Trade strategy considering differences between the fourth wave of COVID-19 and monetary policy [November 21–November 25]

Last Week's Foreign Exchange Range (Volatility Range)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 113.89 | 113.60 | 114.97 | 114.03 | +0.12% |

| EUR/USD | 1.1449 | 1.1250 | 1.1464 | 1.1281 | ▲1.47% |

| EUR/JPY | 130.40 | 127.97 | 130.61 | 128.63 | ▲1.36% |

| USD/CNH | 6.3791 | 6.3615 | 6.3981 | 6.3910 | +0.19% |

| CNH/JPY | 17.8554 | 17.7661 | 18.0032 | 17.8421 | ▲0.07% |

Last Week's Foreign Exchange Summary

USD/JPY

- Last week the dollar-yen rate started at 113.89 yen per dollar. The week began with a continuation of last week’s tone, as dollar buying was dominant, pushing into the 114 range. On Monday, strong U.S. October retail data and China’s October retail sales boosted the upside, and in Asian trading on Wednesday it rose to a year-to-date high of 114.71 and then to 114.97. Afterward, it faced a pullback from the high area, retreating to the lower-114s by Friday. On Friday it rose again to around 114.50, but when a lockdown in Australia was announced during European hours, the dollar weakened against the yen amid Australian dollar selling, briefly pushing to 113.60. As the week ended, gains were reversed, and in the weekend the market recovered on expectations for a U.S. Democratic Party bill, closing at 114.03 yen.

EUR/USD

- The euro started at 1.1449 dollars per euro. Following last week’s trend, there was euro selling and dollar buying, with a gradual decline. On Monday in New York time, it fell below 1.1400, and by Asia time on Wednesday it fell below 1.1300. A stop-loss cascade pushed it down to 1.1264, but it recovered through Thursday. However, on Friday, news of Australia’s lockdown accelerated euro selling, touching the week’s low at 1.1250 before closing at 1.1281.

USD/CNH

- The yuan started at 6.3791 per dollar. Early in the week, dollar weakness and yuan strength dominated, pushing briefly to 6.3615, but comfort with gains led to a rapid rebound to 6.3981. It then fluctuated and closed at 6.3910.Compared with the dollar/yen and euro, it showed a steadier trend.

What Happened Last Week

※ Price indices and monetary statistics are year-on-year, GDP is quarter-on-quarter, and indicators without specific notes are month-on-month or for the current month.15th

- Japan Q3 2023 GDP at an annualized rate: ▲0.8%

- China October retail sales +9.8% (very strong)

- China October industrial production +3.5% (year-on-year)

- Japan September capacity utilization ▲7.3%

- Eurozone September trade balance +€7.3 billion

- ECB President Christine Lagarde said that tightening policy now would hurt the economy when inflation cools, denying market expectations of earlier rate hikes.

- November New York Fed manufacturing index 30.9 (very strong)

- U.S. tapering (reduction of monetary easing) began

- Online talks between President Biden and Chinese President Xi Jinping: held to clash at hard lines on Taiwan and human rights. They agreed to pursue de-escalation, but highlighted deeper rifts between the countries about the path to easing tensions.

16th

- U.S. October retail sales +1.7% (strong)

- U.S. October industrial production +1.6% (strong)

- China’s Communist Party released the full text of the "Historical Resolution" adopted at an important meeting on the 11th. It would be the third historical resolution following Mao and Deng, but did not include the explicit Deng-era bans on "cult of personality" or "collective leadership." Under Xi Jinping's long tenure, the party's collective leadership could face a turning point.

17th

- Japan October trade statistics ▼¥67.4 billion (weak)

- Japan September machinery orders +0.0%

- U.S. October housing starts ▼0.7%

- U.S. October building permits +4.0%

18th

- Initial jobless claims for the previous week: 268K (nearing pre-pandemic levels)

- Philadelphia Fed Manufacturing Index for November: 39.0 (very strong)

- October leading indicators +0.9%

- South Africa Reserve Bank raised policy rate by 0.25% to 3.75%

- Philippines central bank kept the policy rate at 2% for the fourth consecutive meeting. Inflation exceeded target, but outlook remained uncertain.

- Turkish central bank cut the one-week repo rate from 16% to 15%. In a world of tighter policy by other central banks, the lira continued to slump.

