[November 15 – November 19] Trading strategy considering inflation pressures in various countries

Last Week's Foreign Exchange Range (Volatility)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 113.36 | 112.72 | 114.31 | 113.92 | +0.49% |

| EUR/USD | 1.1555 | 1.1433 | 1.1608 | 1.1444 | ▲0.96% |

| EUR/JPY | 131.13 | 130.25 | 131.44 | 130.40 | ▲0.56% |

| USD/CNH | 6.3953 | 6.3712 | 6.4077 | 6.3805 | ▲0.23% |

| CNH/JPY | 17.7262 | 17.6297 | 17.9074 | 17.8575 | +0.74% |

Last Week's Foreign Exchange Summary

USD/JPY

- Last week's dollar-yen moved from 113.36 to start. Early in the week, dollar selling led, pushing briefly to 112.72 by Tuesday. The range around 112.80 persisted afterward, but on Wednesday, with the release of China's October Producer Price Index showing high inflation pressure (+13.5%), U.S. yields rose, quickly driving the dollar higher. In New York trading on Wednesday, the U.S. October CPI also showed strong inflation (+6.2%), pushing yields and the dollar higher, with a sharp rebound to 114.00.On Friday it rose to 114.31 temporarily, but selling predominated at that level, and the week closed at 113.92.

EUR/USD

- The euro started at 1.1555 per euro. Early in the week, euro buying and dollar selling prevailed, gradually rising, reaching 1.1608 on Tuesday. Later, strong October Chinese PPI reversed the trend, and with U.S. October CPI confirming higher inflation pressure, the pair fell below the recent low of 1.1530. On Friday it briefly dropped to 1.1433 and otherwise closed the week weakly at 1.1444.

USD/CNH

- The yuan began at 6.3953 per dollar. In the first half of the week, movement was modest, but after the U.S. October CPI release on Wednesday, dollar buying dominated and the pair rose to 6.4077. Thereafter, with no particular catalysts, Thursday and Friday saw yuan buying during European hours, pulling back to 6.3712 before closing at 6.3805.

Last Week's Notable Events

Note: Price indices and money statistics are year-on-year percentages; GDP is quarter-on-quarter; indicators without specific notes are month-on-month or current-month figures8th

- Japan September Leading Index (CI) – Flash: 99.7

- U.S. Federal Reserve Vice Chair Lael Brainard indicated vigilance on inflation, suggesting conditions for rate hikes could be met by the end of 2022. The President of the Federal Reserve Bank of St. Louis, James Bullard, said on the same day that if high inflation persists, action should be taken sooner, forecasting two rate hikes in 2022. Regarding the tapering of asset purchases starting in November, Bullard mentioned the possibility of ending earlier than currently expected in mid-2022.

9th

- Japan September current account balance +1.033 trillion yen

- Japan October Economy Watchers Survey: Current 55.5; Outlook 57.5

- Euro area November ZEW Economic Sentiment: 25.9

- U.S. October Producer Price Index (PPI) +8.6%

10th

- Japan October M2 Money Stock (YoY) +4.2%

- China October CPI +1.5%

- China October PPI +13.5% (very strong inflation pressure)

- U.S. October CPI +6.2% (very strong inflation pressure)

- U.S. initial jobless claims for the week ending

11th

- Japan October Domestic Corporate Goods Price Index +8.0%

- Mexico's central bank raised policy rate by 0.25% to 5.0%

- Communist Party of China closed its 6th Plenary Session of the 19th Central Committee. Adopted the third "historical resolution" following Mao Zedong and Deng Xiaoping. Xi Jinping solidified authority to potentially serve a rare third term starting next autumn..

- China's annual Singles' Day online shopping festival ended at 00:00 on the 12th (1:00 JST). Alibaba reported that during the sale period, turnover reached a new high of 540.3 billion yuan (about 9.56 trillion yen).

- EU Commission published autumn economic forecast, markedly revising up euro-area inflation projections. For 2021, from 1.9% to 2.4%; for 2022, from 1.4% to 2.2%. Higher energy prices and supply chain constraints mean inflation will stay above the ECB's 2% target for the near term.

12th

- Eurozone September industrial production (MoM) +5.2%

- U.S. September JOLTS job openings 10.4M

- APEC online summit in which 21 economies, including Japan, the U.S., China, and Taiwan, participatedand discussed TPP membership, with mutual support expressed.

