Trade Strategy Considering Omicron Variant and Christmas Holidays [December 20–December 24]

Last Week's Forex Range (Volatility Range)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 113.28 | 113.14 | 114.28 | 113.67 | +0.34% |

| EUR/USD | 1.1316 | 1.1221 | 1.1361 | 1.1239 | ▲0.68% |

| EUR/JPY | 128.31 | 127.75 | 129.66 | 127.74 | ▲0.44% |

| USD/CNH | 6.3728 | 6.3623 | 6.3940 | 6.3857 | +0.20% |

| CNH/JPY | 17.7653 | 17.7136 | 17.9235 | 17.7924 | +0.15% |

Last Week's Forex Summary

USD/JPY

- Last week the USD/JPY started at 113.28 per dollar. With the FOMC meeting on Wednesday approaching, expectations for an earlier tapering announcement led to dollar buying at the start of the week. The USD/JPY trend remained above, edging higher into Wednesday. At the FOMC meeting,the schedule for tapering completion by March next year was announced, briefly pushing it up to 114.28. However, toward the weekend, concerns about the Omicron variant and looming Christmas holidays led to profit-taking, sending USD/JPY down to as low as 113.14. By the end of the week, it recovered to close at 113.68.

EUR/USD

- The euro started at 1.1316 dollars per euro. With the FOMC on Wednesday, dollar buying dominated early in the week, similar to USD/JPY. After the FOMC announced the March tapering schedule, the euro briefly fell to 1.1221, but later recovered as buyers returned. At the ECB Council meeting,the emergency support program was officially announced to end in March 2022, lifting the euro back to 1.1361. Toward the weekend, dollar strength re-emerged and the euro fell to 1.1239 to close.

USD/CNH

- The yuan started at 6.3728 per dollar. With expectations of multiple US rate hikes, dollar buying stayed in control and the dollar appreciated modestly across the week. The weekend closed at 6.3870.

What Happened Last Week

※ CPI and money statistics are year-over-year, GDP is quarter-over-quarter, and indicators without a specific note are month-over-month or current month figures13th

- Japan Oct-Dec Bank of Japan Short-Term Economic Survey of Enterprises large manufacturers 18, non-manufacturers 9

- Japan Oct Machinery Orders +3.8%

- India Nov Consumer Price Index +4.9%

- OPECin its monthly report published, amid stronger restrictions in Europe and the spread of Omicron,slightly lowered oil demand for Oct-Dec 2021.

14th

- Japan Oct Capacity Utilization +6.2%

- UK Nov Unemployment Rate 4.9%

- Sweden Nov Consumer Price Index +3.3%

- Euro Area Oct Industrial Production +1.1%

- US Nov Producer Price Index +9.6% (strong inflation pressures)

- WHO Director-General Tedros stated that the Omicron variant is spreading at a rate not seen with other variants, prompting warnings that hospitals may be overwhelmed if systems are unprepared.

- Chile's central bank to raise policy rate by 1.25 percentage points to 4%, marking the fourth consecutive rate hike.

15th

- China Nov Retail Sales +3.9% (YoY)

- China Nov Industrial Production +3.8% (YoY)

- UK Nov CPI +5.1%

- France Nov CPI +2.8%

- South Africa Nov CPI +5.5%

- Canada Nov CPI +4.7%

- US Dec NY Fed Manufacturing Index 31.9

- US Nov Retail Sales +0.3%

- US Federal Reserve Board (FRB) decided at the FOMC on the 15th to accelerate the tapering of asset purchases, with the expected end shifted from June 2022 to March 2022 and anticipating three rate hikes in 2022. Inflation was persistent, prompting a快速 adjustment to tapering begun a month earlier.

