Trading strategy considering a decline in market participants and U.S. monetary policy [December 13–December 17]

Last Week's Foreign Exchange Range (Volatility)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 112.78 | 112.77 | 113.96 | 113.38 | +0.53% |

| EUR/USD | 1.1321 | 1.1228 | 1.1356 | 1.1311 | ▲0.09% |

| EUR/JPY | 127.61 | 127.50 | 129.19 | 128.24 | +0.49% |

| USD/CNH | 6.3700 | 6.3291 | 6.3893 | 6.3750 | +0.08% |

| CNH/JPY | 17.7005 | 17.6973 | 17.9840 | 17.7767 | +0.43% |

Last Week's Foreign Exchange Summary

USD/JPY

- Last week's USD/JPY started at 112.78. Following the prior week's trend, dollar buying dominated as sessions began, breaking through 113.00 during Asia and 113.30 at U.S. hours. The dollar's rise continued as concerns over Omicron eased and U.S. stocks recovered, reaching 113.96 in New York on Wednesday the 8th. On the 9th and 10th, as U.S. stocks paused, cross currencies were sold and the USD/JPY saw some profit-taking, briefly dropping to 113.22 before a small rebound to close at 113.38.

EUR/USD

- The euro started at 1.1321 per euro against the dollar. Early in the week, euro selling and dollar buying dominated, pushing down to 1.1228 by New York time on the 7th. Afterward, with no particular catalysts, there was a swing to 1.1356 on the 8th in New York time, but the pair moved modestly and closed near the week’s starting level at 1.1312. It was a typical, directionless year-end market.

USD/CNH

- The yuan began at 6.3700 per dollar. From the 7th, persistent yuan buying pushed through the 6.3500 level, leading to a faster dollar decline and yuan appreciation, sinking to 6.3291 at one point. Subsequently, concerns over Evergrande and the PBOC's increase in foreign currency reserve requirement ratio revived the dollar, with a rebound to 6.3893 before settling at 6.3769, leaving the trend directionless.

Events of Last Week

※ Price, money supply, GDP, and other indicators are year-over-year unless otherwise noted; for indicators without special notes, the values are month-over-month or for the current month6th

- Germany October new orders in manufacturing: ▲6.9%

- U.S. Energy Secretary Dan Brouillette at Houston: urged domestic leadership in oil and gas; GDP growth, profitability in the oil and gas industry recover, but production lagging; Biden administration not obstructing increase in output.

7th

- China November trade balance: +$71.72 billion (exports and imports both strong)

- Australia 3Q 2021 housing prices index +5.0% (quarter-on-quarter)

- RBA kept monetary policy unchanged

- Germany October industrial production +2.8%

- Germany December ZEW sentiment index 29.9

- U.S. October trade balance: -$67.1 billion

8th

- Poland central bank raised policy rate by 0.5 percentage point to 1.75%

- India RBI kept policy rate at 4.0%

- Japan October international balance of payments +¥1.18 trillion

- U.S. Oct. JOLTS job openings: 11.0 million (still high)

- Russia November CPI +8.4%

- Brazil central bank raised policy rate by 1.5 percentage points to 9.25%

9th

- Japan Q4 corporate/service-sector Outlook index 9.6

- China November CPI +2.3%

- China November PPI +12.9% (high inflation pressure)

- Initial jobless claims for the previous week: 184K (better than pre-pandemic levels)

- INEGI: Mexico November CPI rose 7.37% year over year, highest since 2001

- Peru central bank raised policy rate by 0.5% to 2.5% at the policy meeting; fifth consecutive rate hike.

- PBOC announces raise in foreign currency reserve requirement: ratio from 7% to 9% starting 15th, to reduce foreign currency liquidity and encourage banks to swap yuan into foreign currency.

10th

- Japan November domestic corporate goods price index +9.0% (high deflator)

- Norway November CPI +5.1%

- Germany November CPI +5.2% (high inflation pressure)

- U.S. November CPI +6.8% (high inflation pressure)

- University of Michigan December sentiment 70.4

- U.S.-hosted Democracy Summit concluded; Biden emphasized democracy as central to the international system

- Markets turned toward risk assets; U.S. stock prices recovered to pre-Omicron levels

- President Biden warned Russia that invasion of Ukraine would lead to deployments of U.S. and NATO forces to Eastern Europe

Economic Terms Glossary

- GDP = Gross Domestic Product: high growth is favorable

- CPI = Consumer Price Index: many advanced economies target 2%

- PCE = Personal Consumption Expenditures: closely related to consumer prices

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Managers' Index: 50 is neutral

