[November 8–12] Trade strategy considering the enacted U.S. BIB (bipartisan infrastructure) and the unpassed BBB (Democrat) bill

Last Week's Foreign Exchange Range (Fluctuation Range)

| Opening Price | Low | High | Closing Price | Change | |

|---|---|---|---|---|---|

| USD/JPY | 114.11 | 113.29 | 114.46 | 113.40 | ▲0.62% |

| EUR/USD | 1.1559 | 1.1513 | 1.1617 | 1.1566 | +0.06% |

| EUR/JPY | 131.95 | 130.82 | 132.58 | 131.16 | ▲0.60% |

| USD/CNH | 6.4042 | 6.3909 | 6.4087 | 6.3925 | ▲0.18% |

| CNH/JPY | 17.7973 | 17.7104 | 17.8812 | 17.7312 | ▲0.37% |

Last Week's Exchange Rate Summary

USD/JPY

- Last week's USD/JPY started at 114.11. Early in the week, after the Liberal Democratic Party won an outright majority in the House of Representatives, stocks rose and the yen weakened, pushing to 114.46. At that level, selling intensified and it gradually retreated. On Tuesday, the Reserve Bank of Australia signaled a more dovish stance than markets expected, accelerating AUD selling, and driven by AUD/JPY selling, USD/JPY slipped below the 114 level. Thereafter, it hovered in the upper 113s, but cross-yen selling remained strong, and by the weekend it fell to 113.29 and closed at 113.40.

EUR/USD

- The euro started at 1.1559 per euro. Early in the week, euro buying regained strength, rising toward around 1.1620. However, at that level the upside was limited, and movement settled in the mid-1.15s. On Thursday, the Bank of England surprised markets by keeping rates unchanged, sending the pound lower and dragging the euro down below 1.1550. On Friday, strong US October payrolls briefly pushed it to 1.1513, but buying returned toward the close, finishing at 1.1566.

USD/CNH

- The yuan began at 6.4042 per USD. Throughout the week it traded in a narrow range around 6.40. Chinese authorities appeared to manage the USD/CNH rate while conducting short-term liquidity operations. The weekend closed slightly lower at 6.3925.

Last Week's Events

※ Price indices and monetary statistics are year-on-year unless otherwise noted; GDP is quarter-on-quarter; indicators without special notes are month-on-month or current-month figures1st

- China October Caixin Manufacturing PMI 50.6

- U.S. October ISM Manufacturing Index 60.8

- House of Representatives election:All 465 seats from single-member districts and proportional representation were decided.The Liberal Democratic Party won 261 seats including additional nominees, reaching an absolute majority on its own.Constitutional Democratic Party of Japan 96, Japan Innovation Party 41, Komeito 32, Democratic Party for the People 11, Communist Party 10, Reiwa Shingikai 3, Social Democratic Party 1. Independents 10.

2nd

- The Reserve Bank of Australia scrapped its target for mid-term (3-year) bond yields at 0.1%.

- Bank of Japan released minutes from the Sept. 21–22 Policy Board meeting, noting a view among members that inflation would turn modestly positive as energy prices rise.

- Several U.S. media reported that Democratic incumbent Phil Murphy won the New Jersey governor’s race. Murphy was thought to be ahead but results were closer than expected, reflecting voter dissatisfaction with President Biden’s administration.

- Toyota and three other Japanese automakers reported October U.S. new-vehicle sales down 28% year over year to 300,000 units, the third straight month of declines. Ongoing semiconductor shortages constrained production, worsening from September’s 23% drop.

3rd

- Japanese holiday (Culture Day)

- China Caixin October Services PMI 53.8

- Euro Area September Unemployment Rate 7.4%

- U.S. October ADP Employment Change +571,000 (strong)

- U.S. October ISM Non-Manufacturing PMI 66.7 (strong)

- U.S. September Manufacturing New Orders +0.2%

- Federal Reserve announced it would begin tapering asset purchases from November. In November, purchases would be reduced by 1200 billion dollars per month cumulatively, with the pace set to zero by June 2022; specifically, U.S. Treasuries will be reduced by 100 billion and MBS by 50 billion monthly, totaling 150 billion.

- China's National Health Commission reported 109 new cases on the 2nd; the daily new cases above 100 mark had not occurred for about three months since Aug 10.

4th

- Russia Holiday (Unity Day)

- Euro Area September Producer Price Index +2.7%

- Bank of England kept rates unchanged despite expectations, hinting at potential rate hikes at upcoming meetings.

