[September 13 – September 17] Trading strategies mindful of each country's economic indicators and expected ranges

Last Week's Exchange Rate Range (Fluctuation Range)

| Open | Low | High | Close | Change | |

|---|---|---|---|---|---|

| USD/JPY | 109.75 | 109.62 | 110.45 | 109.93 | +0.16% |

| EUR/USD | 1.1879 | 1.1802 | 1.1887 | 1.1814 | ▲0.55% |

| EUR/JPY | 130.41 | 129.66 | 130.71 | 129.87 | ▲0.41% |

| USD/CNH | 6.4362 | 6.4237 | 6.4649 | 6.4430 | +0.11% |

| CNH/JPY | 17.0511 | 16.9921 | 17.1052 | 17.0540 | +0.02% |

Last Week's Foreign Exchange Market Summary

USD/JPY

- Last week's USD/JPY started at 109.75 per dollar. The week began with little movement, but as Japanese stocks rose solidly, yen selling gradually gained the upper hand. On Tuesday it broke through 110, and on Wednesday briefly reached a high of 110.45. The trend looked to continue rising, but selling orders thickened, and the pair gradually fell. On Thursday it again dipped below 110, briefly to 109.62. By the end of the week, it recovered to close at 109.94.

EUR/USD

- The euro started at 1.1879. With an ECB meeting looming, the euro continued to weaken from the start of the week. On Wednesday it temporarily dropped to 1.1802, testing the 1.18 level, but large option positions and buy orders supported the early part of 1.18 ahead of the ECB meeting. At the ECB meeting, it was announced that PEPP bond purchases would be reduced, but inflation outlook remained soft, leading to mixed market reactions. The euro then saw some rebound, but with heavy option activity near 1.1850 and lackluster upside, it closed around 1.1815.

USD/CNH

- The yuan started at 6.4362 per dollar. Dollar buying dominated early in the week, pushing to an intr week high of 6.4649 on Tuesday. Thereafter it traded around 6.46 with small moves, but as in the previous week, dollar selling intensified on Friday afternoon in North American hours, briefly hitting a low of 6.4237. It then rebounded to close at 6.4430.

What Happened Last Week

Note: Price indices and money statistics are year-on-year comparisons; GDP is quarter-on-quarter; indicators without special notes are month-on-month or current month values.6th

- U.S. holiday (Labor Day)

7th

- China August trade balance +58.34 billion USD (strong)

- Japan August foreign exchange reserves +1,424.3 billion USD (increase)

- Reserve Bank of Australia announced extension of quantitative easing (A$40 billion weekly bond purchases) from mid-November 2021 to mid-February 2022

- Japan July coincident index 94.5, leading 104.1, lagging 93.8

- Europe September ZEW sentiment index 31.1 (not bad)

- Europe Q2 2020 GDP, YoY +14.3%

- U.S. Secretary Blinken and Defense Secretary Austin met Qatar’s Deputy PM and Foreign Minister on July 7 during a visit to Doha. Qatar acted as mediator for indirect talks with the Taliban and Afghanistan.

8th

- Japan Q2 GDP (revision) YoY +1.9%

- Japan July current account +¥19.108 trillion

- Japan August Economic Watchers Survey: Current 34.7, Outlook 43.7

- U.S. MBA mortgage applications (week over week) ▲1.9%

- Bank of Canada kept policy unchanged at its rate decision meeting

- U.S. July JOLTS job openings 10.934 million

- Fed Beige Book: From early July to August, economic activity overall slightly declined; travel and dining worsened.

- U.S. July consumer credit +$17.0 billion

- U.S. Treasury Secretary Yellen urged Congress again to raise the debt limit in August. Temporary measures to suspend some cash on hand and public employee pension funds were projected to run out by October, warning that the U.S. could become unable to meet its debt obligations.

- Federal Reserve Bank of San Francisco President Williams said in a speech that if the economy continues to improve as expected, starting to taper asset purchases by year-end would be appropriate, aligning with Chair Powell's views.