- ZEW = Leibniz Centre for European Economic Research: 0 is neutral

- NAHB = National Association of Home Builders: 50 is neutral

- NY Fed manufacturing index: 0 is neutral

- Philadelphia Fed manufacturing index: 0 is neutral

- Richmond Fed manufacturing index: 0 is neutral

- Chicago PMI: 50 is neutral

- University of Michigan Consumer Sentiment index: indexed with 1966=100

- S&P/Case-Shiller Home Price Indices: "20-Ccity" index widely used; important for housing market trends

- Pending Home Sales Index: contracts signed but not yet closed

- European Consumer Confidence Index: base 100 for 2000–2020 average; reported as month-to-month change

- European Economic Sentiment Index: base 100 for 2000–2020 average; reported as actual value

- Consumer Confidence Index: base 100 for 1985

- Japan’s Coincident Economic Index: base 100 for 2015

- Japan Economy Watchers Survey: 50 is neutral

- Japan Corporate Goods Price Index (CI): base 0

Notable Economic Indicators and Political Events

13th

- 08:50 Japan Bank of Japan Short-Term Economic Outlook (Quarterly Large Enterprise Activity)

- 08:50 Japan October Machinery Orders

- 21:00 India November CPI

- 21:00OPEC Monthly Report

14th

- 13:30 Japan October Capacity Utilization

- 16:00 UK November Unemployment

- 17:30 Sweden November CPI

- 19:00 Euro Area October Industrial Production

- 22:30US November PPI

15th

- 11:00China November Retail Sales

- 11:00 China November Industrial Production

- 16:00 UK November CPI

- 16:45 France November CPI

- 17:00 South Africa November CPI

- 22:30 Canada November CPI

- 22:30 U.S. December NY Fed Manufacturing Index

- 22:30U.S. November Retail Sales

- 28:00FOMC

- 28:30Powell, Fed Chair Speech

16th

- 08:50 Japan Trade Statistics

- 09:30 Australia November Employment

- 17:30 Swiss National Bank policy decision

- 17:30 Germany December PMI

- 18:00 Euro Area December PMI

- 20:00 Turkey Central Bank policy decision

- 21:00 Bank of England policy decision

- 21:45 European Central Bank policy decision

- 22:30 Lagarde, ECB President, Press Conference

- 22:30 U.S. November Housing Starts

- 22:30 U.S. Previous Week's Initial Jobless Claims

- 22:30 U.S. December PMI

- 28:00 Mexico Banco de Mexico Policy Rate

17th

- Time TBA Bank of Japan Policy Meeting

- 19:30 Russia Central Bank Policy Meeting

And Beyond Next Week

- Jan 17–21: Davos World Economic Forum

- Jan 18: Bank of Japan Policy Meeting (Outlook for economy and prices)

- Jan 26: FOMC

- Feb 3: ECB

- Mar 10: ECB

- Mar 16: FOMC (with Economic Projections)

- Mar 18: Bank of Japan Policy Meeting

- Apr 14: ECB

- Apr 28: Bank of Japan Policy Meeting (Outlook for economy and prices)

- May 4: FOMC

- Jun 9: ECB

- Jun 15: FOMC (with Economic Projections)

- Jun 17: Bank of Japan Policy Meeting

- Jul 21: Bank of Japan Policy Meeting (Outlook for economy and prices)

- Jul 21: ECB

- Jul 27: FOMC

- Sep 8: ECB

- Sep 21: FOMC (with Economic Projections)

- Sep 22: Bank of Japan Policy Meeting

- Oct 27: ECB

- Oct 28: Bank of Japan Policy Meeting (Outlook for economy and prices)

- Nov 2: FOMC

- Dec 14: FOMC (with Economic Projections)