- U.S. September Trade Balance -$80.9 billion

- U.S. initial jobless claims for the previous week near pandemic levels at 269,000

- OPEC+ decided not to increase oil production; warned that demand may slow as COVID-19 cases rise, sticking to a zero-sum response to production requests from consuming nations like the U.S. and Japan.

5th

- Euro Area September Retail Sales -0.3%

- U.S. October Employment report: Nonfarm payroll +531,000; Unemployment Rate 4.6%

- Canada October Employment: +31,000; Unemployment 6.7%

- Biden administration's flagship infrastructure bill of about $1 trillion becomes reality. The Senate had approved it in August; it awaits presidential signature.

Economic Terminology

- GDP = Gross Domestic Product; higher growth is favorable

- CPI = Consumer Price Index; many advanced economies aim for a 2% target

- PCE = Personal Consumption Expenditures; closely correlates with consumer prices

- PPI = Producer Price Index; influences CPI

- PMI = Purchasing Manager Index; 50 is the threshold

- ZEW = Leibniz Centre for European Economic Research; 0 is the baseline

- NAHB = National Association of Home Builders; 50 is the baseline

- New York Fed Manufacturing Index: 0 is baseline

- Philadelphia Fed Manufacturing Index: 0 is baseline

- Richmond Fed Manufacturing Index: 0 is baseline

- Chicago Purchasing Managers Index: 50 is baseline

- University of Michigan Consumer Sentiment Index: indexed with 1966=100

- S&P/Case-Shiller Home Price Index widely used; tracks housing market impact on the economy

- Housing Market Pending Index: measures number of contracts signed but not yet closed

- European Consumer Confidence Index: 100 is average for 2000–2020, reported month-to-month

- European Economic Climate Indicator: 100 is average for 2000–2020, reported in actual values

- Consumer Confidence Index: indexed with 1985=100

- Japan’s Leading Economic Index: indexed with 2015=100

- Japan’s Economy Watchers Sentiment Index: 50 is baseline

- Japan’s Corporate Goods Price Index: 0 is baseline

Important Economic Indicators and Political Events

8th

- Sixth Plenum of the Communist Party of China (through the 11th)

- 14:00 Japan September Leading Economic Index (CI) – preliminary

- 23:30 Clarida, Vice Chair of the Federal Reserve, panel discussion on inflation targets and monetary policy

- 24:30 Powell, Chair of the Federal Reserve, keynote speech at a meeting on gender and the economy

9th

- 08:50 Japan September International Balance of Payments and Current Account

- 14:00 Japan October Economy Watchers Survey

- 19:00 Euro Area November ZEW Economic Sentiment

- 22:00 U.S. October Wholesale Prices Index (PPI) month-on-month

- 23:00 Powell, speech at a meeting on gender and the economy (BOE, BOC, ECB participation planned)

10th

- 08:50 Japan October Money Stock M2 (YoY)

- 10:30 China October CPI (YoY)

- 10:30 China October PPI (YoY)

- 22:30 U.S. October CPI (MoM)

- 22:30 U.S. Previous Week’s Unemployment Claims

- 25:00 Russia Q3–Q4 GDP (Flash)

11th

- U.S. Holiday (Veterans Day)

- China's Singles’ Day, largest online shopping day

- 08:50 Japan October Domestic Corporate Goods Price Index

- 11:00 China October Industrial Production

- 16:00 UK Q3 GDP

- 19:00 ECB Economic Projections

- 28:00 Mexico Central Bank policy rate announcement

12th

- APEC Summit

- 19:00 Euro Zone September Industrial Production (MoM)

- 24:00 November University of Michigan Consumer Confidence (flash)

- 24:00 U.S. September JOLTS Job Openings

Next Week and Beyond

- December 14–15: FOMC (with Economic Projections)

- December 16: ECB

- December 16–17: Bank of Japan Monetary Policy Meeting

- January 17–21: Davos World Economic Forum

- January 18: Bank of Japan Monetary Policy Meeting (outlook for economy and prices)

- January 26: FOMC

- February 3: ECB

- March 10: ECB

- March 16: FOMC (with Economic Projections)

- March 18: Bank of Japan Monetary Policy Meeting

- April 14: ECB

- April 28: Bank of Japan Monetary Policy Meeting (outlook for economy and prices)

- May 4: FOMC

- June 9: ECB

- June 15: FOMC (with Economic Projections)

- June 17: Bank of Japan Monetary Policy Meeting

- July 21: Bank of Japan Monetary Policy Meeting (outlook for economy and prices)

- July 21: ECB

- July 27: FOMC

- September 8: ECB

- September 21: FOMC (with Economic Projections)

- September 22: Bank of Japan Monetary Policy Meeting

- October 27: ECB

- October 28: Bank of Japan Monetary Policy Meeting (outlook for economy and prices)

