【Brand Analysis】MUJI (Ryohin Keikaku) (7453)

A company that is well known for distributing MUJI. A retail chain selling simple design miscellaneous goods, clothing, and additive-free foods.

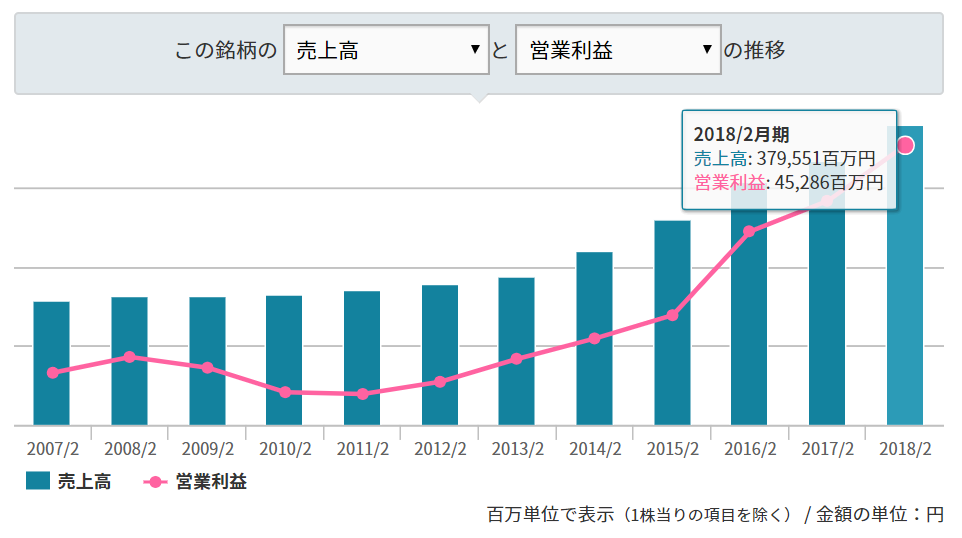

Its performance has been on a steadily upward trajectory.In addition to increasing the number of stores, the company is expanding broadly by moving from miscellaneous goods into foods and clothing.It has benefited from strong repeat demand and continues to show stable performance.

That said, domestic growth is slowing,with growth centered in East Asia such as China, Taiwan, and Korea. The sales mix is about 60% Japan and 30% East Asia, but East Asia is growing around 20% annually. It may well reverse in the not-too-distant future.

In particular,the popularity in China, where the middle-income class is expanding, is striking. In China, local companies acquired trademark rights ahead of the company, leading to litigation, but that also indicates how popular the brand is.

If it can also capture repeat demand in China as it has in Japan, growth can be expected to continue for the near future as the middle-income class expands. Also,under the concept of “simple and good things,” it has a strong advantage in being able to expand into various product categories. In Japan, it has entered houses and frozen foods as well.

Over the past five years, sales have grown at an annual rate of about 14%. Profits have grown at a similar pace. The P/E ratio has hovered around 20–30 times, and there is little chance of a substantial decline in the future.

With the decline in stock price, the P/E ratio fell to the early 20s, and briefly slipped below 20.As long as the P/E ratio is maintained, you can expect roughly a 15% annual increase in enterprise value. It operates essentially debt-free, with no financial concerns, and is a stock I would consider buying now.

At present, unstable stock prices and an economic downturn are concerns.The impact of the economy is not negligible, but not decisive. After the Lehman Brothers crisis, sales were sustained through price reductions, but profit margins declined.

Although long-term, robust growth is anticipated, the ideal timing may be when both earnings falter and stock prices fall. It is prudent to watch closely.