- Dec 15: ECB

- Dec 20: Bank of Japan Policy Meeting

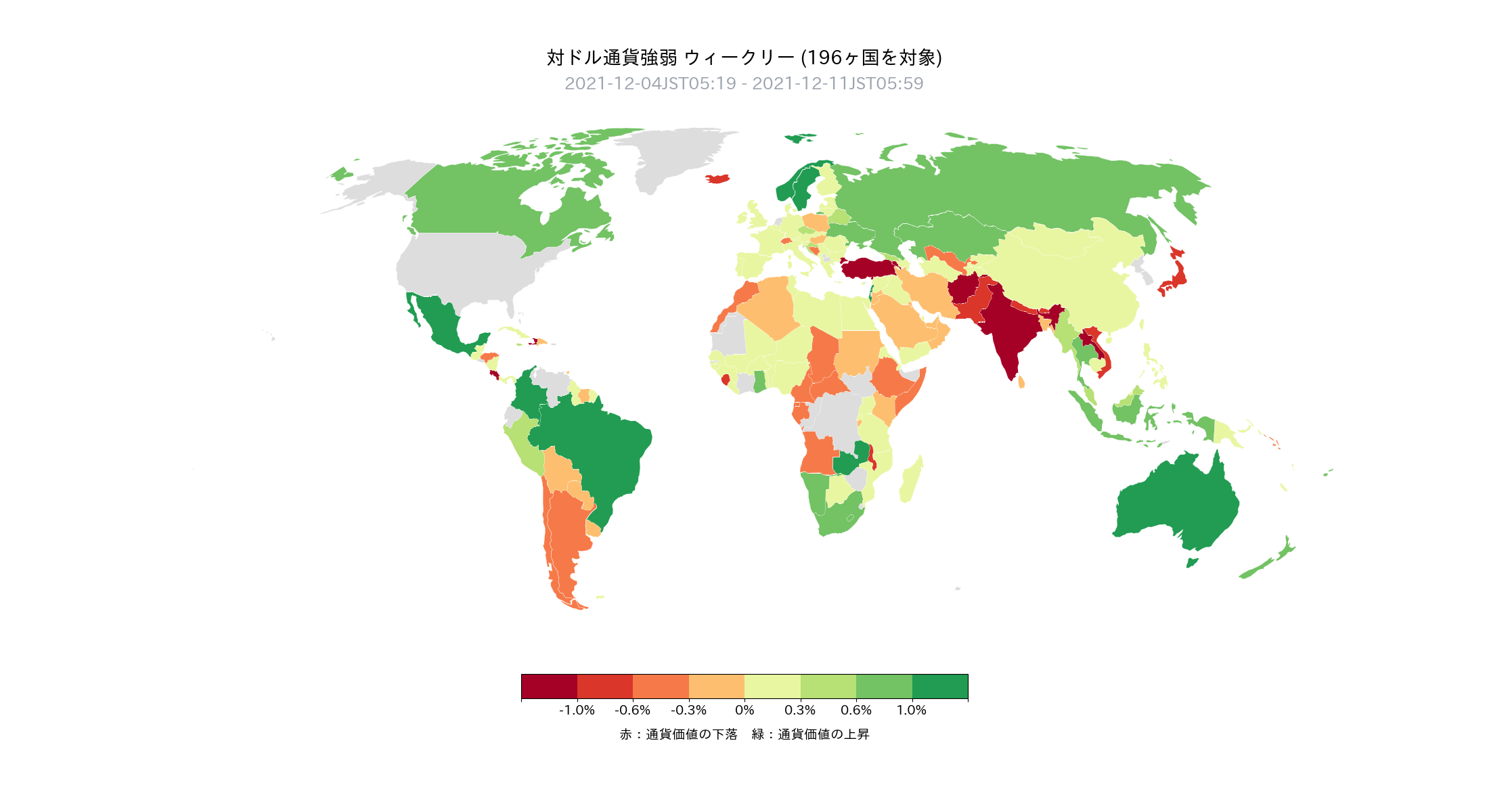

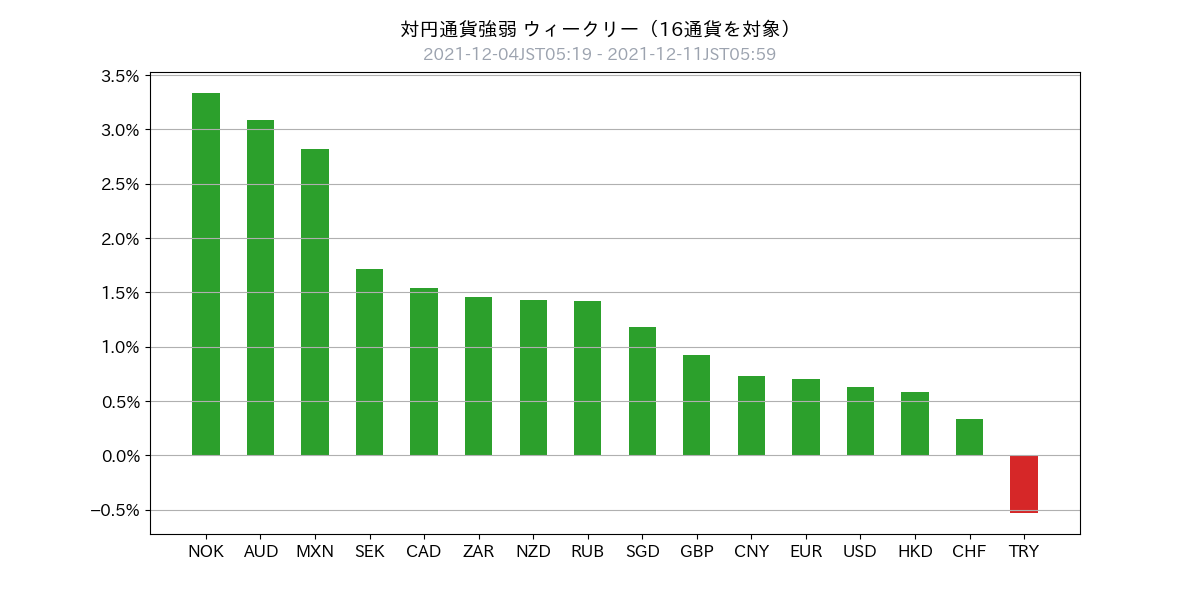

Last Week's Currency Strength

- Last week the dollar weakened (139/196 countries)

- Last week's currency strength is as followsOil-producing nations such as Norway > Chinese yuan > Euro > U.S. dollar > Japanese yen > Turkish lira

- The current market highlight is that the USD/JPY is rising as the dollar weakens. Conversely,when the dollar strengthens, there is a risk of selling emerging market currencies and buying the yen, so be mindful.

- There is also a high correlation between commodity prices and the movements of emerging market currencies. Last week, oil prices rebounded and NOK (Norway) was bought as a producer country.

- The Australian dollar turned bullish after the RBA policy meeting, but there is no major change observed, so excessive upside expectations should be avoided.

Global Macro Environment—Latest

