deaths (7-day moving average) is downward, andOmicron’s weaker virulence is almost certainto be the case (attached chart Daily New Cases)

Market participants' FOMC rate-hike expectations, excerpt from CME Group

COVID-19 new cases, excerpt from Worldmeters

COVID-19 new deaths, excerpt from Worldmeters

Chart Analysis

USD Index (Daily)

- Dollar Index is an indicator of the dollar’s overall strength (basket composition: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Continues to trade within the 95.50–96.90 range in a strong dollar environment

- The current level is viewed as a pullback in the dollar

USD/JPY Medium-term (Daily)

- Break clearly above the 112.70–114.40 range

- A pattern aiming for the recent high of 115.50

- Main driver is yen weakness, so continued risk-on is key

- If a dollar-buying/recoveries resume, there is a risk that USD/JPY could fall

USD/JPY Short-term (Intraday)

- Short-term, it’s prudent to trend higher with 114.70, 115.00 as a base

- Be mindful of dollar-buying and yen-buying episodes

EUR/USD Medium-term (Daily)

- In a downtrend, trading between 1.1210 and 1.1370

- However, buying has been stronger recently

- Continue to sell euro until it decisively clears 1.1370

EUR/USD Short-term (Intraday)

- Clear movement above 1.1350

- 1.1370 briefly breached, but not a full breakout yet

- Consider placing stops around 1.1410 and look to move lower

USD/CNH Medium-term (Daily)

- Bounced after breaking the 6.35 lower bound

- Medium-to-long-term yuan strength persists

USD/CNH Short-term (Intraday)

- Year-end large yuan-buying flow appears to have occurred

- If such capital inflows continue into next year, buying yuan would be straightforwardto do

TodA’s Trading Strategy This Week

Overall Policy

- Follow the risk-on trend (yen selling, yuan buying, stock buying)

- However, with euro near the upper end of its range, start with euro selling

- Continue selling at the top of the range, buying at the bottom

USD/JPY

- Last Friday’s close: 115.08

- View: Range-bound to slightly higher

- Expected range: 114.40–115.80

- Current position: USD/JPY ±0

- At the start of the week, observe first

- If 115.00 holds, go long for a short-term gain

- Take profit near 115.50 first

- If it pulls back, look to re-enter long around 114.70–114.40

EUR/USD, EUR/JPY

- Last Friday’s close: EUR/USD 1.1368

- View: EUR/USD range-bound to down; EUR/JPY range-bound

- Expected range: EUR/USD 1.1300–1.1400

- Current position: EUR/USD ±0; EUR/JPY ±0

- For EUR, plan to build a sell position of 2.0 at week start, expecting a 1.1370 around reversal

- Setting a stop at 1.1410 offers good risk/reward for a downward move

- Would like to take partial profit around 1.1300 on the downside

CNH/JPY, USD/CNH

- Last Friday’s close: USD/CNH 6.3611

- View: USD/CNH range-bound to down; CNH/JPY range-bound to up

- Expected range: USD/CNH 6.3000–6.4000

- Current position: USD/CNH ±0.0; CNH/JPY ±0.0

- At the start of the week, sell USD/CNH by 2.0, place a stop at 6.4250

- Take profits will be watched

Subscriber-Only Discord Invite Code

Please apply using the URL below

※Please align the registered name with your GogoJungle nickname

Notes

Unauthorized reproduction or copying of any content in this newsletter is prohibited. This newsletter is created purely for informational purposes, and its accuracy is not guaranteed by us or the information provider; contents may change due to changes in economic conditions. Use the information at your own risk and consult professionals (legal, accounting, tax, etc.) for individual matters. If a user suffers damages from using this information, we and the information provider are not liable for indemnification regardless of the cause.