- UK COP26 climate conference closed late; negotiations over coal and fossil fuel reductions and funding from developed nations continued to face difficulties

Glossary of Economic Terms

- GDP = Gross Domestic Product; high growth is favorable

- CPI = Consumer Price Index: many advanced economies pursue a 2% target

- PCE = Personal Consumption Expenditures: closely related to consumer prices

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Manager Index: 50 is the dividing line

- ZEW = Leibniz Centre for European Economic Research: 0 is the baseline

- NAHB = National Association of Home Builders: 50 is the baseline

- ISM manufacturing index (New York Fed): 0 is the baseline

- Philadelphia Fed manufacturing index: 0 is the baseline

- Richmond Fed manufacturing index: 0 is the baseline

- Chicago Purchasing Managers Index: 50 is the baseline

- University of Michigan Consumer Sentiment Index: indexed with 1966=100

- S&P/ Case-Shiller Home Price Index widely used: 20-CMS housing price index important for monitoring housing market's impact on the economy

- Pending home sales index: measures homes under contract but not yet closed

- Euro area Consumer Confidence Index: index uses 2000-2020 average of 100; releases are month-over-month

- Euro area Economic Sentiment Index: index uses 2000-2020 average of 100; releases are actual values

- Consumer Confidence Index: indexed with 1985=100

- Japan Economy Watchers Survey: indexed with 2015=100

- Japan Business Outlook Survey: 50 is the baseline

- Japan's Corporate Activity Index: indexed with 0 as the baseline

Key Economic Indicators and Political Events

15th

- 08:50 Japan Q3 7-9 months GDP (real)

- 11:00 China October Retail Sales

- 11:00 China October Industrial Production

- 13:30 Japan September Capacity Utilization

- 19:00 Euro Area September Trade Balance

- 19:00 Lagarde ECB President speaks (Introductory statement by Ms Lagarde at the Hearing before the ECON Committee of the European Parliament)

- 22:30 November NY Fed Manufacturing Index

- U.S.-China summit (online)

- Start of U.S. tapering (reduction of monetary stimulus)

- Lemond U.S. Commerce Secretary and USTR representatives to visit Japan

16th

- 09:30 Previous RBA minutes

- 22:30 U.S. October Retail Sales

- 23:15 U.S. October Industrial Production

17th

- 08:50 Japan October Trade Statistics

- 16:00 UK October CPI

- 17:00 South Africa October CPI

- 22:30 Canada October CPI

- 22:30 U.S. October Housing Starts

- 22:30 U.S. October Building Permits

- 25:00 Russia Q3 2022 GDP (Flash)

18th

- 22:30 Previous week initial jobless claims

- 22:30 November Philadelphia Fed Manufacturing Index

- 24:00 October Leading Economic Index

- North American leaders' summit

19th

- 08:30 Japan October CPI

- 17:30 Lagarde ECB President speaks (Speech by Ms Lagarde at Hessischer Europas Empfang "The Future of Europe")

- 18:00 Euro Area September Current Account

- Middle East security (Manama Dialogue)

- Guangzhou International Auto Show

Next Week and Beyond

- Nov 26: Black Friday

- Dec 14–15: FOMC meeting (with dot plots and projections)

- Dec 16: ECB meeting

- Dec 16–17: Bank of Japan Policy Board meeting

- Jan 17–21: Davos World Economic Forum

- Jan 18: Bank of Japan Policy Board meeting (outlook for economy and prices)

- Jan 26: FOMC

- Feb 3: ECB

- Mar 10: ECB

- Mar 16: FOMC (with projections)

- Mar 18: BOJ Policy Board meeting

- Apr 14: ECB

- Apr 28: BOJ Policy Board meeting (outlook for economy and prices)

- May 4: FOMC

- Jun 9: ECB

- Jun 15: FOMC (with projections)

- Jun 17: BOJ Policy Board meeting

- Jul 21: BOJ Policy Board meeting (outlook for economy and prices)

- Jul 21: ECB

- Jul 27: FOMC

- Sep 8: ECB

- Sep 21: FOMC (with projections)

- Sep 22: BOJ Policy Board meeting

- Oct 27: ECB

- Oct 28: BOJ Policy Board meeting (outlook for economy and prices)

- Nov 2: FOMC

- Dec 14: FOMC (with projections)

- Dec 15: ECB

- Dec 20: BOJ Policy Board meeting

From here on (“Last Week's Currency Strength/Weakness,” “Global Macro Environment Overview,” “Chart Analysis,” and “This Week's Toda Trading Strategy”) are paid articles