9th

- North Korea's National Foundation Day

- Japan August M2 money stock +4.7% (growth pace slowing)

- China August CPI +0.8%; PPI +9.5% (high)

- ECB announced adjustments (tapering) of PEPP purchases

- Previous week's initial jobless claims 310,000

- China Evergrande Group's USD bonds of over 200 billion yuan shook global markets; concerns over solvency due to reckless investments. Government intervention unclear; investors selling.

10th

- Bank of Russia policy rate raised 0.25 to 6.75%

- U.S. August PPI +8.3% (high)

- U.S. July wholesale inventories +0.6%

- U.S. July wholesale sales +2.0%

- Gazprom completed laying Nord Stream 2 to supply gas to Europe via the Baltic; operation planned by end of 2021

- Xi Jinping and Joe Biden held a phone call after seven months; agreed to work toward easing tensions

- People's Bank of China and others officially announced opening of inter-market investment between mainland, Hong Kong, and Macau from October; scale about 300 billion yuan (roughly 5 trillion yen). Aims to attract foreign financial institutions with mainland investment capital.

Glossary of Economic Terms

- GDP = Gross Domestic Product; high growth is positive

- CPI = Consumer Price Index; many advanced economies target 2%

- PCE = Personal Consumption Expenditures; closely correlated with consumer prices

- PPI = Producer Price Index; influences CPI

- PMI = Purchasing Manager Index; 50 is the baseline

- ZEW = Leibniz Centre for European Economic Research; 0 is baseline

- NAHB = National Association of Home Builders; 50 is baseline

- New York Fed manufacturing index; 0 is baseline

- Philadelphia Fed manufacturing index; 0 is baseline

- Richmond Fed manufacturing index; 0 is baseline

- Chicago Purchasing Managers Index; 50 is baseline

- University of Michigan Consumer Sentiment Index: 1966=100

- S&P/ Case-Shiller Home Price Index: 20-city index commonly used to gauge housing market trends

- Housing Permit Index: number of contracts signed but not yet closed

- Euro area Consumer Confidence Index: index with 2000-2020 average set at 100; releases are month-on-month

- Euro Area Economic Sentiment Index: index with 2000-2020 average set at 100; releases are actual values

- Consumer Confidence Index: indexed to 1985=100

- Japan Leading Index: indexed to 2015=100

- Japan Outlook/Watcher's Survey: 50 is baseline

Notable Economic Indicators and Political Events

13th

- IAEA Board of Directors (Vienna until 17th)

