[November 01 to November 05] Trade strategies strongly oriented to bond markets and repatriation across countries

Last week's Foreign Exchange Range (Range of Movement)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 113.60 | 113.25 | 114.31 | 114.00 | +0.35% |

| EUR/USD | 1.1644 | 1.1535 | 1.1692 | 1.1561 | ▲0.71% |

| EUR/JPY | 132.33 | 131.57 | 132.94 | 131.80 | ▲0.40% |

| USD/CNH | 6.3808 | 6.3748 | 6.4104 | 6.4021 | +0.33% |

| CNH/JPY | 17.7999 | 17.7234 | 17.9157 | 17.7983 | ▲0.01% |

Last week's Currency Market Summary

USD/JPY

- Last week's USD/JPY movement started at 113.60 per dollar. Early in the week, solid dollar buying from real demand and strong U.S. housing data pushed it up to 114.31. However, after Tuesday, ahead of the Bank of Japan policy meeting on Thursday, profit-taking selling gradually dominated. At the policy meeting on Thursday, despite rumors of a tapering of pandemic relief, the session ended with no change, but the momentum of selling dollars and buying yen continued, reaching the week’s low of 113.25 in New York time. Later, supported by month-end dollar demand, USD/JPY rebounded and, heading into the London fix on Friday, dollar buying intensified, recovering to the 114 range and closing at 114.00.

EUR/USD

- The euro started at 1.1644 dollars per euro. Early in the week euro selling against the dollar dominated, pushing toward the 1.1600 level. Then, around 1.1600, option activity kept trading around that area for a while. Movement resumed on Thursday at the ECB press conference; when President Lagarde responded to a question about inflation by saying, “We talk about inflation, inflation, INFLATION,” markets shifted from anticipated early easing, German bond yields rose, and the euro was bought up to 1.1692. However, Friday was month-end, and with strong real-dollar demand, the euro reversed sharply, breaking below 1.1600 and sliding to 1.1535, closing at 1.1558 with volatile moves.

USD/CNH

- The yuan started at 6.3808 per dollar. Through Wednesday, movement was modest, but the People’s Bank of China’s accommodative stance became clear, and aggressive daily liquidity injections into short-term funding markets contributed to a gradual shift in favor of dollar-selling yuan buying. Friday, aided by month-end dollar demand, pushed briefly into the 6.41 area before closing at 6.4021.

What happened last week

※ Price indices and money statistics are year-on-year except where noted; GDP is quarter-on-quarter; and indicators without special notes are month-on-month or for the current month25th

- New Zealand holiday (Labor Day)

- Dallas Fed Manufacturing Activity Index +14.6

26th

- Japan September Corporate Services Price Index +0.9%

- U.S. September New Home Sales 800K (strong)

- U.S. October Consumer Confidence 113.8

- October Richmond Fed Manufacturing Index +12

27th

- Australia Q3 Consumer Price Index +3.0% (core +2.1%)

- U.S. September Durable Goods Orders −0.40%

- Bank of Canada holds policy rate at 0.25% and announces cessation of quantitative easing

- Brazil Central Bank raises policy rate by 1.5% to 7.75%

28th

- Bank of Japan keeps policy unchanged

- EU October Consumer Confidence −4.8

- ECB keeps monetary policy unchanged

- U.S. Q3 GDP +2.0% (annualized); reflects decline in personal consumption due to stimulus tapering

- U.S. Initial Jobless Claims 281K (robust)

- U.S. September Pending Home Sales −2.3%

- “Compromise and consensus are the only path to achieving great things in democracy.” Biden has proposed a framework to reduce the Build Back Better plan from $3.5 trillion over 10 years to $1.75 trillion, focusing on child care and climate measures, signaling an end to party infighting.(Build Back Better) framework announced. He moved to bring internal party divisions to an end over a period of months.

29th

- Japan September Unemployment Rate 2.8%

- Japan October Tokyo Metro Area CPI +0.1%

- Japan September Industrial Production −5.4%

- Japan September New Housing Starts +4.3% (YoY)

- Australia September Retail Sales +1.3%

- Australia Q3 Wholesale Price Index +2.9%

- Euro Area October Harmonized CPI +4.1% (high inflation pressure)

- Euro Area Q3 2023 GDP +2.2%

- Mexico Q3 GDP +1.5%

- Canada August GDP −0.1% (MoM)

- U.S. Q3 Employment Cost Index +1.3% (strong wage growth pressure)

- U.S. September Personal Consumption Expenditures (PCE) +4.4%

- Chicago PMI 68.4

- University of Michigan Oct Consumer Sentiment Final 71.7

- Russia September Unemployment 4.4%

- Colombia central bank raised policy rate by 0.5% to 2.5% for two consecutive meetings.

