[Brand Analysis] Ion Fantasy (4343) Accelerating its entry into China

Ion Fantasy (4343) is a shopping center centered on ion, operating a children's amusement facility

for kidsin a company. It is the largest in the industry. The parent company, AEON, holds 65%, and AEON accounts for about 60% of the facilities.

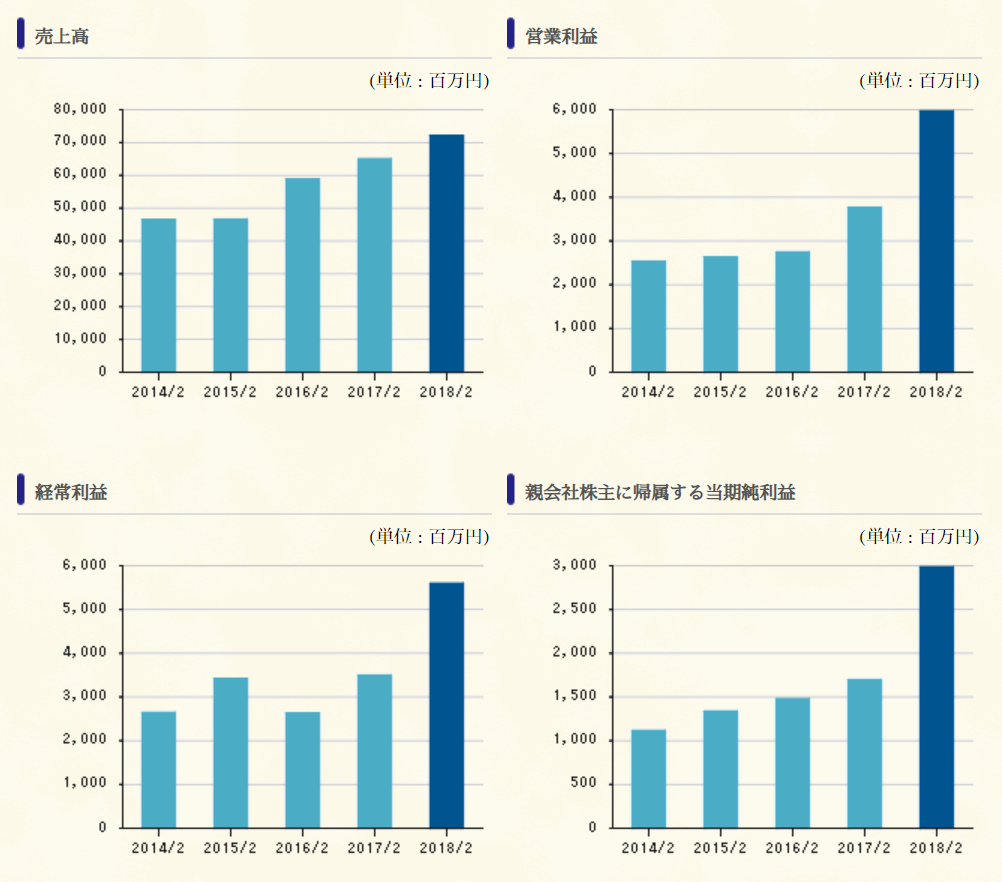

Recently, performance has been favorable. Effects from acquiring the Daiei group’s competitor FanField in 2015, andglobal expansionare beginning to show.

Regarding overseas, acceleration is being made especially inexpansion into ChinaDomestic 459 stores, overseas 389 stores (including 200 in China).

The company’s business is to provide play for children visiting shopping centers and their parents. The core of revenue is the prize division such as medal games and crane games.With few safe and fun places for children's play, there is a certain demand.

As a side note, my children (1 and 3 years old) also often play at the company’s facilities for preschoolers. It costs money, but it is easy to let them play and the satisfaction is high.

A strength is belonging to the AEON Group, which operates the largest retail business in Japan,but recent expansion beyond AEON is increasing. Overseas expansion is part of this.

In recent times, performance has been favorable, but there are signs of stumbling at present.For the 2018 March–November period, a profit decline occurred, and for the September–November period it turned to a loss. One factor is a rebound after a hit game the previous year, but I don’t think that is the only cause.

This business performs well when new, butas it gets old, customer flow declines. Even if depreciation on facilities has finished, fixed costs such as rent and personnel costs are high, deteriorating profitability. To revitalize, facilities must be renovated, which costs money.

Also, the competitive environment is not particularly favorable. It is safe within AEON, buta business that anyone can imitate, and especially if profits are good in places like China, it would be imitated quickly.

In the long run, it becomes a back-and-forth game of slowly losing customers and renovation costs,and profitability is unlikely to rise much. Profit margins are in single digits, and a slight misstep could push it into the red.

Even though the stock price has fallen, it might be best to avoid long-term holding as a business.