【Brand Analysis】PER 7x, dividend yield 4% of Endō Lighting (6932)

※Tsubame Investment Advisory Home Pageis also available for viewing.

[Investment Points]

- Endo Lighting (6932) manufactures and sells lighting fixtures for commercial facilities.PER is at a low level of 7.4xand is renewing its year-to-date low.

- Around the fiscal year ending March 2013, profits expanded significantly due to rapid LED adoption. However, thereafterprofitability deteriorated due to price competition with late entrantsand domestic profits approached zero.

- A European subsidiary acquired in 2014 supports consolidated performance, butwithout improvements in domestic business, investment is difficultto justify.

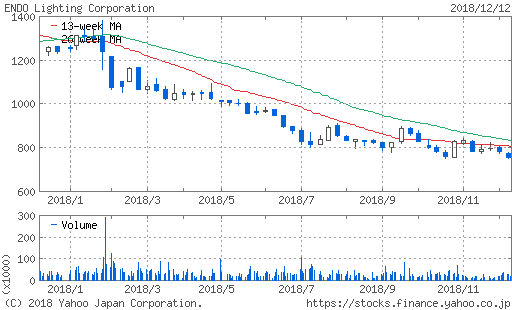

PER 7.4x and National Year-to-Date Low

Endo Lighting (6932) is a company thatmanufactures and sells lighting fixtures for commercial facilities. It calls itself a “high value-added space creation company” and in recent years has focused on LED lighting in its sales activities.

The reason to focus on it isthe low PER.This fiscal year’s predicted PER is 7.4x, below 10x, and the dividend yield reaches 4.0%. If similar performance can continue, it is a level that can be considered sufficiently undervalued.

The stock price is renewing its year-to-date low. Buying when it drops is a fundamental principle of value investing, and since the indicators align, we analyze the business fundamentals.

Sales have remained flat in recent years. Meanwhile, profitability has fluctuated, with a loss recorded in the fiscal year ending March 2016,with earnings levels alternatingand continuing to be volatile.

※2019/3 is company forecast

Looking at past performance, profits rose sharply around the fiscal year ending March 2013, after which they did not grow much. Revenue is nearly the same as today.That period appears to have been a major turning point for the company.

Benefiting from LED conversion and subsequent headwinds

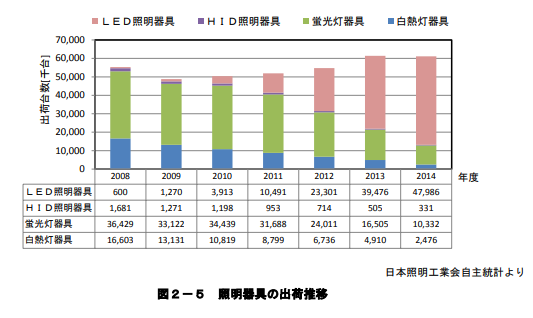

Nowadays, lighting is almost exclusively LED.Low power consumption and long lifespanare its features. Running costs are drastically reduced, so if a new installation is considered, LED is almost the only option.

Endo Lighting was quick to spot this. Being a specialized lighting company, its response was swift. For commercial facilities, reducing running costs yields clear benefits even if initial installation costs are higher,and the seller could enjoy wide profit margins.

Looking at the market,LED began to spread rapidly around 2012, aligning with Endo Lighting’s strong performance. Currently, almost 100% of new shipments are LED, indicating a complete replacement.

However, subsequent performance did not improve. The reason isthat late entrants caught up. For example, Iris Ohyama, known for affordable home appliances, is also investing in LED.

Early movers could generate large profits, but eventual competition intensified and margins shrank. The domestic sector is 최근赤字寸前. If kept as is, a recovery seems unlikely.

Overseas business supporting a sinking domestic operation

Still, the company remains in the black on a consolidated basis thanks to overseas divisions. In the latest earnings,Ansell, a UK lighting fixtures company acquired in 2014, accounts for most of the profits. The acquisition is considered a successful case.

Europe’s construction cycles are slower, so LED adoption is not as rapid as in Japan. Therefore, competition is milder there.The acquired overseas subsidiary now supports the declining domestic business.

Regarding overseas expansion,the plan is to expand not only in Europe but also in China and Asia. However, in emerging markets, price sensitivity is more pronounced than in Europe or other developed regions, making it not easy.

To view as an investment target,first the domestic business’s downward trend must be reversed. To achieve this, reorganization or a major strategic shift in core business is necessary. Without such changes, even with a PER of around 7x, it would be hard to call it cheap. A company with declining earnings cannot be considered undervalued regardless of how low the metric.

If signs of domestic business improvement appear, the current stock price level could present a buying opportunity.Looking forward to a major transformation.

※This article is an excerpt from a member report dated June 23, 2018.