- Large protests in Sudan, Africa, opposing military power seizure after a coup.

- Oct 31: Lower house election voting progress

Economic Terms Glossary

- GDP = Gross Domestic Product; high growth is good

- CPI = Consumer Price Index: many advanced economies target 2%

- PCE = Personal Consumption Expenditures: personal spending; closely related to consumer prices

- PPI = Producer Price Index: influences CPI

- PMI = Purchasing Manager Index: 50 is the baseline

- ZEW = Leibniz Centre for European Economic Research: 0 is baseline

- NAHB = National Association of Home Builders: 50 is baseline

- NY Fed Manufacturing Index: 0 is baseline

- Philadelphia Fed Manufacturing Index: 0 is baseline

- Richmond Fed Manufacturing Index: 0 is baseline

- Chicago PMI: 50 is baseline

- University of Michigan Consumer Sentiment Index: indexed to 1966 = 100

- S&P/Case-Shiller Home Price Index: “20-C city” home price index is widely used; key for housing market trends

- Pending Home Sales Index: contracts signed but not yet closed

- European Consumer Confidence Index: base 100 for 2000–2020 average; released YoY

- European Economic Sentiment Index: base 100 for 2000–2020 average; released as actuals

- Consumer Confidence Index: base 100 for 1985

- Japan Leading Economic Index: base 100 for 2015

- Japan Economy Watchers Survey: 50 is baseline

- Japan Corporate Goods Price Index: base 0

Noteworthy Economic Indicators and Political Events

1st

- House of Representatives election results (31st)

- 10:45 China October Caixin Manufacturing PMI

- 12:00 U.S. October ISM Manufacturing Index

2nd

- 08:50 BOJ Policy Meeting Minutes

- 12:30 Reserve Bank of Australia policy rate announcement

- U.S. Virginia gubernatorial election (checking impact of Biden administration’s popularity)

3rd

- Japan Holiday (Culture Day)

- 10:45 China October Caixin Services PMI

- 19:00 Euro Area September Unemployment

- 21:15 U.S. October ADP Employment

- 23:00 U.S. October ISM Non-Manufacturing

- 23:00 U.S. September Durable Goods New Orders

- 27:00 FOMC

- 27:30 Powell press conference

4th

- Russia Holiday (Unity Day)

- 19:00 Euro Area September Producer Prices

- 21:00 Bank of England rate decision

- 21:30 U.S. September Balance of Trade

- OPEC+ Ministers' meeting

5th

- 19:00 Euro Area September Retail Trade

- 21:30 U.S. October Employment

- 21:30 Canada October Employment

Beyond next week

- Dec 14–15: FOMC (with economic projections)

- Dec 16: ECB

- Dec 16–17: BoJ Policy Meeting

- Jan 17–21: Davos World Economic Forum

- Jan 18: BoJ Policy Meeting (with outlook on economy and price)

- Jan 26: FOMC

- Feb 3: ECB

- Mar 10: ECB

- Mar 16: FOMC (with projections)

- Mar 18: BoJ Policy Meeting

- Apr 14: ECB

- Apr 28: BoJ Policy Meeting (outlook on economy and prices)

- May 4: FOMC

- Jun 9: ECB

- Jun 15: FOMC (with projections)

- Jun 17: BoJ Policy Meeting

- Jul 21: BoJ Policy Meeting (outlook on economy and prices)

- Jul 21: ECB

- Jul 27: FOMC

- Sep 8: ECB

- Sep 21: FOMC (with projections)

- Sep 22: BoJ Policy Meeting

- Oct 27: ECB

- Oct 28: BoJ Policy Meeting (outlook on economy and prices)

- Nov 2: FOMC

- Dec 14: FOMC (with projections)

- Dec 15: ECB

- Dec 20: BoJ Policy Meeting

※ From here on (“Last week’s currency strength/weakness,” “Global macro environment overview,” “Chart analysis,” “This week’s Toda’s trading strategy”) are paid articles

