Sandwich Manse Market Topic Lecture|Part7. Inflation

Mr. Sandwich Masao introduces topics of interest in the current market. This time, about “inflation.” We will provide a concise and easy-to-understand explanation from basic concepts to inflation currently perceived in the U.S. economy. Note: The content of this article is based on the author’s views and does not guarantee future profits.

Link to the previous article

→Sandwich Masao's Market Topic Lecture|Part6. Interest Rates

In Japan, which has not been able to escape deflation, inflation is now progressing in the United States, where the situation is different.

Generally, “gentle inflation” is considered desirable, but what is the current situation in the United States?

Let’s organize from the point of why we aim for gentle inflation.

1. Why aim for gentle inflation

Inflation refers to a situation where prices continue to rise. Many people may think, “Prices should be as low as possible!”, but this mindset is precisely the “deflation mindset” that has spread in Japan.

■ What deflation is expected to cause

For consumers, falling prices may seem welcome, but how about for companies?

When prices drop, to maintain traditional sales levels, companies are compelled to sell more in quantity. While lower prices alongside higher sales volumes might work, consumer demand does not explode, so price declines can pressure sales.

If sales fall, companies will likely pursue cost-cutting reforms to protect profits, and one of the costs involved is, of course, wages. Layoffs are extreme, but at least when sales do not rise, the salaries of employees become harder to increase.

If wage growth stalls, consumer spending declines, and more goods go unsold. If goods aren’t selling, business becomes tougher, leading to further wage cuts… a negative spiral continues.

This negative chain is called a “deflationary spiral.”

After Japan’s bubble burst, this situation led to the “Lost Decade” of economic stagnation. To avoid falling into the deflationary spiral, many advanced economies pursue monetary policies aimed at “gentle inflation.”

Japan, still affected by the pandemic, continues to struggle with low inflation, but the United States seems to be in a very different scenario.

2. Is current U.S. inflation temporary?

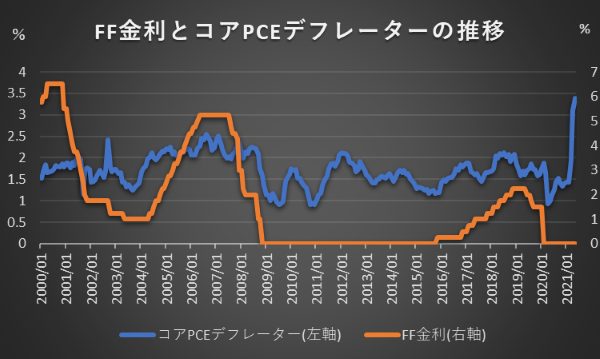

As of July 2021, the Federal Reserve Board (FRB) aims for an inflation rate that remains above the long-term average of 2%, and the key indicator watched is the “core PCE deflator,” a price index.

Source: Prepared by the author from Bloomberg data

Looking at the core PCE deflator, inflation exceeded 3% year-over-year in both April and May 2021, and on a spot basis inflation is running above the FRB’s target. This has brought attention to the next moves, such as tapering of asset purchases and potential rate hikes.

In the previous hiking cycle since 2015, the rate hikes were announced as “preventive,” acting before prices rose. This time, inflation is triggering the moves first.

However, the FRB seems to view this inflation as “temporary.”

■ Drivers of inflation

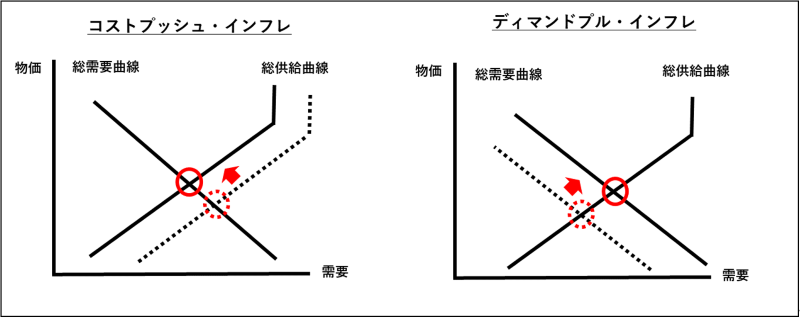

Inflation can be broken down into supply-side and demand-side factors.

The image below shows “cost-push inflation” as a supply-side inflation. Applying this to the current United States, following the post-pandemic reopening, there may be cases where raw material procurement cannot keep up for manufacturing, causing production costs to rise and the overall supply curve to shift left while prices rise.

The other factor, “demand-pull inflation,” is a demand-side inflation. In the United States today, expansive fiscal policy and easy money increase consumers’ purchasing power, and as economic activity resumes and consumption increases, the overall demand curve shifts right, causing prices to rise.

Source: Created by the author

The recent rapid rise in inflation can be seen as the combined effect of cost-push and demand-pull inflation, though it is also true that this reflects a temporary factor following the extraordinary crisis of the pandemic.

Cost-push inflation may ease as supply constraints relax, and demand-pull inflation may be viewed as a reaction after economic activity resumes. Still, markets feel a sense of crisis about the recent rapid inflation, and FRB members’ statements on inflation will continue to attract attention.

※This article reflects the author’s views and does not provide definitive investment judgments. It is for information purposes only and does not solicit the buying or selling of any type of product.

First-class Financial Planning Practitioner. Worked in bank financial product sales, then joined Invast Securities as a currency dealer. Currently in the Marketing Department, working to spread the enjoyment of investing to the world. It is well known on the street that “they answer questions about finance immediately,” and the author aims to become a trusted, elder-brother type. Also, a Sandwich enthusiast to the point colleagues are often surprised. Always handling tasks with a sandwich in hand. Furthermore, every night before bed, he makes the next day’s sandwich himself, a romantic side believed to be his charm point.