- November 2: FOMC

- December 14: FOMC (with Economic Projections)

- December 15: ECB

- December 20: Bank of Japan Monetary Policy Meeting

※ From here on (“Last Week's Currency Strengths/Weaknesses,” “Global Macro Environment Overview,” “Chart Analysis,” “This Week's Toda's Trading Strategy”) is a paid article

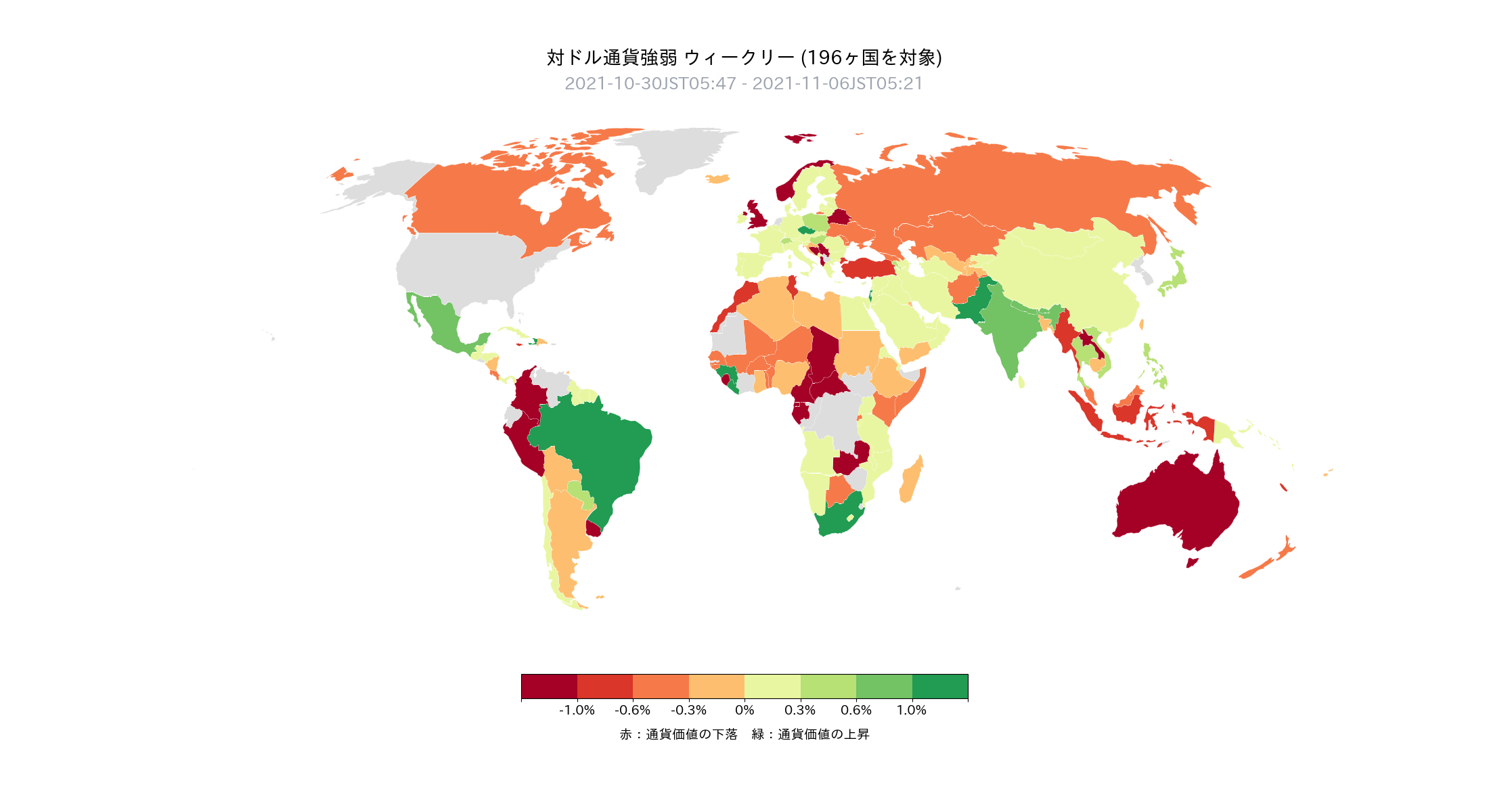

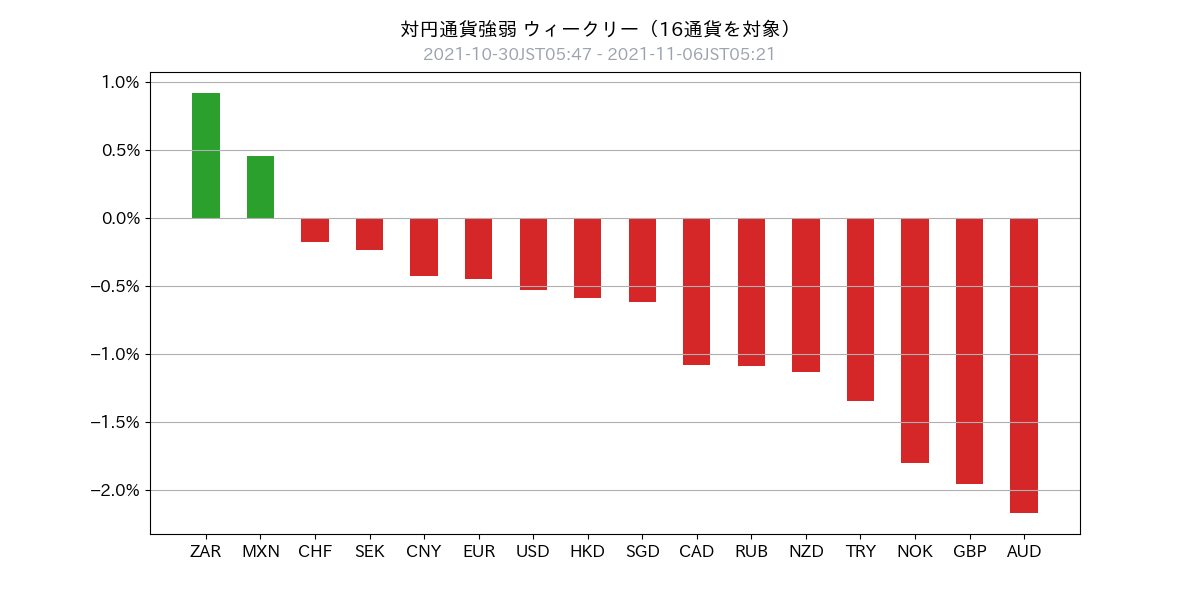

Last Week's Currency Strength

- Last week, the yen was bought while there was no standout movement in the dollar

- Emerging market currencies such as the Brazilian real, the Mexican peso, and the South African rand were also bought

- Australia and the UK were sold due to a more dovish central bank stance than market expectations

- With crude oil prices settling a bit, oil-producing countries like Norway and Russia also saw selling pressure

- In summary, currency strength/weakness as shown on the rightSouth Africa and some other emerging market currencies > Japanese yen > Chinese yuan > euro > US dollar > oil-producing currencies > pound of the UK & AUD which were more dovish than market expectations

Overview of the Global Macro Environment

- The major themes in the current market are 'disruptions in supply chains' and 'rising resource prices', which have fed global 'inflationary pressures' and resulting 'differences in monetary policy'.

- The Federal Reserve (US central bank) judges that it is unclear when supply constraints will ease

- The ECB believes supply constraints will ease over the course of next year

- Several developed-world central banks indicate thatthe rise in current inflation pressures is due not only to supply constraints but also to a rebound in demandas a major factor

- The Reserve Bank of Australia intends to delay easing as much as possible to avoid causing an economic slowdown. The background is relatively low inflation pressure

- The Bank of England signs that it will raise rates within months. The UK is among the earliest to raise among Five Eyes currencies

- The Fed announced the start of tapering (reduction of quantitative easing). It is anticipated to be completed by June next year

- Market participants' expectations for US policy rate hikes center on: first hike in July 2022 and second in December 2022(the outlook is somewhat delayed from last week)

- If you think simply, the currency that has been bought is likely to be the UK due to rate hikes, while Australia, which has delayed tapering or hikes, may be sold