- 08:50 Japan Q3 2020 quarterly Corporate Goods Price Index

- 08:50 Japan August Domestic Corporate Goods Prices

- 27:00 U.S. August Monthly Civic Budget

14th

- United Nations General Assembly (online) opens

- 13:30 Japan July Industrial Production

- 13:30 Japan July Capacity Utilization

- 21:30 U.S. August Consumer Price Index

15th

- Von der Leyen delivers annual Policy Speech

- 08:50 Japan July Machinery Orders

- 11:00 China August Retail Sales

- 11:00 China August Industrial Production

- 13:30 Japan July Services Activity Index

- 18:00 Europe July Industrial Production

- 20:00 U.S. MBA Mortgage Applications Index

- 21:30 September New York Fed Manufacturing Index

- 21:30 U.S. August Import Prices

- 22:15 U.S. August Industrial Production

- 22:15 U.S. August Capacity Utilization

16th

- SCO summit (Shanghai Cooperation Organization) until 17th

- 08:50 Japan August Trade Statistics

- 08:50 Japan Previous Week's T&I data

- 18:00 Europe July Trade Balance

- 21:30 U.S. August Retail Sales

- 21:30 U.S. September Philadelphia Fed Manufacturing Index

- 21:30 U.S. Previous Week's Initial Jobless Claims

- 23:00 U.S. July Corporate Inventories

- 29:00 U.S. July Net Foreign Securities Investments

17th

- BOJ Funds Circulation Statistics for Q1–Q2

- 17:00 Europe July Current Account

- 18:00 Europe July Construction Expenditure

- 18:00 Europe August Consumer Price Index

- 23:00 U.S. September University of Michigan Consumer Confidence

Next Week and Beyond

- Sept 21–22: BOJ Monetary Policy Meeting

- Sept 21–22: FOMC

- Sept 21–27: United Nations General Debate

- Sept 26: German Federal Elections

- Sept 29: Liberal Democratic Party Leadership Election

- Oct 27–28: BOJ Monetary Policy Meeting

- Oct 28: ECB

- Oct 30–31: G20 Summit

- Nov 2–3: FOMC

- Dec 14–15: FOMC

- Dec 16: ECB

- Dec 16–17: BOJ Monetary Policy Meeting

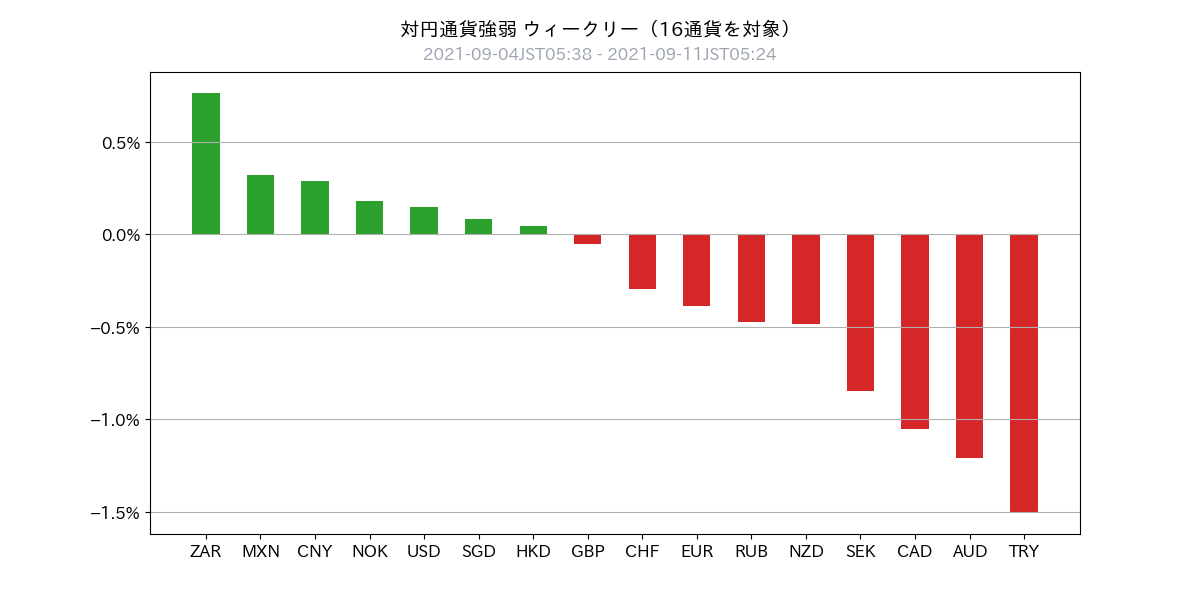

Last week's USD and JPY currency strength

- The yen showed a soft trend

- While Turkey was sold, South Africa was bought, indicating clear relative strength by currency

- The yuan remains stable

- Ruble rose due to rate hikes but faced some selling

- In summary, currency strength is as followsStrong emerging-market currencies > yuan > dollar > yen > euro > Oceania > weak emerging-market currencies

整理 Global Macro Environment

- Globally, producer prices remain high, potentially squeezing corporate profits and putting downward pressure on equities.(Equity market risk factor)

- Attention to China’s real estate heavyweight Evergrande’s default and overall China’s economic slowdown is still needed.(Renminbi weakness factor)

- Attention on the Liberal Democratic Party leadership race. Basicallyyen weakness and stock price increases are expected factorsto consider.