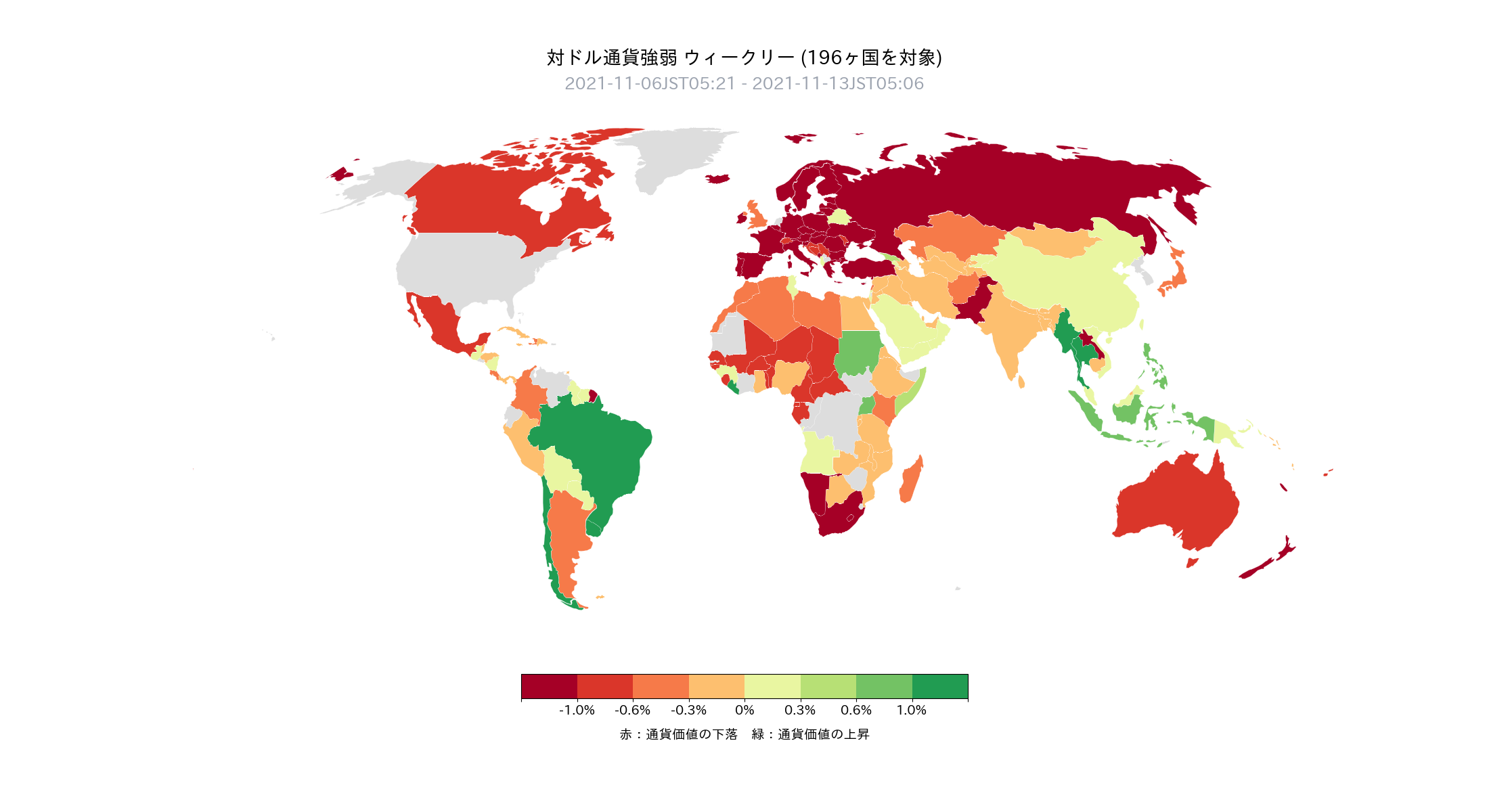

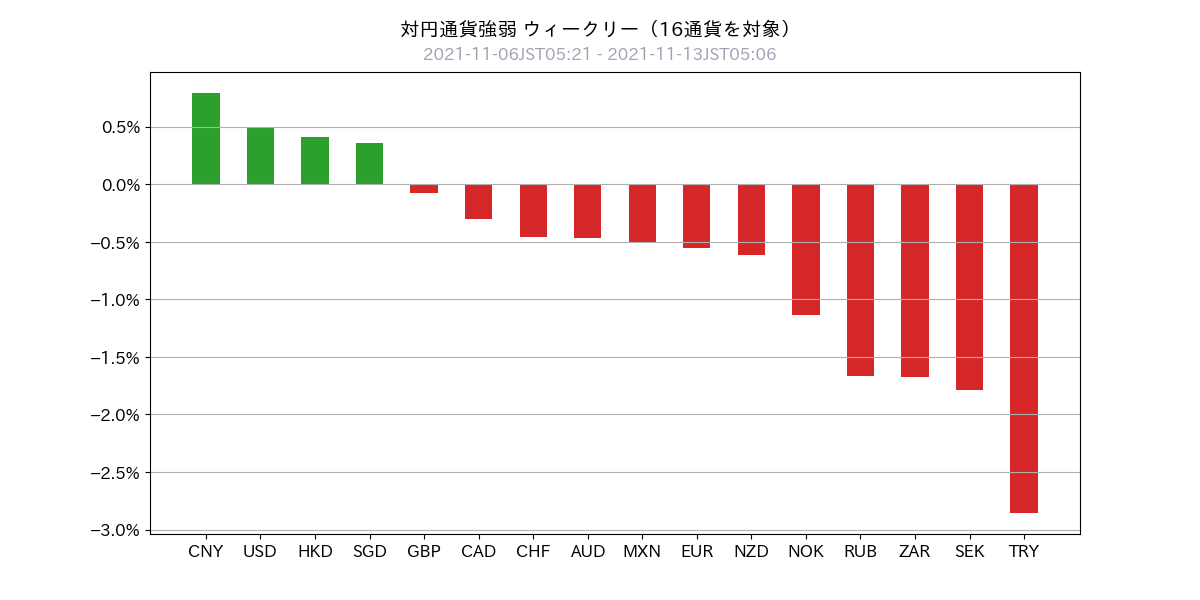

Last week's currency strength

- Last week the dollar strengthened against many currencies (across 160 of 196 countries)

- Backgrounds include rising U.S. inflation pressures and higher U.S. interest rates

- The only major currency that attracted more than the dollar was the yuan

- Underlying reasons include high inflation pressures, with a belief that yuan depreciation is less likely to ignite further inflation

- In a stronger dollar environment, USD/JPY held firm, but manycrosses struggled to advance

- Especially noticeable were selling pressures on emerging market and commodity currencies

- In summary, currency strength/weakness was as followsyuan > USD > JPY > EUR > commodity and emerging market currencies

Global macro environment整理(最新版)