16th

- Japan Trade Statistics ▼¥9,548 hundred million

- Australia Nov Employment +361,000; Unemployment Rate 4.6% (very strong)

- Swiss National Bank kept policy rate at -0.75%

- Germany Dec PMI Manufacturing 57.9, Services 48.4

- Euro Area Dec PMI Manufacturing 58.0, Services 53.3

- Turkish Central Bank cut policy rate by 1.00% to 14.00% (as the US rises rates, Turkey moves to cutting rates—points to watch)

- Bank of England raised policy rate by 0.15% to 0.25%

- US Nov Housing Starts +11.8%

- US Previous Week Initial Jobless Claims 206,000

- US Dec PMI Manufacturing 57.8, Services 57.5

- Mexico Banxico raised policy rate by 0.50% to 5.50%

- Norwegian Central Bank raised policy rate by 0.25% to 0.50%— first rate hike since pausing zero-interest policy in September.

- ECB at 16th Council meeting decided to end the pandemic emergency asset purchase programme by end-March 2022. With the programme totaling 1.85 trillion euros, asset purchases in 2022 onwards are expected to be less than half of current levels.

- G7 health ministers held an online meeting on the new Omicron variant. The chair, UK, reported thatall seven countries agreed that Omicron poses the greatest threat to global public health.

17th

- Russia’s Central Bank raised policy rate by 1.0% to 8.50%

- Bank of Japan decided at the 17th monetary policy meeting to shrink liquidity support measures for COVID-19 response. It will end purchases of Commercial Paper (CP) and corporate bonds up to ¥20 trillion as scheduled by end-March 2022, while extending the holders of funds for banks through Special Operations (OMOs) for six more months to end-September.

- Russia published a new European security proposal calling for NATO expansion halt and de facto troop withdrawal from Eastern Europe; talks with the US and Europe are unlikely to progress, keeping tensions high.

- Colombia’s central bank raised policy rate by 0.5% to 3% (third consecutive hike).

- Turkish lira briefly hit around 17 per dollar, an all-time low, amid direct central bank intervention; it remained about 7% weaker than the previous day.

- FRB officials have signaled a sustained hawkish stance on inflation; Williams of NY Fed on CNBC said rate hikes would be warranted if the economy heals sufficiently, and Waller echoed that a rate hike could come soon after asset purchases end (by March 2022).

- The world continues to grapple with the Omicron spread. WHO noted that Omicron infections are doubling every 1.5 to 3 days in many places, intensifying global infection rates as of the 16th in 89 countries.

Economic Terms Glossary

- GDP = Gross Domestic Product: strong growth is good

- CPI = Consumer Price Index: many advanced economies target 2%

- PCE = Personal Consumption Expenditures: consumer spending; closely related to price levels

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Manager Index: 50 is the baseline

- ZEW = Leibniz Centre for European Economic Research: 0 is the baseline

- NAHB = National Association of Home Builders: 50 is the baseline

- NY Fed Manufacturing Index: 0 is the baseline

- Philly Fed Manufacturing Index: 0 is the baseline

- Richmond Fed Manufacturing Index: 0 is the baseline

- Chicago Purchasing Officers’ Index: 50 is the baseline

- University of Michigan Consumer Sentiment Index: indexed with 1966=100

- S&P/ Case-Shiller Home Price Indices: widely used is the 20-C-city index; critical for housing market trends impacting the economy

- Pending Home Sales Index: contracts signed but not yet closed; measures housing market activity

- European Consumer Confidence Index: 2000-2020 averages set to 100 with range around it (released MoM)

- European Economic Sentiment Index: 2000-2020 averages set to 100

- Consumer Confidence Index: indexed with 1985=100

- Japan Leading Index: indexed with 2015=100

- Japan Tankan Large Manufacturers’ Index: 50 is the baseline

- Japan Corporate Goods Price Index: 0 baseline

Key Economic Indicators and Political Events

20th

- National People’s Congress Standing Committee (through the 24th)

- 10:30 PBOC Loan Prime Rate

- 18:00 Euro Area Oct Current Account

21st

- 09:30 RBA (Australia) Monetary Policy Meeting Minutes

- 22:30 US Q3-Current Account

22nd

- 08:50 BOJ Policy Meeting Minutes

- 16:00 UK Q3-Q4 Current Account

- 22:30 US Q3 Real GDP (Annualized, Preliminary)