- U.S. Biden administration's EV incentives faced pushback from Mexico and Canada. North American leaders' summit highlighted differences. As EV adoption accelerates, a more inward-leaning stance could affect North American auto competitiveness.

19th

- Japan October CPI +0.10% (low inflation pressure)

- Eurozone September current account +€26.9 billion

- ECB President Lagarde said inflation will fall and argued the ECB should not tighten policy further.

- U.S. House passed a spending bill enabling $1.75 trillion over 10 years for child care and climate measures; Senate debate begins. Party leadership aims for Senate passage this year, but expectations of revisions remain, rendering Biden's signature policy uncertain.

- U.S. Defense Secretary Austin spoke at a Manama conference in Bahrain, warning that if Iran does not adopt a serious stance on its nuclear issue, the U.S. will consider all options to safeguard its security. He also said diplomacy would continue.

- The government announced an economic package with record high fiscal spending of 55.7 trillion yen. It aims for scale comparable to global standards, but growth-focused measures comprise only about 20%.With post-pandemic competition in mind, multi-year investments in renewable energy and infrastructure in the U.S. and Europe are starting; Japan should focus on growth areas like environment and digital while cutting waste.

- The government disclosed that it is considering releasing national oil reserves.In response to rising crude prices, the U.S. has asked allies like Japan and South Korea to release reserves to temporarily increase supply and prevent price spikes.

- Several Federal Reserve leaders signaled possible faster tapering pace starting in November.Concerns about persistent high inflation have grown. They aim to finish around mid-2022 and to move on to rate hikes sooner.

Glossary of Economic Terms

- GDP = Gross Domestic Product; high growth is favorable

- CPI = Consumer Price Index: many advanced economies target 2%

- PCE = Personal Consumption Expenditures: closely related to consumer prices

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Manager Index: 50 is the baseline

- ZEW = Leibniz Centre for European Economic Research: 0 is the baseline

- NAHB = National Association of Home Builders: 50 is the baseline

- NY Fed Manufacturing Index: 0 is the baseline

- Philly Fed Manufacturing Index: 0 is the baseline

- Richmond Fed Manufacturing Index: 0 is the baseline

- Chicago PMI: 50 is the baseline

- University of Michigan Consumer Sentiment Index: indexed with 100 in 1966

- S&P/Case-Shiller Home Price Index: "20-Ccity Composite" is widely used for housing market trends

- Pending Home Sales Index: measures contracts signed but not yet delivered

- European Consumer Confidence: indexed to 100 for 2000–2020 average; released as a month-on-month figure

- European Economic Sentiment Index: indexed to 100 for 2000–2020 average; released as a real value

- Consumer Confidence Index: indexed with 100 in 1985

- Japan Coincident Economic Indicators: indexed with 100 in 2015

- Japan’s “Economy Watchers” sentiment index: baseline 50

- Japan Corporate Goods Price Index: baseline 0

Key Economic Indicators and Political Events

22nd

- China & ASEAN Leaders' Summit

- 10:30 China PBOC policy rate announcement

- 17:30 Hong Kong CPI

- 27:00 U.S. 2-year Treasury note auction

- 27:00 U.S. 5-year Treasury note auction

23rd

- Japan Holiday (Labor Thanksgiving Day)

- 06:45 Australia Q3 2023 retail sales

- 23:45 U.S. November Markit PMI (flash)

- 24:00 November Richmond Fed manufacturing index

- 27:00 U.S. 7-year Treasury auction

24th

- 10:00 RBNZ policy rate

- 22:30 Initial jobless claims for previous week

- 22:30 U.S. October durable goods orders

- 24:00 U.S. October personal consumption expenditures (PCE deflator)

- 24:00 U.S. October new home sales

- 28:00 FOMC minutes

25th

- U.S. holiday (Thanksgiving)

26th

- 08:30 October Tokyo metropolitan area consumer price index

From Next Week

※ From here on (“Last Week's Currencies Strengths/Weaknesses”“Global Macro Environment Overview”“Chart Analysis”“This Week's Todan Trading Strategy”) this is a paid article