- The current major themes are “supply-chain disruption” and “rising commodity prices,” which feed global “inflation pressures” and consequently lead to differences in monetary policy.

- Last week, inflation pressures in China producer prices and U.S. consumer prices rose, fueling expectations for earlier rate hikes in the U.S.,and there was increased speculation that rate hikes could occur during the tapering process.

- Whether the U.S. Democratic Build Back Better bill passes Congress is also a focal point

- As inflation pressures mount, questions about whether additional budgets are needed may be emerging

- The Fed began tapering (reducing asset purchases) on November 15, aiming to complete by June next year

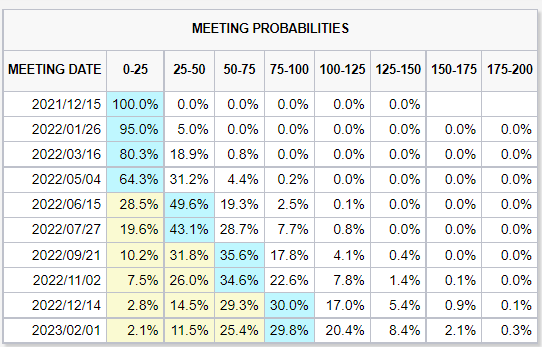

- Market participants’ views on U.S. policy-rate hikescenter on the first hike around June 2022 and the second around September 2022(the outlook has moved earlier than last week)