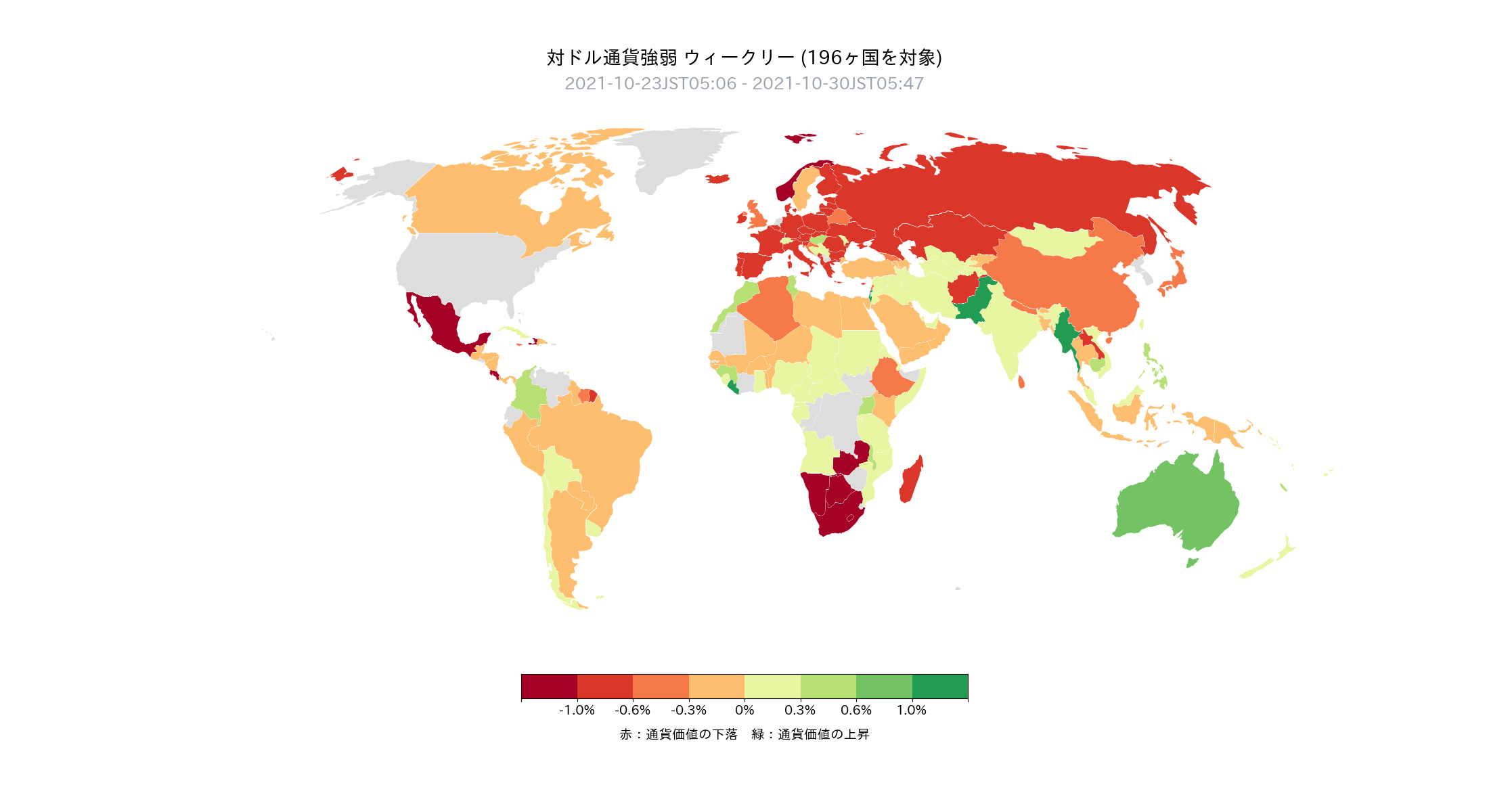

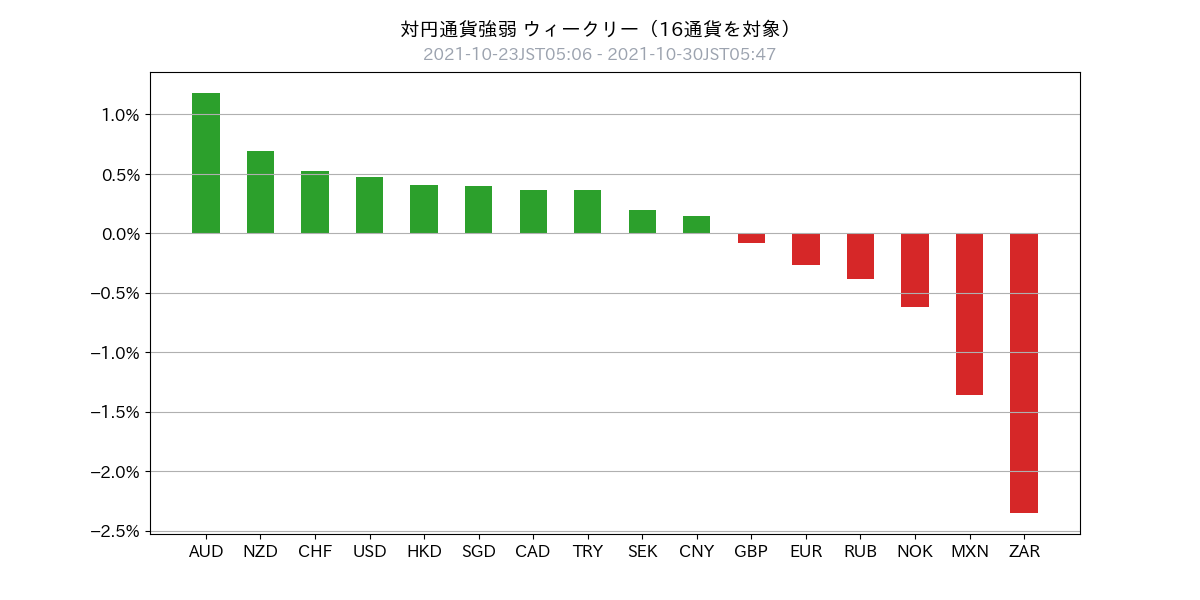

※ Visualizes currency gains and losses to help infer the current "theme of the market"

- Last week, the dollar strengthened (111/196 countries)

- Emerging market currencies such as the South African rand and the Mexican peso softened

- Australia was bought due to a higher likelihood of earlier rate hikes

- In summary, currency strength/weakness is as followsOOA currency > US Dollar > Japanese Yen > Euro > Emerging market currencies (South Africa, Mexico, etc.)

Global macro environment整理

- The main themes in the current market are "supply chain disruptions" and "high resource prices," which have led to globally rising inflationary pressures and, as a result, differences in monetary policy.

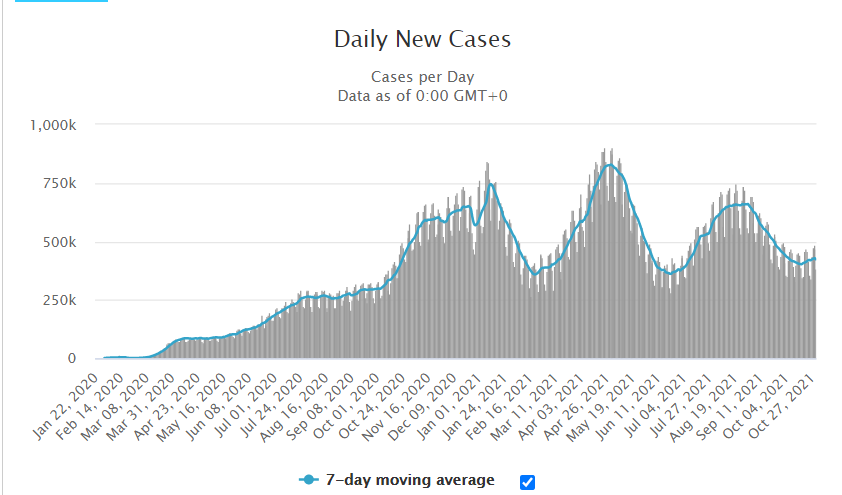

- In financial markets, the increase in new coronavirus cases has moved out of focus (especially in advanced economies),as we are moving toward a post-pandemic outlook, it seems.