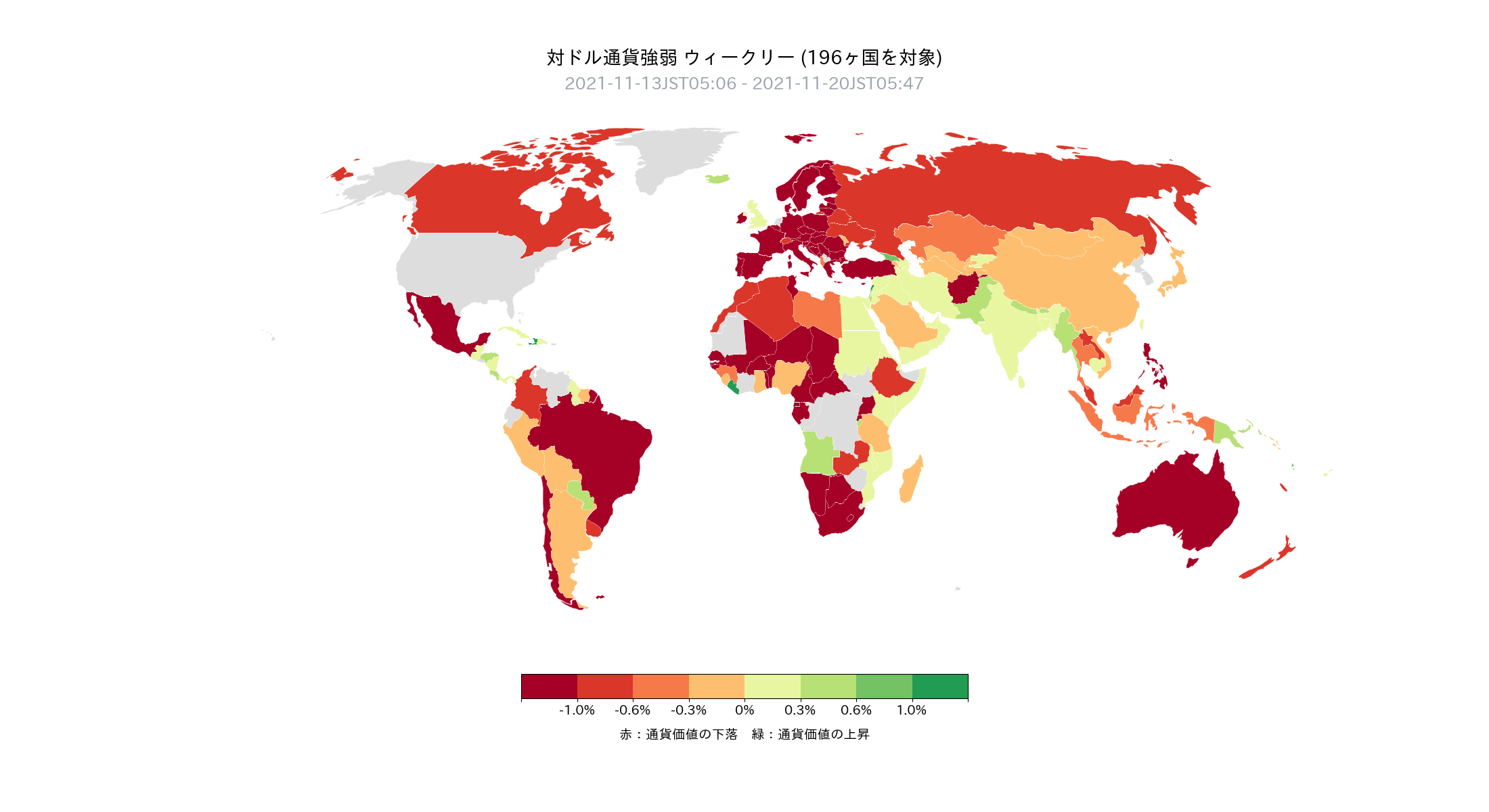

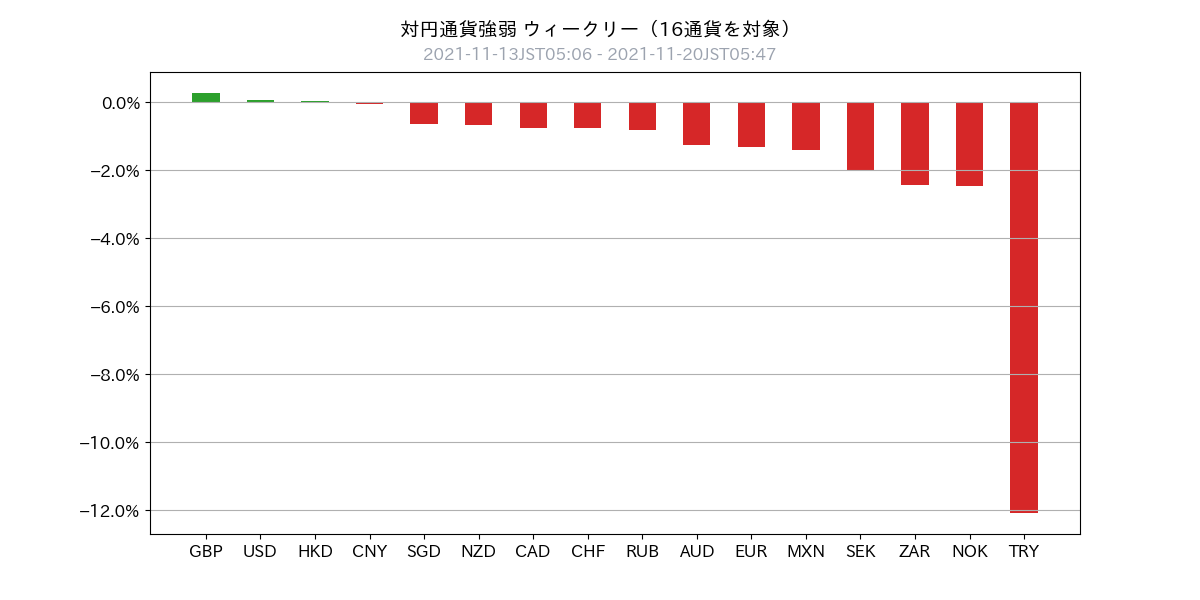

Currency Strength Last Week

- Last week, the dollar strengthened against major currencies (123/196 countries)

- Reasons include strong U.S. economic data, rising U.S. inflation pressure, and rising U.S. interest rates

- Among major currencies, the only one that appreciated more than the dollar was the British pound

- Behind this is the expectation of early rate hikes in the U.K., with several meetings anticipated to hint at further rate increases

- In a dollar-strengthening environment, USD/JPY and cross-yen pairs have struggled to advance

- The backdrop is that, due to dollar strength, vulnerable emerging market and commodity currencies are being sold, and the yen is being bought back

- Note that the Turkish lira has collapsed due to the central bank cutting rates contrary to the theory