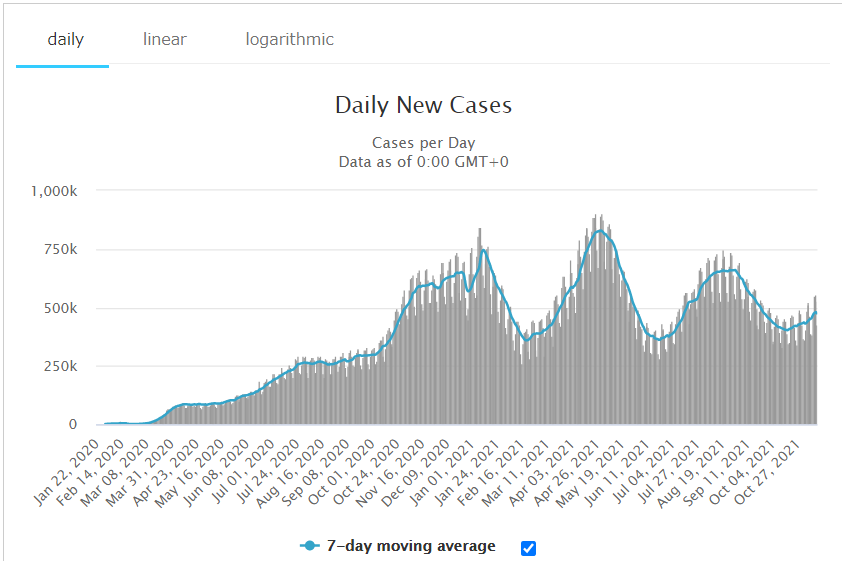

- The trend in new COVID-19 cases has turned slightly upward (Daily New Cases chart attached below shows 7-day moving average)

- We should continue to monitor inflation pressures in the currencies we tradeand consider them carefully.

Global macro environment整理(補足)

- The Fed views supply constraints as uncertain as to when they will ease

- The ECB projects supply constraints to ease over the next year

- Several advanced central banks point to not only supply constraints but also demand recovery as major factors behind current inflationary pressures

- Australia's central bank seeks to delay easing to avoid a growth slowdown, due in part to relatively low inflation pressures

- The Bank of England has signaled rate hikes in the coming months; among Five Eyes currencies, the UK seems to tighten the fastest

COVID-19 new cases, excerpt from Worldometers

Chart Analysis

USD Index (daily)

- Dollar Index is a measure of the dollar’s overall strength (currency basket composition: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Clear break above resistance at 94.70

- In the near term, there is room to rise smoothly with no major resistanceto hinder ascent.

USD/JPY Mid-term (daily)

- Recent range judged at 112.20–114.40

- Last week fell to 112.72 but then rallied, testing the 114.40 resistance again

- If 114.40 is decisively cleared, upward momentum may continue

USD/JPY Short-term (hourly)

- Treat 113.80 as a short-term support

- If the pair holds above this level, the upside view for next week seems reasonable

EUR/USD Mid-term (daily)

- Downward trend continues, breaking below 1.1530 support

- In the near term there is no major support; prefer selling on rallies

EUR/USD Short-term (hourly)

- Set upside for selling on rallies around 1.1490

USD/CNH Mid-term (daily)

- Broad range roughly 6.35–6.60

- Narrow range 6.35–6.4250

- Still see a trend of dollar weakness and yuan strength continuing

- Be mindful that 6.35 may be tested this week

USD/CNH Short-term (hourly)

- Retracement target around 6.3900–6.3950

This Week's Toda Trading Strategy

Overall policy

- Dollar-buying bias

- U.S. economy is solid, inflation fears rising push U.S. rates higher, and the USD Index is breaking resistance, so selling to initiate may not be necessary

- Yuan-buying bias

- Interest rate differentials between the U.S. and China are around 2.3%, domestic inflation pressures make yuan depreciation less likely; yuan is the only currency that can be stronger than the dollar

- JPY and EUR are biased to selling

USD/JPY

- Last Friday’s close: 113.92

- View: flat to higher

- Expected range: 113.50–115.50

- Current position: USD/JPY at around ±0

- Consider buying on dips around 113 yen

- Take profits around 114.40, with more on a breakout

- If 114.40 is decisively cleared, re-enter long USDto ride higher

EUR/USD, EUR/JPY

- Last Friday’s close: EUR/USD 1.1444

- View: EUR/USD flat to lower; EUR/JPY flat

- Expected range: EUR/USD 1.1300–1.1530

- Current positions: EUR/USD ±0; EUR/JPY ±0

- Sell on rallies above 1.1490

- Take profits based on orders and indicators as appropriate.

CNH/JPY, USD/CNH

- Last Friday’s close: USD/CNH 6.3805

- View: USD/CNH flat to lower; CNH/JPY flat to higher

- Expected range: USD/CNH 6.3000–6.4000

- Current positions: USD/CNH ± 0.0; CNH/JPY +7.0

- Expect a break below 6.35 and hold yuan long

- If USD/JPY breaks lower, plan to reduce half of the position

Subscriber-only Discord Invitation Code

Please apply using the URL below

※Please align the registered name with your GogoJungle nickname

Notes

Unauthorized reproduction or copying of any content in this e-newsletter is prohibited. This newsletter is created solely for information provision, and its accuracy is not guaranteed by us or the information sources. Content may change due to changes in economic conditions. Please use the information at your own risk and consult professionals in law, accounting, tax, etc. If users suffer damages from using this information, we and the information providers do not assume liability regardless of the cause.