- The market theme is gradually returning from “Omicron” to “U.S. monetary policy.”This is supported by existing vaccines remaining effective against Omicron, and vaccination progress reducing severe cases and fatalities.

- In such a context,market participants’ expectations for Federal funds rate hikes in the U.S. have moved up, with the first hike now anticipated for May 2022 and the second for September 2022.Inflation pressures are strong, and comments from Fed officials hinting at an earlier tapering completion have also influenced this.

- Risk-off factors include “Omicron,” deterioration of China’s real estate market (Evergrande, etc.), and the Russia-Ukraine issue.

- Risk-on factors include the potential passage of the Democratic Build Back Better bill and a rebound in commodity prices.

- This week, with the FOMC meeting on Wednesday, we aim to trade by capturing changes in U.S. monetary policy.

Global Macro Environment—Notes

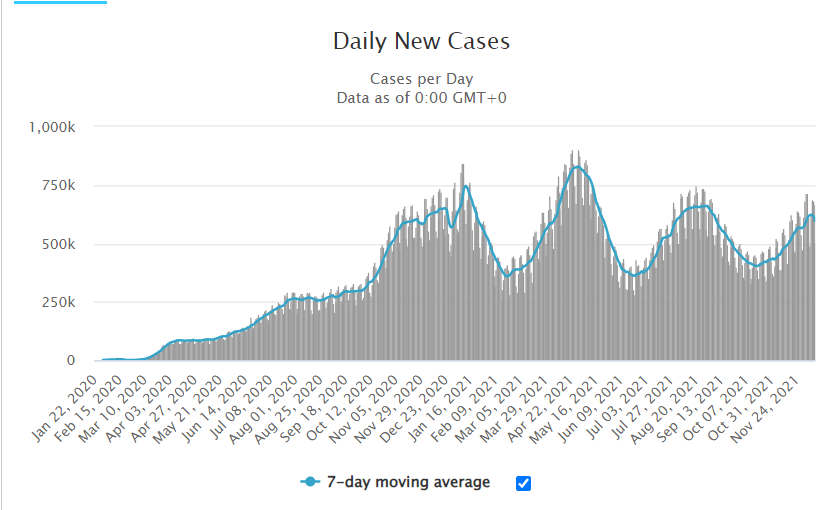

- The trend of new COVID-19 infections (7-day moving average) is moving toward a peak (attached chart Daily New Cases)