- In summary, currency strength is as followsBritish pound > U.S. dollar > Japanese yen > Chinese yuan > Euro > Resource/emerging market currencies > Turkish lira

Global Macro Environment Review (Latest)

- The major themes in the current market are “supply chain disruption” and “commodity inflation,” which have fed global “inflationary pressures” and consequently “differences in monetary policy.”

- Among the factors pushing U.S. inflation are the question of whether the Build Back Better Act will pass Congress. The bill passed the House with a majority last week and is moving to the Senate for consideration.

- In this environment,some Fed participants have suggested an earlier tapering and faster reduction in accommodation.

- It remains important to continue monitoring U.S. monetary policy, notably the FOMC.We think so.

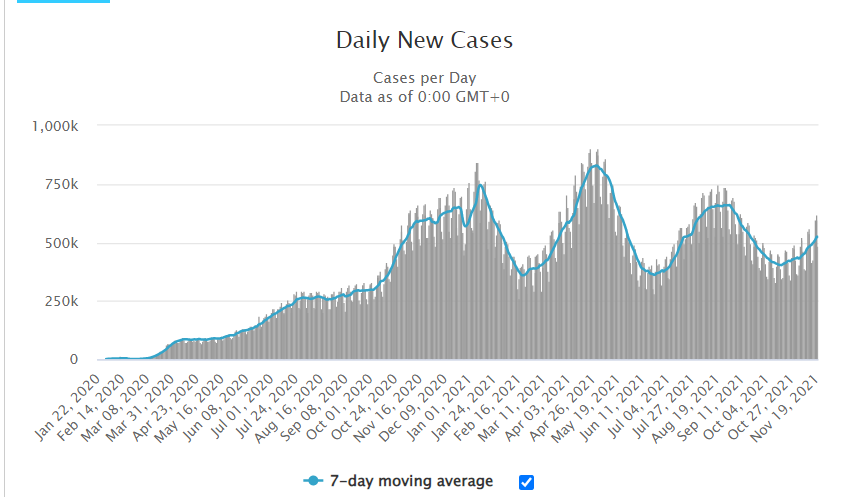

- with Australia reopening lockdowns nationwide, attention is also on a potential fourth wave of COVID-19that could influence developments.

