[Stock Analysis] Jigen (3679) can continue its rapid growth like this?

Summary

- Jigen (3679) is a company that operates a job/housing/lifestyle information search site.Rapid business expansion and M&A leading to rapid growth。

- The president is a young, shrewd executive who started as a student entrepreneur and later joined Recruityoung, capable manager. With that prowess, there is a strong possibility of continued rapid growth.

- The human resources industry is sensitive to economic conditions, and the large amount of goodwill arising from M&A, plus the lack of a standout strength, remaina major risk.

Stock Details

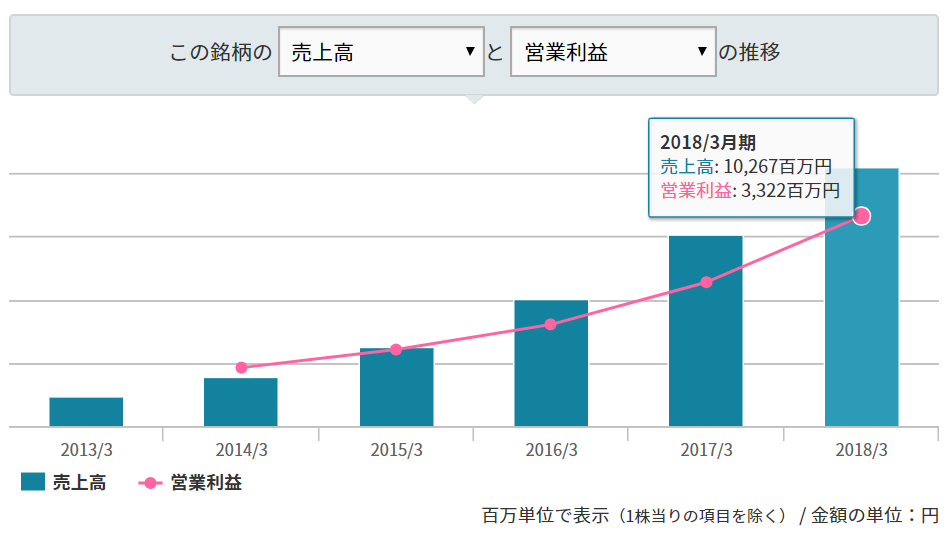

They operate information-search sites such as “転職EX (Career Change EX)”, “派遣EX (Temporary Staffing EX)”, and “賃貸EX (Rental EX)”.a company that runs human resources, real estate, and lifestyle-related information search sites. Founded in 2006, relatively young, with momentum in business expansion.

President Jo Hirao is a hands-on leader. He started a business while at Keio University, won the Tokyo Metropolitan Student Entrepreneur Championship, joined Recruit, and became the youngest group subsidiary CEO. In 2010, he acquired a joint venture between Dream Inc. and Recruit (MBO) and has continued to the present.

As a Recruit-affiliated company, the speed is remarkable. They continually launch sites and expand the business.

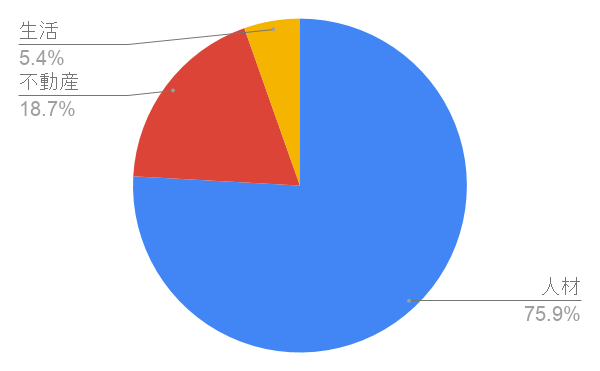

The main revenue pillars are human resources-related: job changes, dispatch, part-time work. A business model that aggregates information from job-change sites (such as doda, MyNavi Workplace, etc.) and sends traffic to these sites for advertising revenue. They also operate real estate and lifestyle-related sites.

Additionally, they aim for growth through M&A. They have completed 11 M&A deals totaling 9 billion yen since going public, contributing to business expansion.

Given the overwhelming speed and the management’s high awareness, they are likely to continue growing smoothly in the future.

However, there are several traps.

