10 Steps to Make FX with the Crab Trader Method Your Income Pillar | Step 1: Always Record Your Trading P&L

Kani Trader's Profile

Kani Trader. Started YouTube Live on January 15, 2018. Streams all 12 hours—from noon to late night—of his own trades in real time. With the themes “Make money, right in front of you” and “Make money, right in front of you,” every day he公開s all entry orders, stop orders, and entries.

Twitter:https://twitter.com/keibakinma

*This article is a reprint/edit of an article from FX攻略.com June 2019 issue. Please note that the market information written in the main text may differ from the current market.

Don’t Repeat the Same Mistakes

There are many things you need to do to succeed in FX, such as studying the basics of the currency market, learning how to use MT4, and practicing technical analysis.

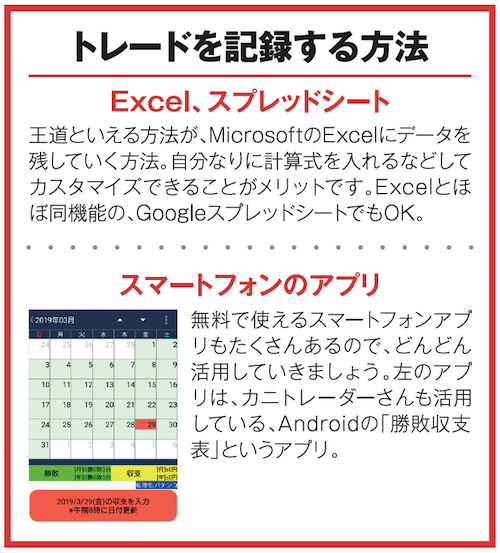

But for people starting FX now, there is one thing I want you to tackle first. It is “keeping a trading log.” To be frank, among people who continuously achieve results in FX, none do not keep records of their profits and losses. More precisely, if you don’t track your P/L, you won’t know whether you are winning or losing.

Why keep a log? It is to review daily trades. If you don’t record a day's trade, memories fade and you will eventually forget it.

And by reviewing finished trades, you won’t repeat the same mistakes. By not repeating a past mistake, your trading method will be continually polished, and your P/L will improve.

Most people probably feel more stressed about recording losses than profits. But to prevent repeating failures, losses should be recorded in detail.

In that sense, when keeping a trading log, be sure to write down not only P/L, currency pair, and trade time, but also the reasons you won or lost. Simply saying “I won” or “I lost” will make a completed trade a one-off result. I personally review and record that day’s trades every night before sleep.