Trading strategy considering the near-term risk-on sentiment and year-end liquidity [December 27–December 31]

Last Week's Foreign Exchange Range (Fluctuation Range)

| Opening Price | Low | High | Closing Price | Change Rate | |

|---|---|---|---|---|---|

| USD/JPY | 113.63 | 113.33 | 114.52 | 114.41 | +0.70% |

| EUR/USD | 1.1243 | 1.1235 | 1.1344 | 1.1317 | +0.66% |

| EUR/JPY | 127.72 | 127.51 | 129.79 | 129.48 | +1.38% |

| USD/CNH | 6.3857 | 6.3668 | 6.3909 | 6.3724 | ▲0.21% |

| CNH/JPY | 17.8032 | 17.7380 | 17.9676 | 17.9453 | +0.80% |

Last Week's Forex Summary

USD/JPY

- Last week's dollar-yen pair started at 113.63 yen per dollar. The week began with a dip to 113.33, but thereafter the market gradually turned risk-on as the Turkish lira rebounded and vaccine effectiveness against the Omicron variant was demonstrated by pharmaceutical companies, leading to a gradual strengthening of the dollar-yen.As of Friday the 24th, the week’s high was 114.52 yen; after that, trading was subdued during the Christmas holidays, closing at the same level of 114.41.

EUR/USD

- The euro started at 1.1243 dollars per euro. With the market leaning risk-on for the reasons above, the euro saw buying interest. After fluctuating, it moved up into the 1.13s by midweek, and the upside continued. However, around 1.1340 selling dominated, and it subsequently traded in the 1.1300–1.1340 range, closing at 1.1317.

USD/CNH

- The yuan started at 6.3857 per dollar. In a risk-on environment, the dollar weakness and yuan strength progressed gradually. It touched 6.3668 on Friday and closed at 6.3724.

What Happened Last Week

※ Price indices and money statistics are year-on-year for the CPI, GDP is quarter-on-quarter, and other economic indicators without special notation are month-on-month or for the current month.20th

- PBOC (People's Bank of China) lowered the one-year LPR (Loan Prime Rate) by 0.05%

- Eurozone October current account balance +€18.1 billion

- U.S. November leading indicators +1.1%

21st

- U.S. Q3 2021 current account deficit −$214.8 billion

- U.S. 20-year Treasury auction highest bid yield 1.942%

- Israeli Prime Minister Bennett announced plans to begin a fourth dose for those aged 60 and older and for healthcare workers, in light of the Omicron variant. According to local media,the fourth shot would be the first in the world.

22nd

- U.S. Q3 2021 real GDP (BEA)+2.3% (0.2 percentage point upward revision)

- U.S. Q3 2021 core PCE (BEA) – preliminary value+4.6% (0.1 percentage point upward revision)

- U.S. November existing-home sales +1.9%

- BOJ Governor Kuroda said at a recent policy meeting that the inflation outlook for 2021 was revised down from the previous estimate, due largely to temporary factors such as a change in statistical computation methods earlier this summer.Among BOJ members, the view on inflation was that the forecast would continue to rise gradually as energy prices rise, and the upside would be moderated by these factors.The price growth outlook is regarded as having a positive effect on Japan's economy overall, though some negative aspects were noted.

23rd

- Germany November import price index +24.7%

- Canada October monthly GDP +0.8% (MoM)

- U.S. initial jobless claims for the previous week 205,000

- U.S. November PCE deflator +5.7%

- U.S. November durable goods orders +2.5%

- U.S. November new home sales +12.4% (annualized 744,000)

- The Turkish lira has been surging in forex markets.At one point it reached around 10 lira per dollar, up about 16% from the previous day. After the government announced a scheme to guarantee foreign-currency value of lira-denominated deposits on the evening of the 20th, the uptrend continued.

- INEGI reported Mexico’s December 2021 early CPI rose 7.45% year over year. Prices for airfares, travel packages, and items like lemons rose.

