Using the bankruptcy probability of Barsala as a reference, unravel EA performance from backtests③

Unraveling the bankruptcy probability of an EURJPY EA that outs a 400%+ gain in 18 years

The first prepared EA is an EURJPY 1-hour dedicated EA.

With a 440% return over 18 years, a maximum drawdown of 9.7% relative to initial capital, a recovery factor averaging 2.46 per year, and an average of about 270 trades per year, the numbers look excellent for this EA.

Now, let's calculate each of these values.

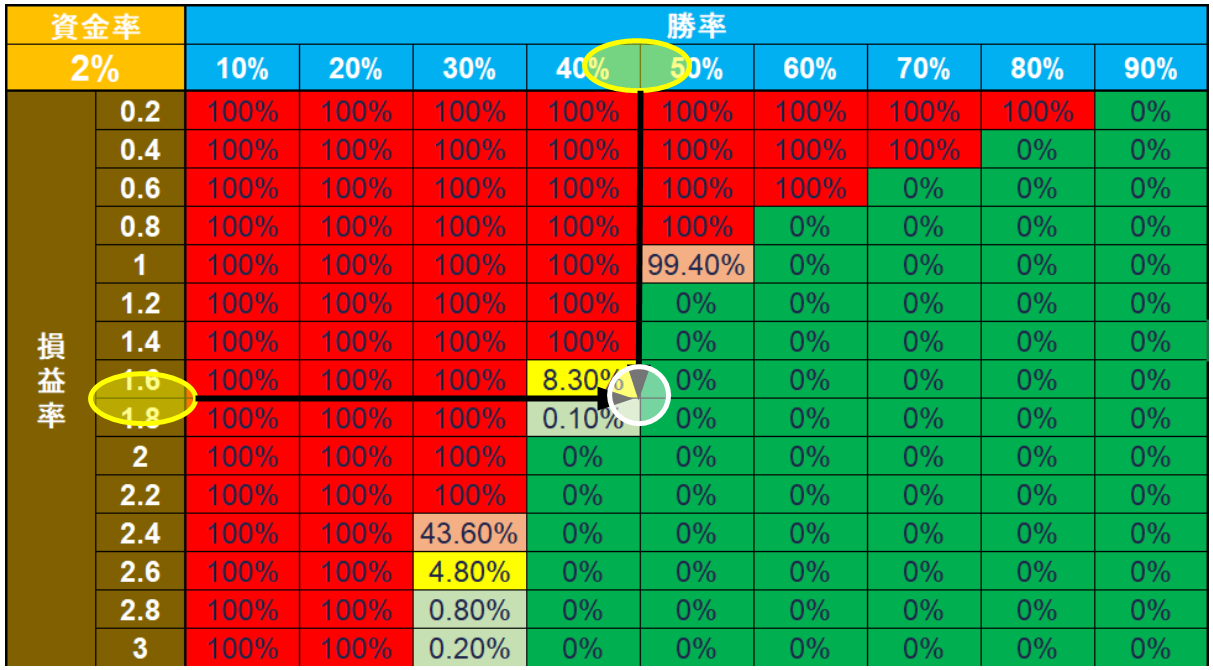

Win rate is「46.85%」

Average profit/loss ratio is「5731.88 ÷ 3383.27 = 1.695」で約1.7

Capital adequacy ratio is「20222.86 ÷ 1000000.00 =0.02」で2%

so we will use a 2% VaR bankruptcy probability table.

Since the win rate and the loss ratio are around the published figures, we add those four surrounding values and divide by 4.

8.30 + 0.10 + 0.0 + 0.0 = 8.4 ÷ 4 = 2.1

If this EA is operated with a capital of 1,000,000 yen and 0.1 lots, and it repeatedly trades at the maximum loss, the calculation yields“a 2.1% chance of bankruptcy”.

The EA will not repeatedly trade at the maximum loss, but“we cannot say it will never happen”, so please check how much risk you are taking when operating the EA.

That said, if the maximum loss yields a bankruptcy probability in the 2% range, you can generally operate without going bankrupt.

Next time, we will unravel an EA with a low win rate but a right-skewed profit/loss profile (small losses, large gains).

× ![]()