[Results Published] For investment beginners, WealthNavi is good!

Hello, I’m Totti.

Technology progresses are truly remarkable, aren’t they?

“Robo-advisor: robots with financial algorithms automatically manage assets” is a dream for tech-minded people like me, lol.

This time, I will explain robo-advisors, a service where artificial intelligence (AI) automatically invests in various assets worldwide,based on my own performance and clearly for beginners.

1. What is a Robo-Advisor

As the name suggests,“robots (artificial intelligence: AI) invest according to financial algorithms”— a service that automatically invests in various assets around the world when you make a fixed monthly contribution.

Well-known ones include WealthNavi and THEO.

Most people aren’t traders, and they can’t become Warren Buffett, sothey have no idea about future movements of the market or individual stocks… right?

The Japanese government promotes investment policies like NISA, but how many Japanese actually invest?

From a detached perspective, I’d say only about 10–20% perhaps.

There are still manywho are just saving money.

This service is really recommended for beginners who are still just saving and considering starting investing.

Since long-term investing is the default,young people should try it.

I am usingWealthNavi, and I think it’s a really good service for investing beginners, so I wrote about WealthNavi this time.

By the way, WealthNavi is the robo-advisor service of WealthNavi Corporation, established in April 2015.

2. Good points of WealthNavi

(1) Can invest in a wide range of assets worldwide

Investingdistributes by “region” and “asset”, soindividuals can achieve a diversified portfolio, which is its biggest appeal.

- Regions to invest: Japan, developed markets, emerging markets, etc.

- Assets to invest in: financial assets (US stocks, Japanese/European stocks, emerging market stocks, US bonds), real assets (gold, real estate), etc.

In relation to volatility risk by region and asset,combining multiple regions and assets helps prevent a one-sided decline in asset value.

(2) Dollar-cost averaging

Investing a fixed amount every month causes the number of shares purchased to vary (dollar-cost averaging).

With this approach, when the market falls, you can buy more shares at a cheaper price, so you won’t despair; conversely, when the market rises, you buy fewer shares at a higher price, preventing you from overpaying at high prices.

However, if the regions or assets you invest in are consistently rising, you’ll gain profits, butif they trend downward, you may incur losses upon sale.

(3) Asset management is hands-off

Basically, after answering a few questions at the initial stage to determine your acceptable risk and setting it up, the rest isleft to the robot.

It’s easy.

Among readers of this blog, there aren’t any short-term traders, right?

Many have a full-time job,investing is a side job, orbeginner investors.

Staring at the market is really exhausting and hard to profit from.

(4) You can make use of compounding

I also wrote about piling up NISA (Tsumitate NISA), but basicallyit assumes long-term operation, soyou can benefit from compounding.

Related article:【Performance Disclosure】Tsumitate NISA is the strongest investment method for beginners!

Related article:【Performance Disclosure】The advantages and disadvantages of peer-to-peer lending and recommended operators

In short,“reinvesting investment gains”,in the long term, its power is enormous.

There is also a risk of principal loss, but in the long termUS stocks and others have been steadily growing, so a long-term “buy and hold” could be a good approach.

3. WealthNavi fees, etc.

Current fees are,an annual rate of 1.0% of assets under management (excluding tax) .

For example, with a principal of 1,000,000 yen, the fee would be 10,000 yen, so if the annual return is 5%, the investment return would be 50,000 yen; after deducting the fee 10,000 yen, the profit would be 40,000 yen.

In addition,the minimum investment is 100,000 yen, and automatic contributions are from 10,000 yen or more.

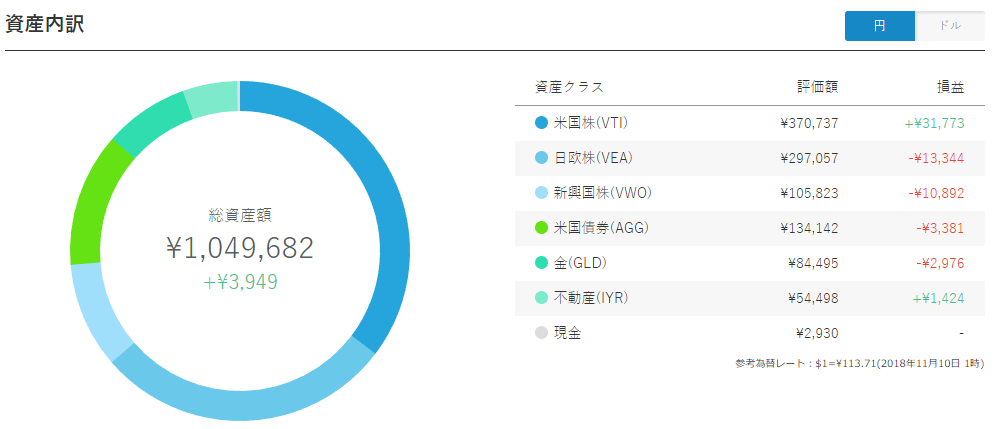

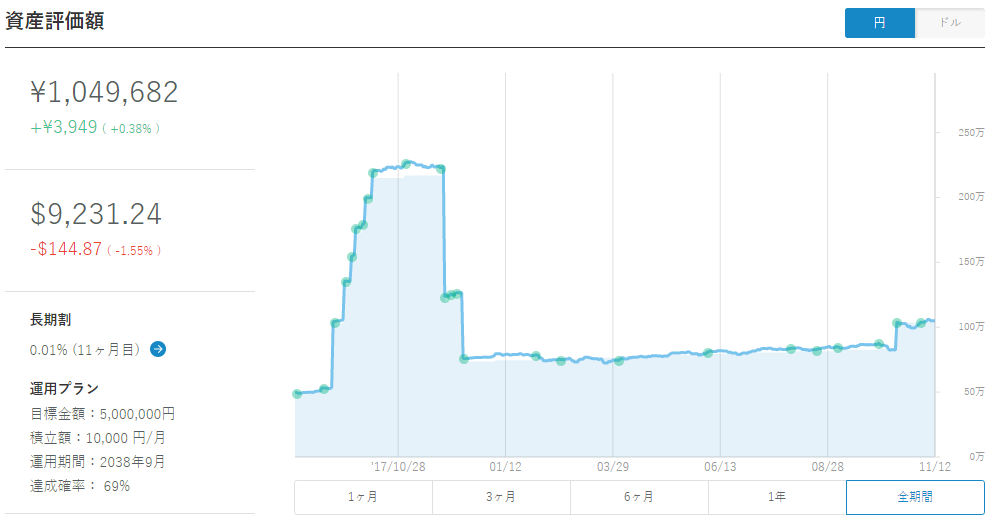

4. Annual performance disclosure

I will disclose my performance. Here it goes!

I started on August 20, 2017, contributed 10,000 yen every month, and managed assets for about 1 year and 3 months (risk tolerance 4).

As of now (November 12, 2018), the principal is 1,045,733 yen, with a profit of +3,949 yen and a rate of return of 0.38%.

(Note) I made several deposits and withdrawals along the way.

There was a time when the balance was over +100,000 yen… but with today’s global stock market slump, unrealized gains are almost gone. By portfolio,US stocks (VTI) are performing well, while others are dragging.

5. Summary

- Robo-advisors automatically invest in various global assets using AI.

- Basically, it’s fine to leave it to the service. WealthNavi is recommended.

- Combining multiple regions and assets helps prevent a one-sided decline in asset value.

- Long-term investing with small amounts is possible. Especially recommended for young people whose lives are long.

I’d be glad if this helps those considering robo-advisors.

Blog here