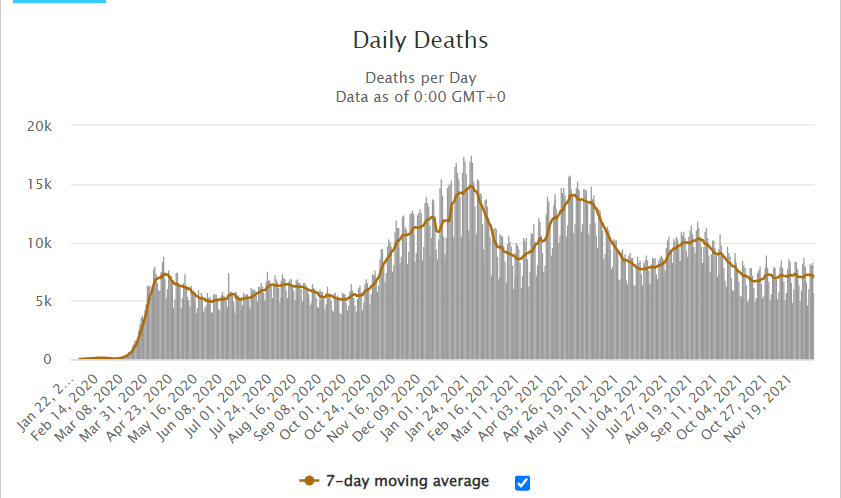

- New deaths have settled, and the Omicron spread does not seem to lead to as large an increase in fatalities as before (attached Daily Deaths chart)

COVID-19 new confirmed cases, excerpt from Worldometers

COVID-19 new confirmed cases, excerpt from Worldometers

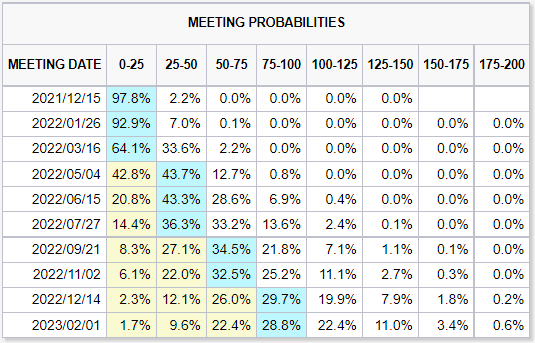

Market participants’ FOMC rate hike expectations, excerpt from CME Group

Chart Analysis

USD Index (Daily)

- Dollar Index is an indicator of overall dollar strength (composition of basket: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- In a dollar-strengthening environment, it moves within a 95.50–96.90 range

- Around 95.50, consider buying

USD/JPY Medium-term (Daily)

- Last week it retraced, but the daily chart shows upper levels weakening

- Selling on the retracements looks prudent seems reasonable

USD/JPY Short-term (Timeframe)

- If it moves higher, watch whether it can clearly clear the 113.80–114.00 level

EUR/USD Medium-term (Daily)

- In a downtrend, it trades around 1.1210–1.1370

- I would like to sell above 1.1350

EUR/USD Short-term (Timeframe)

- In a tighter range, 1.1230–1.1350

- Selling from 1.1330–1.1350 is also worth considering

USD/CNH Medium-term (Daily)

- Broke below the 6.35 lower bound, but rebounded to the upside for now. Background: increase in foreign currency reserve requirements

- From a chart perspective, selling on rallies seems favorable, but given rising U.S. yields, it is uncertain whether the yuan can strengthen further

USD/CNH Short-term (Timeframe)

- In the short term, selling rallies around 6.3790–6.38 may work

This Week's Toda's Trading Strategy

Overall Policy

- Market participants thin around year-end, so expect a volatile market; keep positions light

- Given the lack of clear direction, emphasize selling on the top of ranges and buying on the bottom

USD/JPY

- Last close: 113.38

- View: flat to slightly lower

- Intended range: 112.70–113.80

- Current position: USD/JPY ±0

- Expect the U.S. rate hikes to push the dollar/yen lower

- Short-term mildly bearish

- Trends are not strong, so we will aggressively seek pullbacks and ralliesbuy on dips, sell into rallies

EUR/USD, EUR/JPY

- Last close: EUR/USD 1.1311

- View: EUR/USD flat to lower; EUR/JPY lower

- Expected range: EUR/USD 1.1230–1.1350

- Current positions: EUR/USD ±0, EUR/JPY ±0

- Sell above 1.1330–1.1350; take profits around 1.1230

- If EUR/JPY rises toward around 129.00, consider selling

CNH/JPY, USD/CNH

- Last close: USD/CNH 6.3750

- View: USD/CNH flat to lower, CNH/JPY flat

- Expected range: USD/CNH 6.3000–6.4000

- Current positions: USD/CNH ± 0.0 CNH/JPY +1.5

- At market open, monitor whether 6.3790 acts as resistance, and look to sell

- However, with U.S. yields rising, avoid excessive expectations for the yuan; if yuan weakens, exit early

Subscriber-exclusive Discord Invite Code

Please apply via the URL below

※Please match the registered name with your GogoJungle nickname

Notes

× ![]()