- Russian President Putin held his year-end press conference in Moscow. He urged Russia’s willingness to accept a new European security framework, including a moratorium on NATO’s eastward expansion in relations with the West.

- BOJ Governor Kuroda stated in a speech that円安 could have a pronounced negative impact on household income through higher prices, noting that the share of imports in domestic consumption, particularly durable goods, is increasing.He suggested that yen depreciation could have positive effects for exporters and the economy overall, but he acknowledged the risks as well.

24th

- The Christian world observes Christmas Eve as a holiday.

- Japan November nationwide CPI +0.6%

- Japan November corporate services price index +1.1%

- Japan November new housing starts +3.7%

- The Ministry of Internal Affairs and Communications reported that November's CPI rose 0.6% year on year, up 0.5 points from October. Excluding the impact of the policy-driven mobile price reductions, the pace appears to exceed 2%.

- UK health authorities reported daily new Omicron infections reaching 20,279, totaling 114,625 nationwide. New COVID-19 infections on the 24th reached 122,186, marking four consecutive days above 100,000; both figures were record highs.

- From December 24 to 26, major airlines worldwide canceled more than 4,000 flights as Christmas holidays begin.The cancellations were due to Omicron-related infections among airline staff, creating travel disruptions.

- China's Xi Jinping leadership is considering lowering the target for real GDP growth for 2022 from 2021's level.While 2021's target was above 6%, proposals for 2022 include a target of 5.5–6%.

Economic Terms Glossary

- GDP = Gross Domestic Product: high growth is positive

- CPI = Consumer Price Index: many advanced economies target around 2%

- PCE = Personal Consumption Expenditures: closely related to consumer prices

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Manager Index: 50 is the threshold

- ZEW = Leibniz Centre for European Economic Research: 0 is the baseline

- NAHB = National Association of Home Builders: 50 is the baseline

- NY Fed Manufacturing Index: 0 is the baseline

- Philadelphia Fed Manufacturing Index: 0 is the baseline

- Richmond Fed Manufacturing Index: 0 is the baseline

- Chicago PMI: 50 is the baseline

- University of Michigan Consumer Sentiment Index: indexed with 100 for 1966

- S&P/ Case-Shiller Home Price Index: the 20-CMS Home Price Indices are commonly used; a key indicator for housing market trends that influence the economy

- Housing Pending Sales Index: contracts signed but not yet closed

- European Consumer Confidence Index: 100 is the average from 2000–2020, up or down from there (released as MoM)

- European Economic Sentiment Index: 100 is the average from 2000–2020 (released as actuals)

- Consumer Confidence Index: indexed with 100 base in 1985

- Japan's Composite Leading Index: indexed with 100 base in 2015

- Japan's Economy Watchers Survey: 50 is the baseline

- Japan Corporate Goods Price Index: 0 baseline

Attention-Grabbing Economic Indicators and Political Events

27th

- Australia, New Zealand, Canada, UK holidays

28th

- Australia, New Zealand, Canada, UK holidays

- China's Evergrande Group misses a USD 250.2 million dollar-denominated bond interest payment

- 08:50 Japan December industrial production

- 23:00 U.S. October Case-Shiller U.S. home price index

- 24:00 U.S. December Richmond Fed manufacturing index

29th

- 24:00 U.S. November existing-home sales pending index

- 25:00 Russia Q3-Q4 real GDP

- 25:00 Russia December consumer price index

30th

- 22:30 U.S. initial jobless claims for the previous week

31st

- Many countries including Japan, Korea, Germany observe holidays or early closes

- 10:00 China December PMI

Next Week and Beyond

- Jan 17–21: Davos World Economic Forum

- Jan 18: BoJ Monetary Policy Meeting (outlook for economy and price structure included)

- Jan 26: FOMC

- Feb 3: ECB

- Mar 5: National People's Congress

- Mar 10: ECB

- Mar 16: FOMC (with economic projections)

