【FX】Trading using board information experiment begins MT4 automated trading (results report)

1. Introduction (Self-Introduction)

My name is Sabecks. I earn money with a self-made automated FX trading program (EA) for USD/JPY. I have created over 1000 EAs, and four of them are running regularly, among which two with high accuracy are currently being sold on GogoJungle.

Kyuubei: A high-win-rate EA that starts in the morning and earns steadily (not martingale)

https://www.gogojungle.co.jp/systemtrade/fx/46633?via=users

Gotoh-kun: The latest winning logic for Gotoh Day

https://www.gogojungle.co.jp/systemtrade/fx/50796?via=users

If you don’t mind, please at least take a look at its accuracy.

2. Experimental Content

This is an experiment to see whether trading using the price board information provided by Gaitame.com can be profitable.

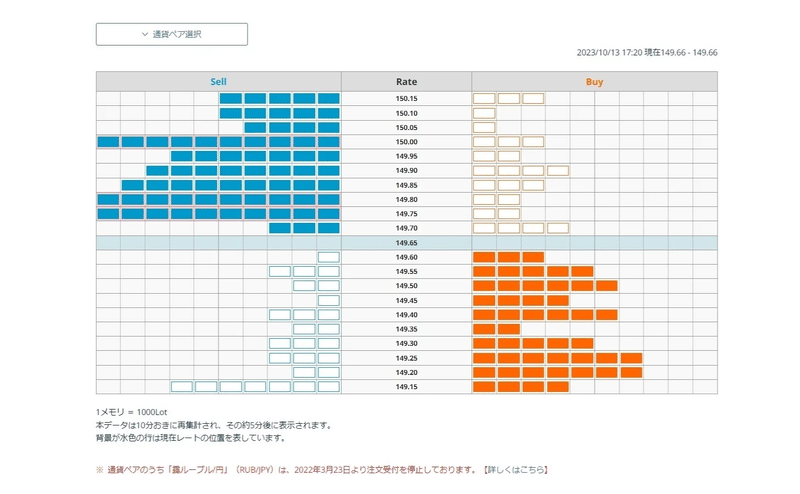

2.1 What is the order book information

Order book information represents the prices and quantities of buy and sell orders.

https://www.gaitame.com/markets/order/

On the above site, you can see orders placed by Gaitame.com users.

The order book information appears as follows.

2.2 Experiment content

We hypothesized that the price would reverse at full-scale tick marks on the order book. In the image above, the reversal and rise would occur around 149.75–149.80, and if you entered a sell position at the reversal, you could win.

In other words, because order book information shows actual orders, the market would move accordingly where there are many bids or asks.

I built a system that retrieves order book information from the Forex Dot Com board using automated trading (MT4). Please refer to the article below for details of the system I built.

https://www.gogojungle.co.jp/finance/navi/articles/61074

This experiment investigates what happens when buying and selling using real-time changing order book information via automated trading.

3. Experimental Results

It would have been nice to display the trading records with a graph, but they mixed with other trade data, so I will only report the results.

As a result, the conclusion is that the method is “effective in certain market conditions.”

What I did was to use the order book information to time the reversal and execute trades on a counter-trend basis.

That is, if 150.00 yen is at full scale on the order book, I would enter a sell position assuming a reversal at 150.00 yen.

After actually running it with automated trading, it could be broadly classified into four patterns.

Pattern 1: Price does not reach the level

Pattern 2: Price briefly reaches the level

Pattern 3: Price exceeds the level and then comes down

Pattern 4: Price exceeds the level and keeps rising without falling back

For each pattern, if Pattern 1 does not reach the level, you can ignore it since the automated trading would automatically take a position when the level is reached.

Patterns 2 and 3 are essentially reversal patterns, so you want to capture them well with automated trading.

Pattern 4 is a losing pattern. If Pattern 4 occurs, there’s no choice but to cut losses.

At first, I entered with the expectation that reversal would occur when the tick mark was full, and I would fill orders when the 5-minute Heikin-Ashi (average bar) showed reversal.

However, to reduce losses from Pattern 4, I changed the entry condition to “enter when the price has exceeded and the Heikin-Ashi shows a reversal signal.”

Then I built it so that entries would execute when the reversal happened again with the Heikin-Ashi. This was done to attempt to profit even in Pattern 4.

By doing this, I considered earning some profit even in Pattern 3, and even slight profit in Pattern 4. The losing pattern occurred when the Heikin-Ashi failed to express reversal properly.

In conclusion, I said it was “effective in certain market conditions.” This was because in USD/JPY, when the price approached 150 yen, the market faced resistance and the order book tick marks were full and reversed frequently, allowing for substantial profits.

However, when there is no resistance, or when there is no heavy selling or bottom support, the order book tick marks seldom reach full scale.

During a single day, there may be only one instance of full-scale tick marks, causing the operating rate to drop sharply.

Thus, this automated program does not move much to begin with.

And even when it moves, it tends to capture only small reversals, so it cannot earn large profits.

Nevertheless, it was effective in situations where the market seemed to be stalling before whether the 150 yen barrier would be broken.

Therefore, I would say that “the reversal strategy based on order book information is an effective approach in markets with a visible barrier that causes standstill.”Also, a key point is that after economic indicators are released, there is often a strong break through the barrier, so after indicator releases and during NY time, it is important not to run this reversal program.

4. Summary

From this experiment, I found the approach of building an automated program using order book information to be very interesting.

Using order book information allows the automated program to incorporate the decision criteria of many other people, and also to incorporate human judgments that automated programs typically cannot.

Using order book information makes it possible to program trades in real time based on human judgment, which is fascinating.

When considering markets as driven by crowd psychology, order book information is a very valuable source of information.

I would like to refine the program I made this time a bit more so that it runs in barrier situations.

Wouldn’t you also like to try trading using order book information?

The key is to use it when the order book is full, i.e., when trade information is concentrated.

Automated programs still find it difficult to capture the most optimal entry and execution points.

Discretionary trading using order book information also seems viable if you can keep monitoring the market.

That concludes my report.

Thank you for reading this far, m(_ _)m

See you somewhere again