- 22:30 US Q3 Core PCE (Annualized)

- 24:00 US Nov Existing Home Sales

23rd

- Russia, Putin annual press conference

- Keidanren meeting; BoJ Governor Kuroda speaks

- 16:00 Germany Nov Import Prices

- 22:30 Canada Oct Monthly GDP

- 22:30 US Week-ago Initial Jobless Claims

- 22:30US Nov Personal Consumption Expenditures (PCE Deflator)

- 22:30 US Nov Durable Goods Orders

- 24:00 US Nov New Home Sales

24th

- US and other Christian-majority countries observe Christmas Eve (holiday)

- 08:30 Japan Nov Nationwide Consumer Price Index

- 08:50 Japan Nov Corporate Services Price Index

- 14:00 Japan Nov New Construction Starts

Next Week and Beyond

- Jan 17–21: Davos World Economic Forum

- Jan 18: BoJ Monetary Policy Meeting (outlook for economy and prices)

- Jan 26: FOMC

- Feb 3: ECB

- Mar 10: ECB

- Mar 16: FOMC (with Economic Projections)

- Mar 18: BoJ Monetary Policy Meeting

- Apr 14: ECB

- Apr 28: BoJ Monetary Policy Meeting (outlook for economy and prices)

- May 4: FOMC

- Jun 9: ECB

- Jun 15: FOMC (with Economic Projections)

- Jun 17: BoJ Monetary Policy Meeting

- Jul 21: BoJ Monetary Policy Meeting (outlook for economy and prices)

- Jul 21: ECB

- Jul 27: FOMC

- Sep 8: ECB

- Sep 21: FOMC (with Economic Projections)

- Sep 22: BoJ Monetary Policy Meeting

- Oct 27: ECB

- Oct 28: BoJ Monetary Policy Meeting (outlook for economy and prices)

- Nov 2: FOMC

- Dec 14: FOMC (with Economic Projections)

