Monte Carlo simulate the basics of market making strategies

Hello.

Recently I’ve been thinking about market making using APIs, but my main perspective has been as a buy-side practitioner, so I’d like to confirm the basics and I did a simple simulation. The Python code I used is at the end of the blog. It might be a reference for creating a crypto MM bot (the boom has been going on for almost a year now).

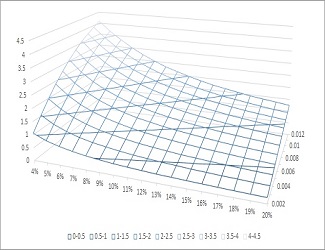

Basically, I am the only MM in the market, moving the price of the target asset according to a Wiener process, while receiving market orders from investors that are placed according to a certain probability distribution, and I do not hedge at all, just perform a Marie (offsetting buy and sell orders) and analyze how the final profit and loss will turn out.

To read more

http://delta-hedge.xyz/2018/12/04/mm-simulation/

On the blog, besides such standalone articles, we publish the following articles:

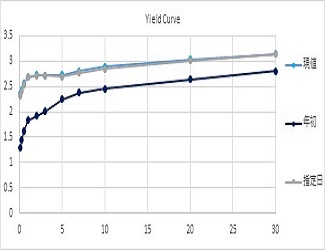

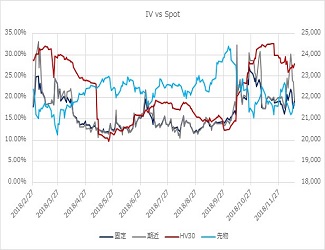

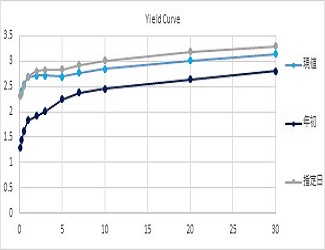

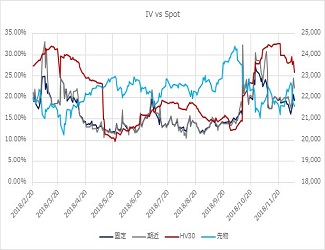

- Weekly analysis of Nikkei 225 options IV

- Weekly analysis of US interest rates

- How to implement IB Securities API using Python

- A roundup of market data available for free