Is GASOLINE price hike funded by public money? The reason for 190 yen even though crude oil hasn't arrived yet

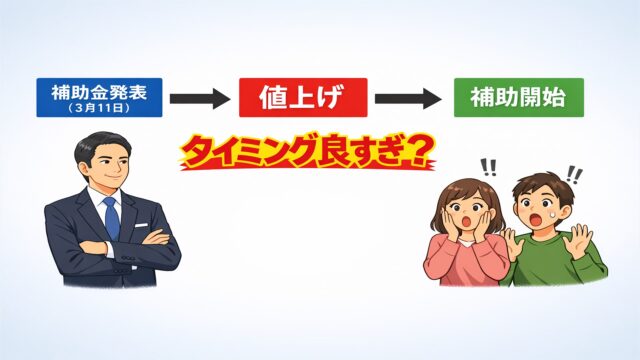

“Was the gasoline price increase a case of public funds being siphoned off?” The recent fluctuation in gas prices, which many people are questioning, is accompanied by several unnatural points. First, the timing of the price hike.Right around the time of the subsidy restart announcement, the major refiners announced a wholesale price increase, and retail prices jumped into the 190 yen range at once.

However, starting around March 19, when the subsidies began, prices subsequently fell sharply in a short period. This pattern of “rise and then fall” cannot be explained by simple cost pass-through.What’s most decisive is that Middle Eastern crude oil has not yet arrived in Japan.In addition, this subsidy is designed to “cover the portion exceeding 170 yen,” so subsidies are unnecessary if the price does not exceed 170 yen. What do you think about this mechanism?

The unnatural rise, its link to subsidies, and delays in crude oil procurement—these three factors together feel off. This article will organize the true nature of this discomfort from the perspectives of timing and structure.

?Crude oil procurement and price do not add up

Crude oil is loaded in oil-producing countries, transported by tanker, refined after arrival in Japan, and finally sold as gasoline. This whole process typically involves a lag of several weeks. Therefore, if the retail price spikes in mid-March, it is natural to think it reflects prices for crude oil that could be purchased in the future, not the cost of crude oil already procured.

This does not align with an explanation of price increases. Considering geopolitical risks such as tensions in the Strait of Hormuz, one could say, in a extreme expression, that “crude oil traded at high prices has not yet entered Japan even a drop.” From this situation, it follows thatprices are formed not by actual costs but by expectations or risk premiums.

Movements to preempt future supply concerns and price rise risks are rational from a market perspective, but they follow a different logic from “surging procurement costs,” and this mismatch is the root of the unease.

?The timing of the price increase is too convenient

As of March 16, the national average was 190.80 yen, up about 30 yen from the previous week. To organize this rapid rise: on the night of March 11, subsidies were restarted; immediately after, from the 12th onward, the major refiners (like ENEOS) raised wholesale prices by about 26 yen, and retail prices surged. Then, with the subsidy starting on March 19, prices began to fall.

This sequence does not reflect a typical causal chain of “cost increases leading to hikes,” but rather a pattern of “policy decision → price increase → subsidy adjustment.”As a result, because it started well above the subsidy threshold of 170 yen, the greater the excess portion, the larger the subsidy amount becomes.

On social media, questions such as “Why raise prices when the tankers haven’t even arrived yet?” spread, and experts describe it as a “preemptive price rise factoring in supply concerns.” While attributing malice is difficult, it is natural for consumers to feel that prices are being advanced too much. This alignment of timing fosters mistrust about the relationship between the system and prices.

?The speed of price reductions is too fast

After subsidies began, retail prices fell sharply within days. Normally, prices are constrained by stock and procurement costs and adjust gradually. In goods like gasoline, existing stock prices are reflected, so rapid price cuts are unlikely. Yet in this case,a nearly 20 yen drop was observed soon after subsidies began, with some stores reflecting it the same day.

This movement suggests that part of the price was not fixed costs but adjustable margins or expected amounts. In other words, the risk premium embedded at the time of the hike may have been peeled away at the same moment subsidies began.This further supports the possibility that not all of the price increase reflected real costs, raising questions about price formation transparency.

?The subsidy design distorts incentives

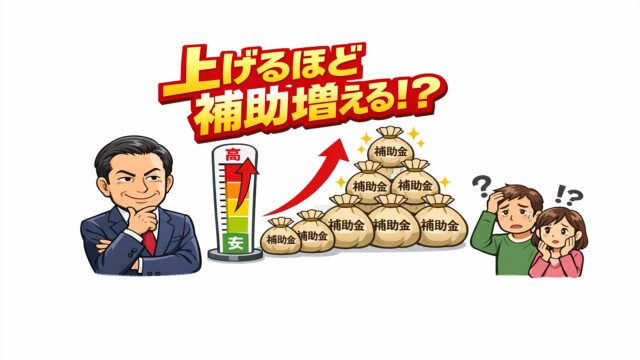

The current subsidy system is a variable scheme that covers the portion exceeding 170 yen for refiners. Analyzing this, it seems to raise prices in anticipation of future risks, the excess portion is subsidized, and as a result retail prices fall.

The problem is that subsidies can apply to prices already increased beforehand.In terms of design, this is simple, but it creates room for incentives to push prices up in advance. How about this as a comparison?If subsidies were proportional to the actual increase in procurement costs,they would cover only truly increased costs, and reduce unnecessary subsidies or pre-emptive actions.

On the other hand, the current system ignores differences in self-service vs full service, urban vs rural, and inventory turnover, making price distortion easier. The government prioritized speed and clarity, but as a result regional and store differences have widened, and questions about the system’s fairness have grown. Past subsidy schemes have also been criticized for insufficient reflection in retail, andwe must also acknowledge that complete monitoring has its limits.

?Mismatch with pre-release stock releases

The government releases private stock for 15 days and national stock to mitigate supply concerns and stabilize prices. Theoretically, if supply is secured, prices should stabilize, yet high prices persist. By the way, stockpiling involves an obligation to maintain 70 days of reserves by the oil majors, but this can be reduced to 55 days.In other words, simply reducing inventory does not bring about major operational changes.

Additionally, the national stockpile announced that it would trade at prices one month prior, so this is not a case of elevated prices due to real demand. This phenomenon shows that prices are determined by expectations and risks rather than actual demand, meaning that “future expectations” strongly influence prices more than physical supply.

In such circumstances, the effect of stock releases tends to be limited, creating a misalignment between policy and the market. Supply exists, yet high prices are hard for consumers to understand, fueling distrust.

?Is this a case of “public money sucking”?

The key points are clear: - The time axis of procurement and price does not align - Price increases are linked to subsidy decisions - Price declines occur simultaneously with subsidy starts. Considering these, the main cause of hikes can be seen as risk avoidance/anticipation (risk premium), not procurement costs.

In the ENEOS wholesale price increase of about 26 yen, pre-notice caused panic fueling and stockouts,and on social media, voices asking if this was opportunistic rose.Subsidies increase as the excess portion grows, so it is natural that doubts arise about the relationship between the system and prices.

The rationality of corporate activity is understandable, but if the costs of that rationality are leveled via taxes, that is another matter. Considering the gravity of energy issues, what do you think? As a result, it is natural to feel that public funds are involved in price increases unrelated to actual costs.

Whether we should call this state “public money siphoning” is debatable.The words are strong, but looking at the structure, it is natural for some to feel that way. How do you view fluctuations in gasoline prices?

Completely risk-free trading simulator to freely practice and verify!

One-Click FX Training MAX detailed page