- Dec 15: ECB

- Dec 20: BoJ Monetary Policy Meeting

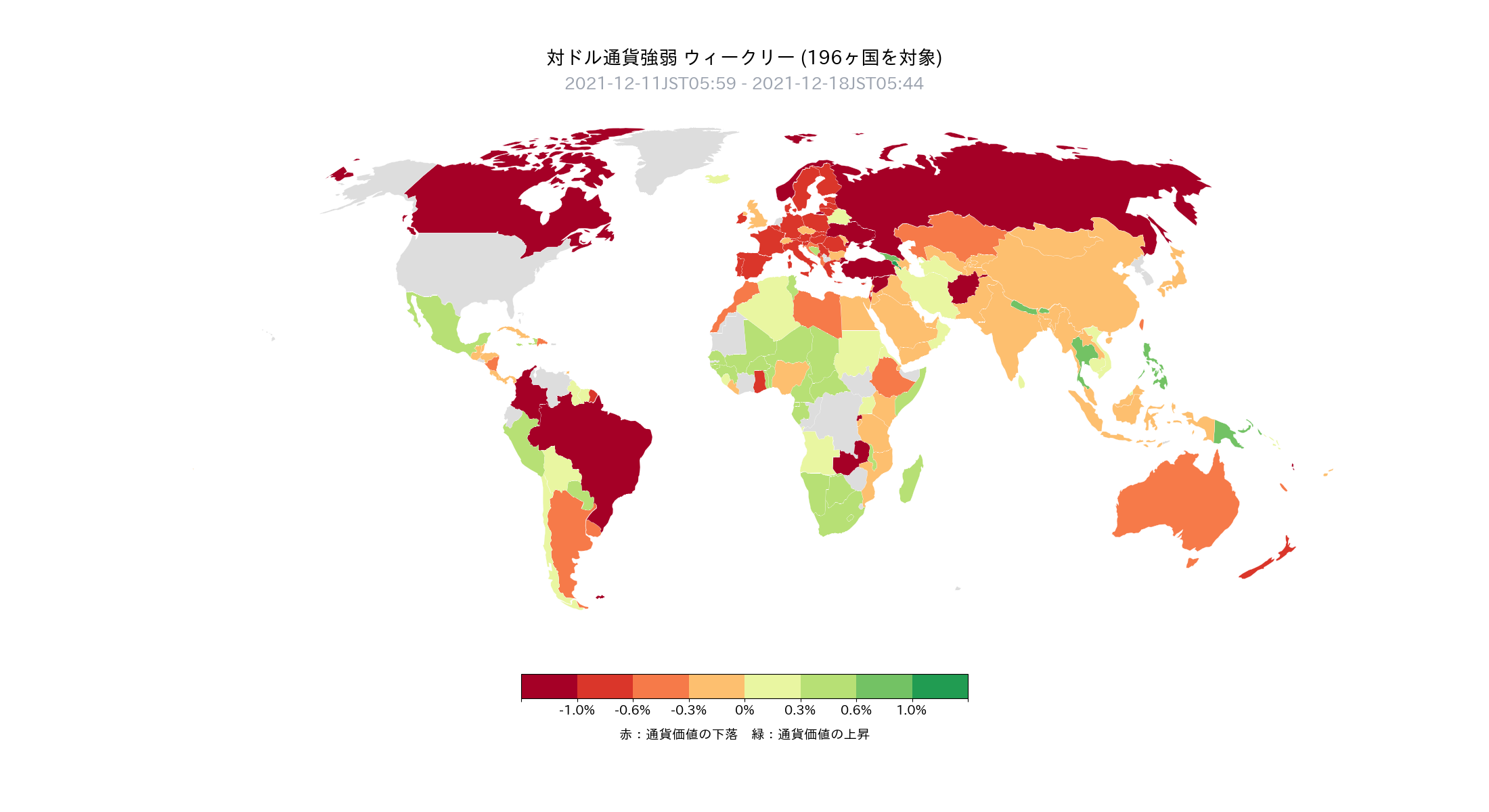

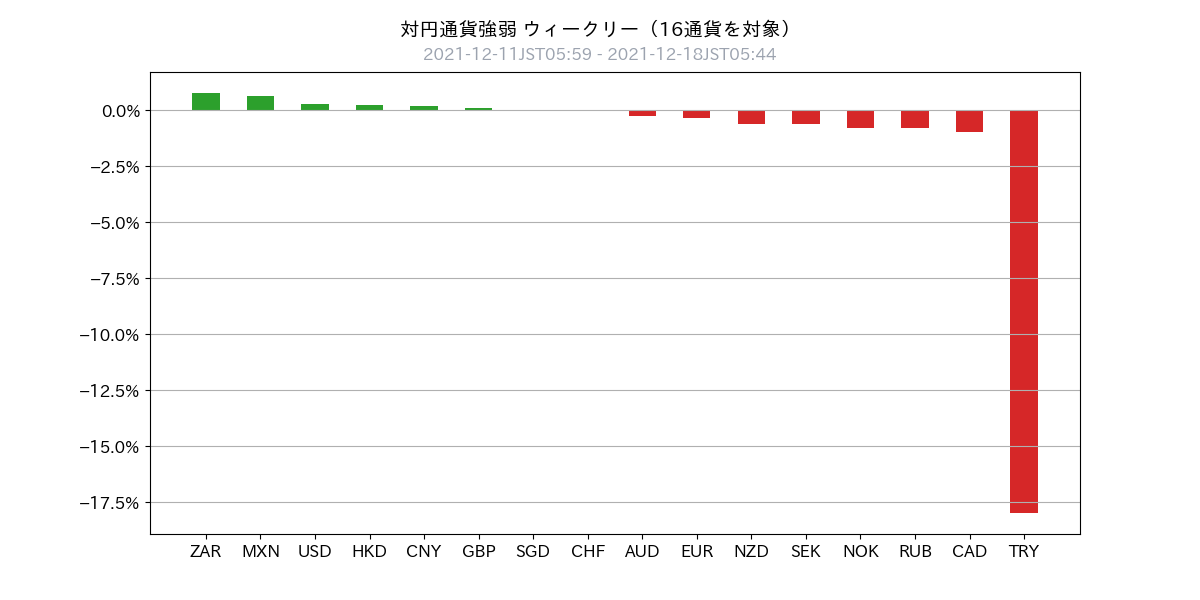

Last Week's Currency Strength

- Dollar buying remained dominant last week (138/196 countries). Backed by expectations of earlier tapering of monetary easing and rate hikes in the United States.

- The currencies of Canada, Russia, Europe, etc., perhaps due to cold weather, of higher latitudes were sold.

- The Turkish lira fell more than 17.5%.Believed to be one of the factors deteriorating market sentiment.

- Last week's currency strength/weakness was as followsDollar > yuan > yen > euro > lira

Global Macro Environment Update (Latest)

- Last week, interest rate hikes were implemented by the UK, Norway, Mexico, Russia, Chile, and Colombia.Central banks around the world are responding to broad inflationary pressures with rate hikes.

