[Stock Analysis] Sodic trades at a P/E below 5

※Tsubame Investment Advisory Homepageis also available for viewing.

【Points of Investment】

- ・Sodick (6143) is a machine tool maker specializing in electrical discharge machines. Recently“China stimulus demand”has expanded its business.

- ・Machine tool manufacturers show large swings between boom and bust periods.The 10-year average P/E ratio relative to EPS is about 15x, not necessarily cheap, and there isn’t a guaranteed growth driver.

- ・In downturns, stock prices can fall offering opportunities, but regardless, competitive product strength and future investment are essential.Invest in companies with long-term prospects.

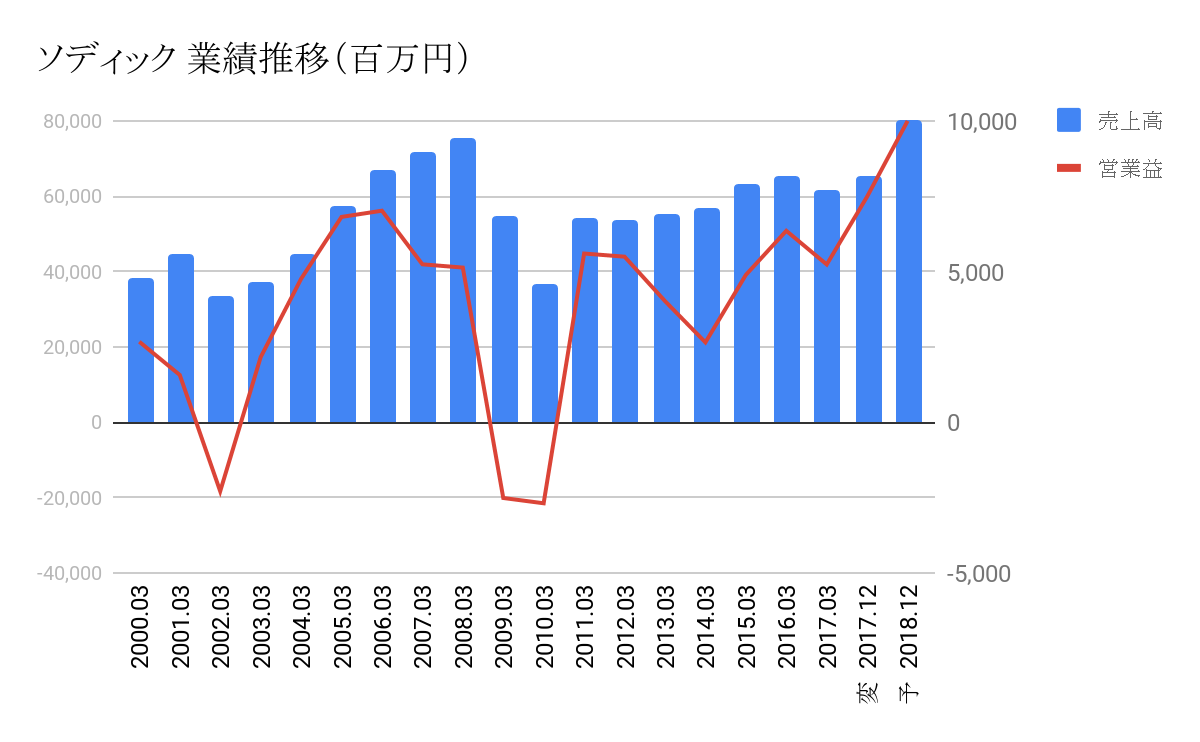

The favorable performance is driven by “China demand”

Sodick (6143) is a machine tool maker that specializes in electrical discharge machinesand holds a world-leading market share for these products.

Recent results have indeed been strong. Based on forecasts,this fiscal year's sales and operating profit are projected to reach record highs. In contrast, the P/E ratio is below 5x, appearing quite cheap.

However, looking at the underlying earnings, it isn’t clear that it is completely cheap.

The positive momentum stems fromsurging Chinese demand. Not only for Sodick, but for machine tool makers, strong Chinese demand has supported earnings growth over the past several years. Sodick appears to be riding that wave.

Discharge machines used by Sodick are instrumental in shaping the “mold” before manufacturing other machines or products. Molds are made from harder-than-usual metals, requiring specialized techniques. In that field,they developed the world’s first NC engraving EDM power supplyand that strength remains a competitive advantage.

Tending to and valuing the technologies developed in the past, the company has become an indispensable player in manufacturing—an archetypal trait of Japanese manufacturing. Even if the products shift from TVs to smartphones, the underlying technology remains valuable, and during favorable cycles earnings can grow substantially.

However, historical performance shows thatrevenue collapses in recessions and losses are recorded repeatedly, as capital investment tends to surge in booms but is postponed during downturns, causing demand to plummet. This is the fate of machine tool manufacturers.

In that sense, the current robust performance driven by “China stimulus” may not be reliable.The 10-year average P/E relative to EPS is about 15x.

Growth businesses are not yet developed

However, companies do not keep doing the same things forever.If new businesses are growing, those areas can drive growth beyond the business cycle.

Sodick is strengthening other domains besides EDM, such asmetal 3D printing and food machinery that is less sensitive to the economy.

Nevertheless, these are not guaranteed to be smooth.Metal 3D printing sales are currently only about 800 million yen, making it a long way from being a growth driver. Food machinery also would be difficult to become a growth driver unless it requires specialized technology.

Focus on long-term prospects rather than chasing near-term figures

We conducted screening based on numerical data this time, butlooking only at the present numbers can be dangerous. Recognizing the nature of the business and identifying what constitutes true value is, in our view, the core job of an analyst.

With Sodick,the traditional strengths remain viable, but there is no guarantee how long that will continue. With manufacturing shifting toward China, local firms may catch up.

Currently, the economy is buoyant,and earnings are exceeding actual capabilities, making it difficult to buy at the moment. At the same time, if the economy worsens, earnings may fall below actual capability, potentially making it severely undervalued.

If that happens, first check whether the business could become insolvent due to earnings declines, and if demand subsequently rises, ensure the company has the capability to produce competitive productsthat outpace rivals, which would present a prime opportunity.

Many companies fail to invest for the future during good times, only to face stagnation when the economy slows. Conversely, the truly good companies are those that accumulate inherent strength during downturns and still invest for the future during good times. We intend to continue seeking such firms.

※This article is an excerpt and edit of a report dated April 7, 2018.