- Whether a risk-on environment becomes the mainstream is under watch.Key factors are the lengthening of U.S. monetary easing and signs of COVID-19 recovery。

- COVID-19 resurgence has entered a pause for now(Daily New Cases chart attached below shows a range from flat to slight decline with a 7-day moving average)

- Investors’ outlook for U.S. monetary policy expects tapering decision within the year and rate hikes to start in November 2022, which is the consensus.(This schedule has largely stabilized)

- U.S. equities tend to underperform from August to October historically (seasonality).

COVID-19 new infections, excerpt from Worldometers

FOMC rate hike expectations from market participants, excerpt from CME Group

Chart Analysis

USD Index (Daily)

- Dollar strength does not persist

- Tapering timing and rate-hike timing are broadly set, so dollar-driven fluctuations may remain limited for a while

USD/JPY Medium-term (Daily)

- Wide range: 107.50–111.65

- Core range: 109.00–111.00

- Expect a market with unclear directional bias

USD/JPY Short-term (Intraday)

- Day-trading range: 109.40–110.40

- Upside pressure slightly stronger

EUR/USD Medium-term (Daily)

- Wide range: 1.1630–1.2250

- Continuing to move near the lower end of the range

EUR/USD Short-term (Intraday)

- Day-trading range: 1.1800–1.1900

- Buying near 1.1800 is a viable strategy

USD/CNH Medium-term (Daily)

- Range judged: 6.35–6.60

- Recently a trend of dollar weakness and yuan strength continues

USD/CNH Short-term (Intraday)

- Day-trading range: 6.4200–6.5200

- If it dips below 6.42, 6.36 comes into view

- The decline from Friday afternoon to late night may continue, to test in day-trades(Possible regular flows from Europe and the U.S.)

This Week’s Toda’s Trading Strategy

Overall policy

- Keep a close watch on Chinese and Japanese stock markets to detect risk-off signals early

- Be aware that the Covid-19 new infection curve is slowing its rise(Be mindful of continued risk-on)

- Gradually, investors may return, increasing clarity of direction(Assess whether risk-on or profit-taking leads)

- The U.S. dollar is weak as the August 2021 payrolls data lowered expectations for further rate hikes, suggesting possible dollar weakness continues(Possibility of continued dollar weakness)

- With Abe/ Suga not running in the leadership race causing political instability and monetary easing likely to persist, selling the yen is expected to lead(lead).

- Keep in mind domestic economy slowdown from U.S.–China confrontations and power struggles; continue to hold yuan, and adjust positions as necessary

- Euro shows signs of revival in economic indicators; consider buying in advance

USD/JPY

- Last Friday’s close: 109.93

- View: range-bound to upside

- Assumed range: 109.40-111.40

- Current position: USD/JPY about flat

- Policy: In the short term, avoid strong market bias; buy near 109.40 and sell near 111.40

EUR/USD, EUR/JPY

- Last Friday’s close: EUR/USD 1.1814

- Assumed range: EUR/USD 1.1800–1.1900

- View: EUR/USD flat to up; EUR/JPY flat to up

- Current positions: EUR/USD ±0, EUR/JPY ±0

- Policy: Focus on EUR/USD, buy around 1.1800 and sell around 1.1900

CNH/JPY, USD/CNH

- Last Friday’s close: USD/CNH 6.4430

- Assumed range: USD/CNH 6.4200–6.5200

- View: USD/CNH flat-to-down, CNH/JPY flat-to-up

- Current positions: USD/CNH ± 0.0, CNH/JPY +3.0

- Policy: Hold CNH/JPY long (mid-to-long term); sell USD/CNH on Friday afternoon and buy back late Friday night (day trade).

- Be wary of the impact of worsening Chinese economy and Evergrande’s default on the market

Subscriber-only Discord invitation code

Please apply using the URL below

Note: Please use your GogoJungle nickname for registration

× ![]()