- Mar 18: BoJ Monetary Policy Meeting

- Apr 14: ECB

- Apr 28: BoJ Monetary Policy Meeting (with outlook for economy and price)

- May 4: FOMC

- Jun 9: ECB

- Jun 15: FOMC (with economic projections)

- Jun 17: BoJ Monetary Policy Meeting

- Jul 21: BoJ Monetary Policy Meeting (with outlook for economy and price)

- Jul 21: ECB

- Jul 27: FOMC

- Sep 8: ECB

- Sep 21: FOMC (with economic projections)

- Sep 22: BoJ Monetary Policy Meeting

- Oct 27: ECB

- Oct 28: BoJ Monetary Policy Meeting (with outlook for economy and price)

- Nov 2: FOMC

- Dec 14: FOMC (with economic projections)

- Dec 15: ECB

- Dec 20: BoJ Monetary Policy Meeting

Currency Strength Last Week

- Last week, dollar selling was dominant (140/196 countries).

- One factor in the risk-on market was the substantial rebound in the Turkish lira.Reason: the Turkish government's loss-compensation measures.

- Additionally, resource currencies performed well, with buying in South Africa, Norway, Australia, etc.The outlook for economic activity was reassured as the effectiveness of existing vaccines against the Omicron variant was demonstrated.

- In summary, last week's currency strength order was as followsTurkish lira > Resource currencies > Euro > Chinese yuan > US dollar > Yen

Global Macro Environment (Latest)

- Despite it being Christmas week, risk-on sentiment arose due to the lira rebound and the efficacy of existing vaccines against Omicron.

- US stocks returned to pre-Omicron levels; for example, the S&P 500 closed at a new high.

- On the other hand, Omicron infection spreads rapidly, with new COVID-19 cases at a record pace.

- Whether this will be read asthe coronavirus turning into a common cold, or whether that assessment is premature remains to be seen.This will continue to require monitoring ongoing reports.

- The passage of the U.S. Democratic Build Back Better Act is postponed to next year.

- This week is the year-end holiday week.As usual, market participants thin out, making it harder to discern direction. Also, with fewer orders, be mindful of choppy price movements.

Global Macro Environment (Supplement)

- Markets are rapidly pricing in the start of a rate hike cycle in March next year

- The dollar-rate hike expectation centers around three increases next year

- The trend of daily new COVID-19 cases (7-day moving average) is rising again (see attached chart Daily New Cases)

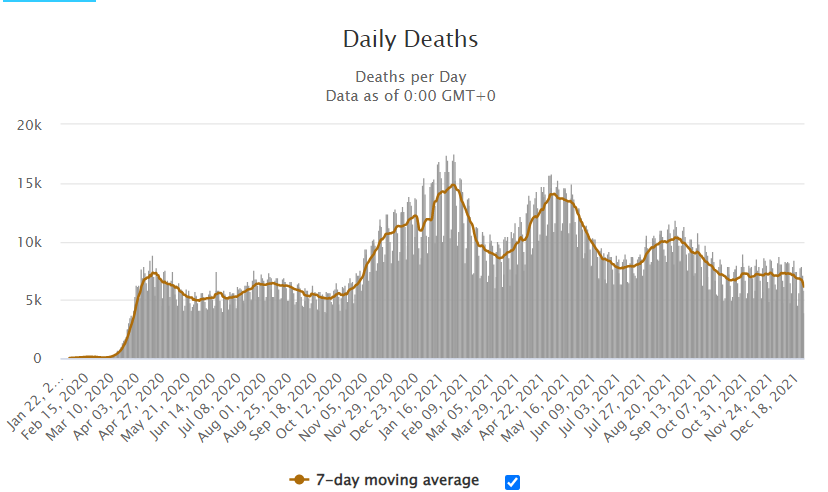

- The trend of daily new COVID-19 deaths (7-day moving average) is downward(Attached chart Daily New Cases )。This result is also perceived as a risk-on factor.