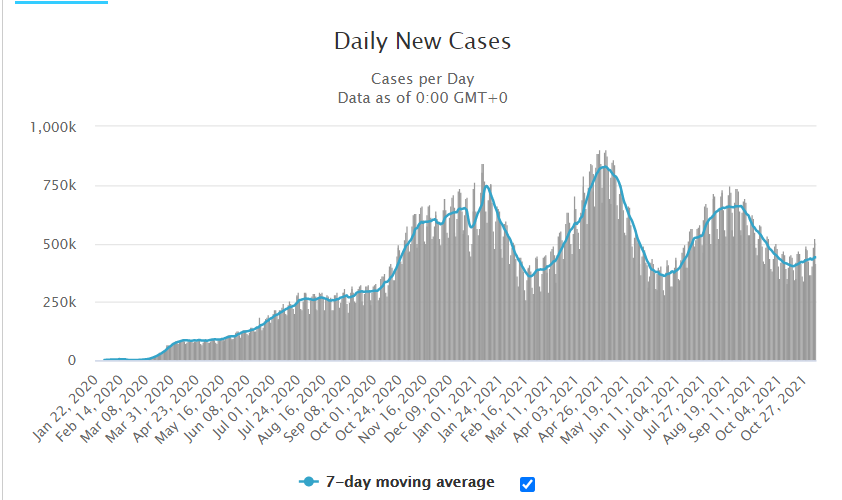

- The trend of new COVID-19 cases is stabilizing (the attached chart Daily New Cases below shows a seven-day moving average; it appears quite settled)

- In summary, the forex market will continue to move on differences in monetary policy (including market expectations), and equities are expected to remain firm on an economy recovering

COVID-19 New Cases, excerpt from Worldmeters

Chart Analysis

USD Index (Daily)

- Dollar Index is an indicator of overall dollar strength (Basket components: EUR 57.6%, JPY 13.6%, GBP 11.9%, CAD 9.1%, SEK 4.2%, CHF 3.6%)

- Although it surpassed the previous top of 94.50, it was bounced back at the resistance around 94.70

- To break above 94.70, a large dollar-buying catalyst may be needed

USD/JPY Mid-Term (Daily)

- Recently the range is judged to be 112.20–114.40

- Upside focus around 113.30–114.40

- Last week’s close was around 113.30; watching whether this level holds is important

USD/JPY Short-Term (Hour)

- If the downside continues to trend lower, watch for a sharp drop

- Downside targets are 113.00, 112.20

- Upside targets are 114.00, 114.40

EUR/USD Mid-Term (Daily)

- The downward trend is continuing

- Last week there was a scenario where the level of 1.1530 was broken

EUR/USD Short-Term (Hour)

- Selling on rally targets remains around 1.1580–1.1620, 1.1670

- We want to continue to target selling on rallies

USD/CNH Mid-Term (Daily)

- In a broad range, 6.35–6.60

- Narrow range 6.35–6.4250

- We continue to judge that a trend of dollar weakness and yuan appreciation persists

USD/CNH Short-Term (Hour)

- In the past month, no major moves; fluctuates around 6.3950 with about 200 pips range

This Week's Toda Trading Strategy

Overall Policy

- Last week, strong US economic indicators including October payrolls appeared, but as it’s weekend, dollar buying momentum weakened

- With the Bipartisan Infrastructure Bill (USD 550 billion) passed on the weekend, markets may react with higher US stocks at the start of the week

- Considering these, we judge that dollar buying is likely at the start of the week

- Mid-week to late week, we want to observe whether the dollar index can surpass the key level 94.70

- If it cannot be broken, we expect a range and will sell at the top and buy at the bottom

- Overall, forex remains in a consolidation phase; we will keep position sizes small and stay aligned

USD/JPY

- Last week’s close: 113.40

- View: sideways to upside

- Projected range: 112.20–114.40

- Current position: USD/JPY ±0

- Policy: dollar-buying bias at the start of the week.Because the BIB bill may have changed rate levels, we will reconsider entries if needed.

- Take profits around the 114 handle and monitor whether it can decisively break above 114.40

EUR/USD, EUR/JPY

- Last week’s close: EUR/USD 1.1566

- View: EUR/USD flat to down; EUR/JPY flat

- Projected range: EUR/USD 1.1400–1.1620

- Current positions: EUR/USD ±0, EUR/JPY ±0

- Policy: selling on rallies. We want to operate selling around 1.1580–1.1620.

- Profit target around 1.1530. Beyond that, we will trail with small lots

CNH/JPY, USD/CNH

- Last week’s close: USD/CNH 6.3925

- View: USD/CNH flat to down, CNH/JPY flat to up

- Projected range: USD/CNH 6.3600–6.4200

- Current positions: USD/CNH ± 0.0, CNH/JPY +4.0

- Policy: watch China's monetary easing stance and maintain yuan buying holdings.

Subscriber-Only Discord Invitation Code

Please apply from the URL below

Please align the registered name with your GogoJungle nickname

Important Notes

Unauthorized reproduction or copying of any contents published in this newsletter is prohibited. This newsletter is prepared solely for information provision, and its accuracy is not guaranteed by us or the information providers, and the contents may change due to changes in economic conditions. Use the published information at your own risk and consult professionals in law, accounting, tax, and related areas for individual matters. If a user suffers damages from using this information, our company and the information providers are not liable for any damages regardless of cause.