- With the FOMC (Federal Reserve policy meeting) being navigated smoothly,the market attention is shifting toward the impact of Omicron.In particular, authorities such as G7 health ministers and the WHO are sounding the alarm regarding the rapidly spreading Omicron variant in places like the UK.

- Furthermore, passage of the U.S. Democratic Build Back Better bill is expected to be delayed into next year, which, combined with the two preceding points,creates a conspicuous risk-off environment.

- The market is finally entering Christmas holiday mode.Typically liquidity dries up, making it harder to discern a clear trend. Also, with fewer orders, be wary of wild price movements.

Global Macro Environment Update (Supplement)

- The expectation is for three rate hikes next year as the base scenario

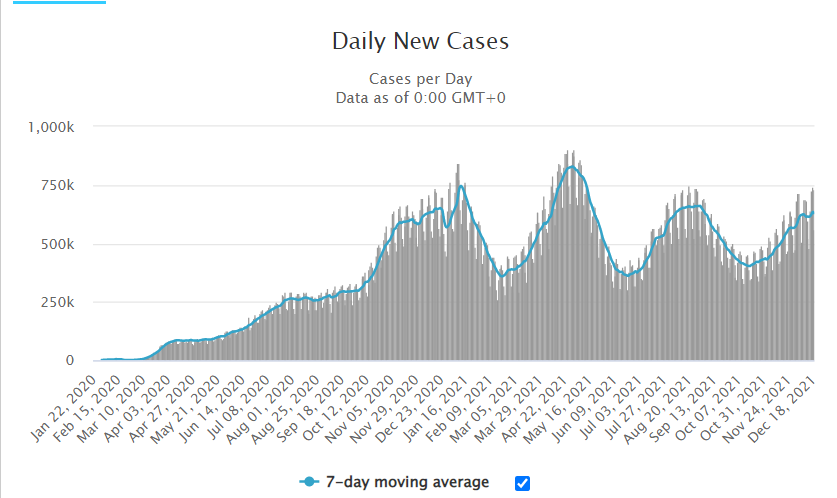

- The daily new COVID-19 cases (7-day moving average) are again on an upward trend(Attached chart: Daily New Cases)