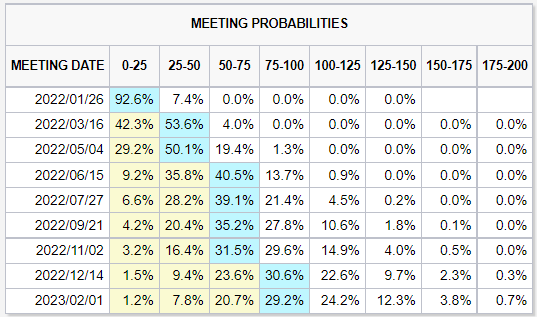

Market participants’ FOMC rate-hike expectations, excerpt from CME Group

COVID-19 daily new cases, excerpt from Worldometers

Chart Analysis

USD Index (Daily)

- Dollar Index is an indicator of overall dollar strength (composition of the basket: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Within a dollar-strength trend, it has traded in a range of 95.50–96.90

- The current level is viewed as a pullback opportunity

USD/JPY Medium-Term (Daily)

- Brushing past the 112.70–114.40 range with momentum

- The main driver is risk-on and yen weakness, so whether this continues is crucial

USD/JPY Short-Term (Intraday)

- Both medium- and short-term upside pressure remains stronger, making it reasonable to push higher

EUR/USD Medium-Term (Daily)

- In a downtrend, it is trading around 1.1210–1.1370

- There appears to be selling pressure near resistance, but until 1.1370 is clearly surpassed, selling-first is advisable

EUR/USD Short-Term (Intraday)

- Narrower range around 1.1230–1.1350

- Dollar strength is prevailing; at present, maintain a selling bias

USD/CNH Medium-Term (Daily)

- Broke the lower end of the 6.35 range and rebounded

- Upper levels remain heavy

USD/CNH Short-Term (Intraday)

- Little movement continues.

- With U.S. rate hikes ahead, how long yuan strength lasts remains in question

This Week's Toda Trading Strategy

Overall Policy

- Enter on a risk-on trend

- However, monitor Omicron developments closely. With thin market participation around year-end, expect low liquidity and smaller positions.

- Sell at the top of ranges, buy at the bottom

USD/JPY

- Last Friday's close: 114.41

- View: range-bound to mildly higher

- Expected range: 113.55–115.25

- Current position: USD/JPY ±0

- Use 114.00 and 114.40 as levels to buy on pullbacks

- If it pulls back, enter on dips around 113.50

EUR/USD, EUR/JPY

- Last Friday's close: EUR/USD 1.1317

- View: EUR/USD range-bound to down; EUR/JPY range-bound

- Expected range: EUR/USD 1.1200–1.1370

- Current position: EUR/USD +2.0; EUR/JPY 0

- Expect range continuation

- Sell until 1.1370 is clearly broken

- Buy back around 1.1200

CNH/JPY, USD/CNH

- Last Friday's close: USD/CNH 6.3724

- View: USD/CNH flat, CNH/JPY flat

- Expected range: USD/CNH 6.3500–6.4250

- Current positions: USD/CNH ± 0.0; CNH/JPY ± 0.0

- If USD/JPY declines to the mid-113s, consider buying CNH/JPY

Subscriber-Only Discord Invitation Code

Please apply from the URL below

※ Please match your registered name with your GogoJungle nickname

Important Notice

Unauthorized reproduction or copying of any content published in this newsletter is prohibited. This newsletter is created for information provision only, and its accuracy is not guaranteed by our company or the information sources. Also, the published content may change due to changes in economic conditions. Use the information at your own responsibility and judgment, and for individual matters, please consult professionals in law, accounting, and taxation. If a user suffers damage from using this information, our company and the information sources shall not be liable for compensation regardless of the cause.