Differences in taxation that affect your tax return! Differences between domestic FX and overseas FX taxes. Can't use tax incentives?

“If you have a domestic account you can carry forward losses, but what about overseas accounts?” In short,overseas FX is treated very differently tax-wise from domestic FX, and including rules on loss carryforward and netting gains and losses, you cannot use the favorable domestic “special cases.”in many cases.

Selling well!A high-functionality trading practice tool that feels like the real thing?9,800 yen?

?FX New Gen: One-Click FX Training MAX

?First, the core conclusion

- Domestic FX (over-the-counter FX with registered financial authorities):

- Principle-treated as “miscellaneous income related to derivative trading” (separate filing)

- Tax rate is generally fixed (around the 20% range)

- Loss carryforward is possible (up to 3 years) and gains/losses within the same category are easier to net

- Overseas FX (accounts with overseas brokers):

- Principle-treated as “miscellaneous income” (aggregate taxation)

- Income is combined with other income such as salary, which can raise the tax rate

- Loss carryforward is generally not allowed (hard to utilize losses in the following year)

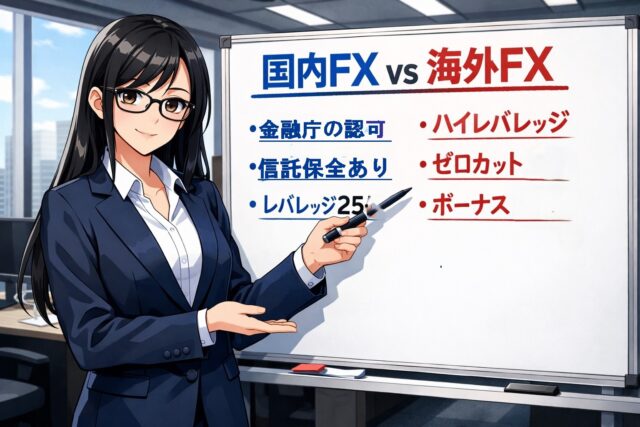

?Domestic FX vs Overseas FX

- Source of income

- Domestic: Separate taxation (“miscellaneous income related to derivative trading”)

- Overseas: Aggregate taxation (“miscellaneous income”)

- Tax rate image

- Domestic: generally fixed (about the 20% range)

- Overseas: tax rate may rise when combined (varies greatly by person)

- Treatment of losses

- Domestic: loss carryforwards may be available (with conditions)

- Overseas: loss carryforwards are often not usable

- Scope of netting gains and losses

- Domestic: easy to net within the same category (futures-related)

- Overseas: tends to be limited to miscellaneous income, narrow in scope

?As a company employee, the “progressive taxation trap” tends to occur

When overseas FX becomes aggregate taxation,

- Salary income + overseas FX profit + other income

is combined to determine the tax rate,the higher your main job income, the more likely overseas FX profits are taxed at a higher rate.

On the other hand, domestic FX is, in principle, calculated separately from other income, so the tax rate is fixed at 20.315%.

There is a common misunderstanding here.

“With aggregate taxation, couldn’t losses be offset against salary?”

In short, the answer is generally no.

Overseas FX losses are treated as “miscellaneous income minus,” but miscellaneous income cannot be netted against salary income.

- Salary: 5,000,000 yen

- Overseas FX: ▲1,000,000 yen

in that case, you are taxed on the 5,000,000 yen salary as is, and the ▲1,000,000 cannot be offset against salary. Moreover, this loss cannot generally be carried forward to the next year.

Aggregate taxation means “to determine tax rate by combining incomes,” not “to offset a deficit against other income.”

?Even within miscellaneous income, netting gains and losses is tough

On the other hand, it may be possible to net with other miscellaneous income (for example from another side business), but you generally cannot offset with salary income.

More importantly,you generally cannot offset domestic FX gains with overseas FX losses.

- Domestic FX: separate taxation (miscellaneous income related to derivative trading)

- Overseas FX: aggregate taxation of miscellaneous income

and because the classifications differ,

- Domestic FX: +1,000,000 yen

- Overseas FX: ▼1,000,000 yen

even in that case, you generally cannot net them to zero.

Domestic FX profits incur roughly the 20% tax range, while overseas FX ▲1,000,000 yen is likely to be written off in that year, creating a “twist.”

This is another point that people using both domestic and overseas accounts tend to overlook.

?Are there any tax-system-based advantages to overseas accounts?

From a tax perspective, the advantages of overseas FX are limited.

- If your main income is low and the applicable progressive tax rate is under 20%

- If other aggregate-taxed income is small

In such cases, the rate could end up lower than the flat ~20% of domestic FX.

However,

- Loss carryforward cannot be used

- Cannot net with domestic FX

- As income rises, tax rate may jump sharply

Therefore,in many cases, tax-wise it tends to be unfavorablein reality.

?Using a registered domestic account with the Financial Services Agency is the safe course

As seen so far,

- Loss carryforward is usable

- Gains and losses can be net within the same category

- Tax rate is essentially fixed and easy to understand

- Regulatory framework is well-established as a Financial Services Agency-registered practitioner

Therefore,from both tax and regulatory perspectives, using a Financial Services Agency-registered domestic account is more rational and safer.

While overseas accounts offer features like high leverage and zero-cancel,

- Tax disadvantages are likely

- Difficult to utilize losses

- Many cases where netting is not possible due to different classifications

- Regulatory protections and supervision differ from domestic ones

with such risks.

Excluding rare cases where tax rates are reduced (low-income bands, etc.),in terms of tax stability, predictability, and institutional reassurance, choosing a domestic Financial Services Agency-registered broker is prudentand realistic.

※This article is a general整理. Income classifications, loss netting, expenses, and carry-forward eligibility vary by individual circumstances. For actual filings, please consult a tax accountant or tax office.

Completely risk-free trading simulator to practice and verify freely!

Detail page for One-Click FX Training MAX