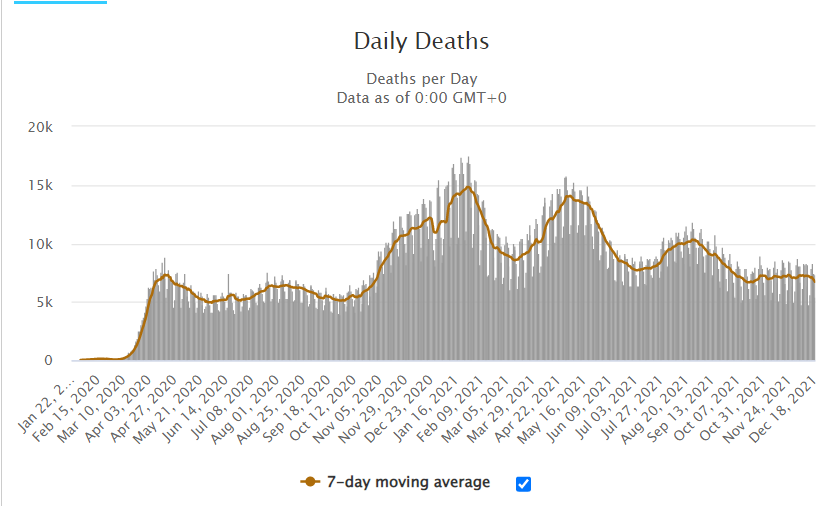

- The daily new COVID-19 deaths (7-day moving average) are leveling off and may turn downward

Chart Analysis

USD Index (Daily)

- The U.S. Dollar Index is a measure of the dollar's overall strength (basket composition: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Within a broader dollar strength trend, it is trading in a range of 95.50 to 96.90

USD/JPY Medium Term (Daily)

- In a dollar-strength environment, it is trading in a range of 112.70 to 114.40

USD/JPY Short Term (Intraday)

- In an even narrower range, 113.20 to 114.00

EUR/USD Medium Term (Daily)

- In a downtrend, trading in the 1.1210 to 1.1370 range

- 1.1370 is acting as a strong support

- Next year, euro selling on rallies could be effective

EUR/USD Short Term (Intraday)

- In an even narrower range, 1.1230 to 1.1350

- Around 1.13, prefer selling pressure

USD/CNH Medium Term (Daily)

- Broke below the 6.35 range, then rebounded

- If it breaks above 6.40 or 6.4250, the yuan may stay under pressure for a while

USD/CNH Short Term (Intraday)

- Short-term upside pressure is strong

- With rising U.S. yields, further yuan strength may be unlikely

This Week's Todashi Trading Strategy

Overall Policy

- With markets thinner during Christmas, expect higher volatility; keep positions light

- Assume little trend clarity overall; focus on selling on top of ranges and buying at the bottom

USD/JPY

- Last Friday's close: 113.67

- View: flat to slightly lower

- Proposed range: 112.70 to 114.00

- Current position: USD/JPY ±0

- There are many risk-off factors, and resistance at 114.40; short-term downside bias

- In a rising scenario (around 114.00), look to sell on rallies

EUR/USD, EUR/JPY

- Last Friday's close: EUR/USD 1.1239

- View: EUR/USD flat to lower; EUR/JPY lower

- Proposed range: EUR/USD 1.1200 to 1.1300

- Current position: EUR/USD ±0; EUR/JPY ±0

- Prefer selling above 1.1300

CNH/JPY, USD/CNH

- Last Friday's close: USD/CNH 6.3857

- View: USD/CNH flat to higher; CNH/JPY flat to lower

- Proposed range: USD/CNH 6.3500 to 6.4250

- Current positions: USD/CNH ±0.0; CNH/JPY ±0.0

- With rate hikes in view, avoid excessive optimism for the yuan; adopt a wait-and-see stance

Subscriber-Only Discord Invitation Code

Please apply from the URL below

※Please align the registered name with your GogoJungle nickname

Important Notice

Unauthorized reproduction or copying of any content published in this newsletter is prohibited. This newsletter is prepared solely for information provision, and its accuracy is not guaranteed by our company or the information sources. The content is subject to change due to changes in economic conditions. Use the information at your own risk and discretion; for individual matters, please consult professionals in law, accounting, and tax. If a user suffers damages from using this information, our company and the information sources shall not be liable for compensation regardless of the cause.

× ![]()