- Under these circumstances, Australia’s interest rates surged last week, supported by a strong economy, so the Australian dollar was bought.

- The reasons include rising inflationary pressures, a record-high trade surplus due to soaring commodity prices, and expectations for earlier monetary tightening.

- The U.S. economy is also very strong, but the question is how that compares, which is the mood of the FX market.

- The trend of daily new COVID-19 cases has slightly turned up (the attached chart Daily New Cases shows a recent uptick on a 7-day moving average)

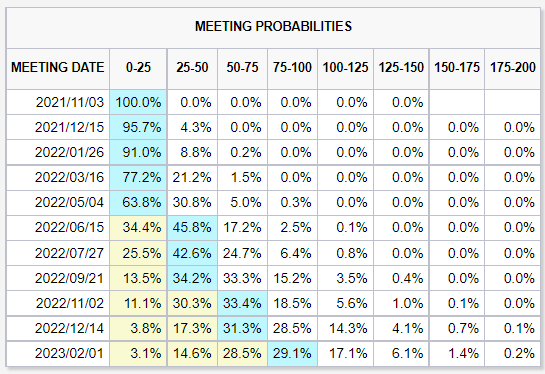

- Investors’ expectations for U.S. monetary policy became more forward-looking: tapering was priced in by the Nov 2021 FOMC, and rate hikes by the June 2022 FOMC, which is even more anticipated than the previous week (and priced in even further ahead than before).