- The fourth wave of COVID-19 is viewed as a factor that could dampen inflation

- In this environment, market expectations for U.S. policy rate hikes remain centered on the first hike in June 2022 and the second in September 2022 (the outlook is largely unchanged from last week)

- We should continue to monitor inflationary pressures in traded currencies and the impact of COVID-19as a key area to watch.

Global Macro Environment Summary (Supplement)

- New COVID-19 infections are trending up somewhat, raising concerns about a potential fourth wave (Daily New Cases chart attached below uses a 7-day moving average)

- HoweverAustralia's ongoing strict measures suggest these are likely temporary global moves to be mindful of.

- The Fed views supply constraints as uncertain regarding when they will ease

- The ECB believes supply constraints will ease by next year at the latest

- Several advanced central banks point to not only supply constraints but also strong demand recovery as major drivers of current inflation pressures

- The Reserve Bank of Australia aims to delay easing to avoid choking the economy, given relatively low inflation pressures

- The Bank of England signals rate hikes within the next few months; among Five Eyes currencies, the U.K. is expected to raise rates the earliest

COVID-19 new cases, excerpt from Worldometer

Chart Analysis

USD Index (Daily)

- The USD index indicates the overall strength of the dollar (basket composition: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Next resistance is around the June 2020 high, about 97.65

USD/JPY Medium Term (Daily)

- Note that daily range is widening

- The view remains that it will continue to range or trend higher

USD/JPY Short Term (Intraday)

- 113.80 and 114.40 have both broken to the upside and downside but still serve as reference levels

EUR/USD Medium Term (Daily)

- Next support is the June 2020 low at 1.1210

- The next level to watch is around 1.0770

EUR/USD Short Term (Intraday)

- Sell rallies around 1.1300–1.1350

USD/CNH Medium Term (Daily)

- Range continues between 6.3500 and 6.4250

- Within a range, buying CNY to earn swap points seems favorable

USD/CNH Short Term (Intraday)

- No clear trend in the short term

This Week's Todo: Toda’s Trading Strategy

Overall Approach

- Favor buying the dollar

- The U.S. economy is strong, early tapering expectations are present, and the dollar index is breaking resistance, so selling is not necessary

- Favor buying the yuan

- The U.S.-China rate differential is around 2.3%, domestic inflationary pressures make yuan weakness unlikely. The yuan is the only currency that can be bought more than the dollar

- Sell the yen and the euro first

- However, be mindful that if crude oil prices fall, the yen may be bought back

- The euro shows a clearer downtrend

USD/JPY

- Last Friday's close: 114.03

- View: range-bound to slightly higher

- Expected range: 113.30–115.00

- Current position: USD/JPY flat (±0)

- More upside bias, but monitor for possible yen strength on crude oil declinesas a precaution

- Keep long-term positions to other currencies; focus on buying low, selling highwhen possible

- Lower bound: 113.30–113.80, upper bound: 114.50–115.00

EUR/USD, EUR/JPY

- Last Friday's close: EUR/USD 1.1281

- View: EUR/USD range-bound to lower; EUR/JPY range-bound to lower

- Expected range: EUR/USD 1.1110–1.1350

- Current positions: EUR/USD ±0, EUR/JPY ±0

- If selling euros yields profits, hold positions through the week

- Consider selling above 1.1300

- Plan to sell below last week's low of 1.1250

CNH/JPY, USD/CNH

- Last Friday's close: USD/CNH 6.3910

- View: USD/CNH range-bound, CNH/JPY range-bound to slightly up

- Expected range: USD/CNH 6.3500–6.4250

- Current positions: USD/CNH ± 0.0, CNH/JPY +6.0

- When USD/JPY moves higher (around the upper 114s), take profits on half the position

Discord Invite Code for Subscribers

Please apply from the URL below

Please align the registered name with your GogoJungle nickname

Notes

All content in this newsletter is protected by copyright and may not be reproduced without permission. The newsletter is for information purposes only, and its accuracy is not guaranteed by us or the information provider. Contents may change due to changes in economic conditions. Users should rely on their own judgment and consult professionals (law, accounting, tax, etc.) for individual matters. If users incur damages from using this information, we and the information provider are not liable for any damages, regardless of the cause.