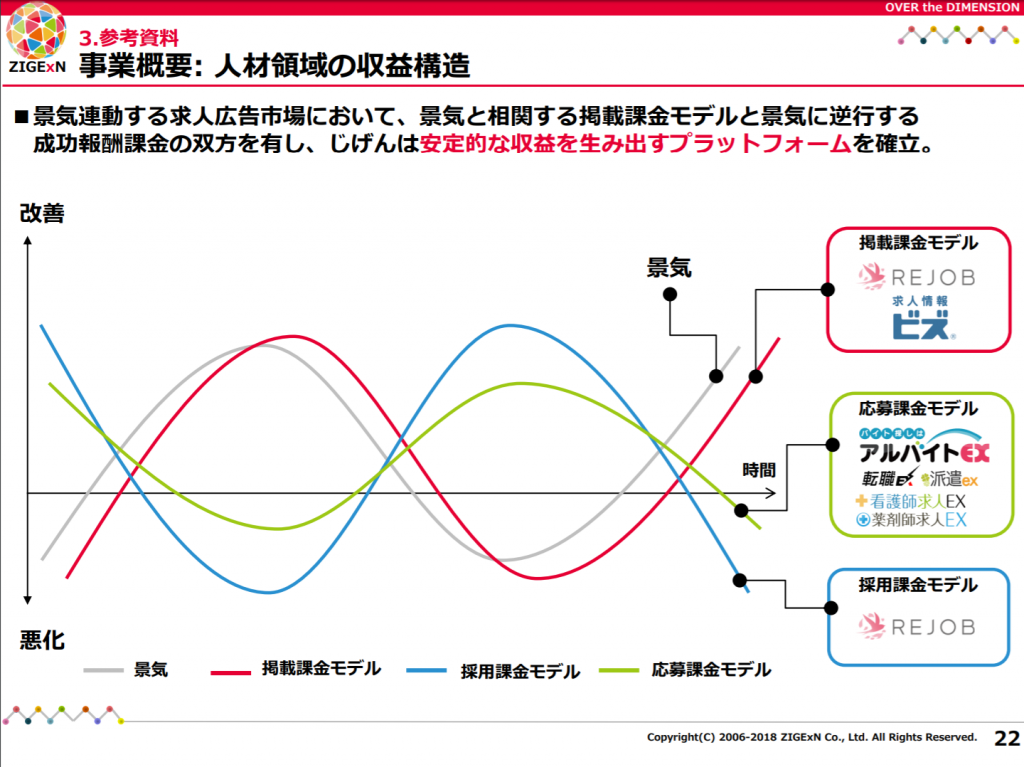

HR-related businesses are highly cyclical, and when the economy slows, existing sites are bound to be negatively affected to some extent. The company claims its success-based business model aligns with the economy, but as the economy worsens, hiring appetite for startups tends to dull, making that claim dubious.

Furthermore, the previously driving factor of growth,concerns about M&A.

For a 9 billion yen acquisition, goodwill is 7.5 billion yen. In other words, most of the purchase price exceeds the asset value. Goodwill must be written off if the acquired company’s profitability declines, andthere is a non-negligible risk of a large loss if the economy deteriorates.

Moreover, in the long term,there is no clear core strength to anchor the business. Certainly the management’s intelligence and grit exist, but I cannot see a business core that must be this particular company. I am not favorable toward this kind of Recruit-affiliated company.

As the overall market declines, the stock price falls, and the PER has dropped from a peak of about 60x to around 20x. Considering future economic downturns and long-term competitiveness,I would find this stock hard to buy.

Epilogue

Goodwill is the amount written off when the acquired company is deemed not to justify its acquisition price. It is not a loss at the time of purchase, but as goodwill increases, the potential for future significant losses grows.

Whether to recognize a loss is determined by “impairment tests” at each financial reporting period. These tests estimate the value of the acquired company based on various assumptions, butthe final numbers can be swayed quite a bit by simple adjustments.

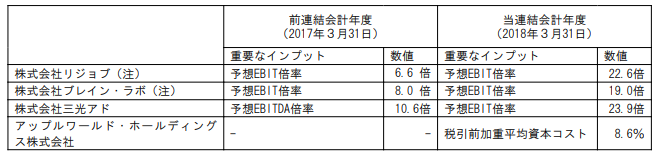

With this in mind, looking at the FY2019 (March) securities report, among the assumed figures the“projected EBIT multiple” has risen sharply from the previous year.

It may be speculation, but this rise could indicate that the subsidiary’s earnings are declining, and the assumed figures were adjusted to compensate. The average EBIT multiple is only around 10x, but here it has reached around 20x.

Although not outright fraud,this could be a yellow flag when estimating future losses.