Chart Analysis

USD Index (daily)

- Dollar Index is a broad measure of the dollar’s strength (basket composition: EUR57.6%, JPY13.6%, GBP11.9%, CAD9.1%, SEK 4.2%, CHF 3.6%)

- Rebounded on the weekend due to month-end dollar buying

- With expectations for rate hikes pulled forward, watch whether it can break above the previous top of 94.50 and the resistance of 94.70

USD/JPY Medium-term (daily)

- Recent range estimated at 112.20–114.40

- Upside potential roughly 113.30–114.40

- Momentum appears to be fading and the pace is somewhat heavy

USD/JPY Short-term (hourly)

- Rebound from around 113.30

- Watch whether it can break above 114.40, 114.70 (year-to-date high)

- If the downside accelerates, be cautious of a sharp drop

EUR/USD Medium-term (daily)

- Range of 1.1530–1.1670 remains in effect

- If 1.1530 is broken to the downside, the lower target is hard to identifyso it’s better to judge by price action and RSI

EUR/USD Short-term (hourly)

- Sell-on-rise level around 1.1580–1.1620

USD/CNH Medium-term (daily)

- In a wide range of 6.35–6.60

- China’s policymakers are clearly easing, and 6.35 has moved away slightly

USD/CNH Short-term (hourly)

- Narrow range 6.3700–6.4250

- Watching authorities’ moves; around 6.4250, consider selling on rallies

This Week’s Todai Trade Strategy

Overall Policy

- As the U.S. economy remains strong with inflation pressures, anticipate earlier rate hikes,prioritize dollar buying (macro stance)

- Assuming prolonged Japanese monetary easing,sell the yen first. However, as U.S. interest rates rise, flows into emerging market currencies and yen buying will be considered, so we plan to take a dip-buying approach this week. (waiting for a pullback)

- China’s policymakers are clearly easing,the yuan should be bought only on pullbacks. In any case, we want to follow policymakers’ stance.

- The euro hasexperienced a major chart breakdown, so we willlead with selling (buying dollars).

- Only,we want to ride the rally more with AUD than other currencies

- Currency momentum is judged as followsAUD > USD > CNY > EUR > JPY (though we also anticipate selling emerging market currencies, buying euros, and buying yen, so chasing highs is deemed risky)

USD/JPY

- Last Friday's close: 114.00

- Outlook: sideways to higher

- Estimated range: 113.00–114.70

- Current position: USD/JPY flat

- Policy: buy on dips. Be bold below 113. If it breaks 114.70, ride it higher.

EUR/USD, EUR/JPY

- Last Friday's close: EUR/USD 1.1561

- Outlook: EUR/USD flat to lower; EUR/JPY flat

- Range expected: EUR/USD 1.1400–1.1670

- Current position: EUR/USD flat; EUR/JPY flat

- Policy: sell on rallies. In the 1.1580–1.1620 zone, prefer selling strategies. If 1.1530 breaks lower, follow lower.

CNH/JPY, USD/CNH

- Last Friday's close: USD/CNH 6.4021

- Outlook: USD/CNH flat to lower, CNH/JPY higher

- Range: USD/CNH 6.2500–6.4000

- Current position: USD/CNH ±0.0 CNH/JPY ±0

- Policy: monitor China’s easing stance while buying on pullbacks

AUD/USD, AUD/JPY

- Last Friday's close: AUD/USD 0.7523

- Outlook: AUD/USD higher, AUD/JPY higher

- Range: AUD/USD 0.7460–0.7600

- Current position: AUD/USD +3.0, AUD/JPY +3.0

- Policy: hold long positions

Subscriber-only Discord invitation code

Please apply from the URL below

※ Please align the registered name with your GogoJungle nickname

Important Notices

Unauthorized reproduction or copying of any content in this newsletter is prohibited. This newsletter is prepared solely for informational purposes, and its accuracy is not guaranteed by our company or the information providers. Also, the contents may change due to changes in economic conditions. Use the information at your own risk and consult professionals in law, accounting, tax, etc. If a user suffers damages from using this information, our company and the information providers will not be liable for damages regardless of the cause.