No over-optimization, with a favorable risk-reward ratio, '千紫万紅'

【Thousand Purple, Ten Thousand Red Overview】

Currency pair: [USD/JPY]

Trading style: [Scalping][Day Trade]

Maximum positions: 2; Other: Can be changed from 2 to 4 via parameters.

Maximum lots: 40; Other: This is the maximum lot size set by the broker.

Used timeframe: M5

Maximum stop loss: 90

Take profit: 90

【Trading Logic】

Using four moving averages, Bollinger Bands, and a Stochastic oscillator

Simple buy-the-dip and sell-the-rally strategy

【Trading Image】

When entering, two positions are opened at staggered times; exits are performed as either at the same price or distributed across orders.

Take profit and stop are both 90 pips, but logic-based exits help reduce losses.

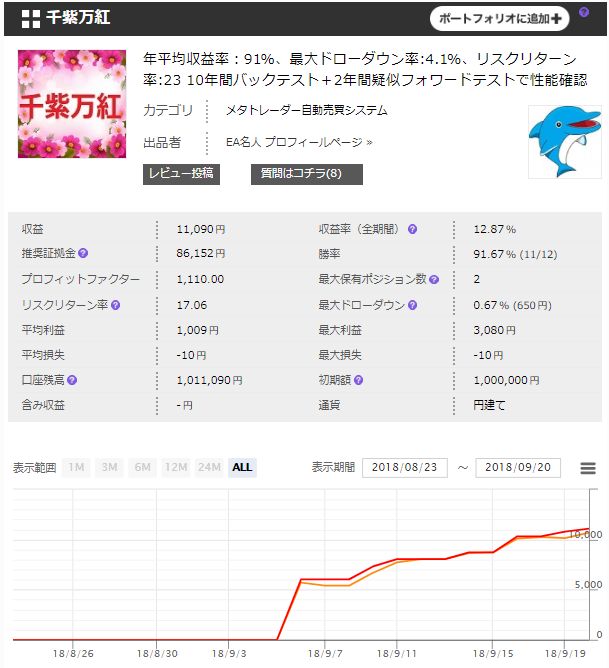

In forward testing, we operate with a fixed 0.1 lot, but,

during the period the maximum drawdown is 640 yen, while profits exceed 10,000 yen, resulting in a very high risk-return ratio.

Stops and take-profit are both 90 pips, making it unlikely to experience a string of small losses turning into a big one.

Now, how about backtesting? Let's take a look.

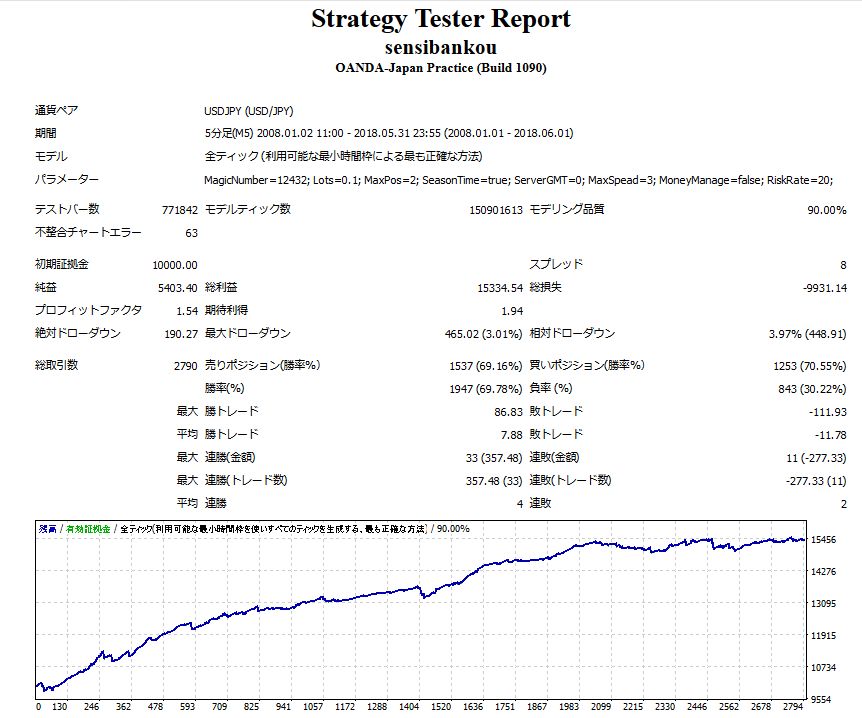

【Backtest Analysis】

2008.01.01-2018.06.01

0.1 lot fixed

Spread 0.8 pips

Net profit +$5,403

Maximum drawdown -$465

Win rate 69%

Total trades: 2,790

Thus.

Even with two positions, the maximum drawdown is as low as -$465.

Trade count is about 250 per year. Since two positions are taken at once, it may feel like about 100 per year.

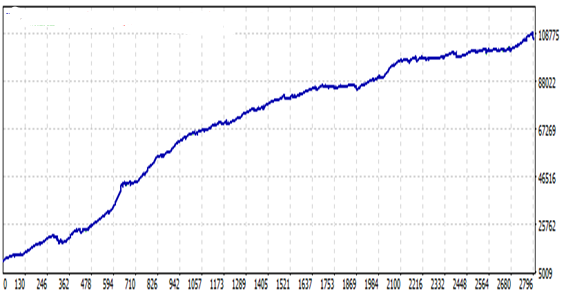

【Monthly and Yearly P/L】

On a monthly basis, December tends to be more prone to losses.

On a yearly basis, profits have been relatively low in the recent years.

Higher volatility seems to correlate with higher profits!

【Recommended Margin and Expected Annual Return】

Recommended margin per 0.1 lot is

(4.5×2)+(5.4×2)=19.8

You can start with about 200,000 yen.

Expected annual profit, averaged over 10 years, is 58,000 yen, corresponding to a 30% return.

【What is Pseudo-Forward Test?】

As a feature of Thousand Purple, Ten Thousand Red, we note that a "pseudo-forward test" is performed.

The following is an excerpt from the Investment Navi+ seller's article, "EA Without Curve-Fitting by Optimization"EA Without Curve-Fitting by Optimization"抜粋

■ Pseudo Forward Test

・You can determine whether performing a pseudo-forward test constitutes curve fitting.

This is a method employed in MT5.

・Here is an example using my upcoming released EA, "千紫万紅".

・During the first 10 years of the past 12 years, optimization was performed using Strategy Tester,

and the remaining 2 years were forward-tested with the same parameters using Strategy Tester,

to verify performance.

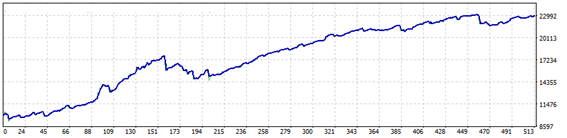

10-year backtest

・Period: 2006-08-01 to 2016-08-01

・Net profit: 96,342

・Average annual return: 96.3%

・Maximum drawdown: 3,692

・Expectancy: 34.51

・Win rate: 73.50%

・Total trades: 2,792(273 per year)

2-year forward test

・Period: 2016-08-01 to 2018-08-01

・Net profit: 13,014

・Average annual return: 65.1%

・Maximum drawdown: 3,388

・Profit factor: 1.77

・Expectancy: 25.42

・Win rate: 70.90%

・Total trades: 512 (256 per year)

・Returns, win rate, and number of trades are somewhat lower, but profits still clearly

have been achieved.

Forward testing results are very good, so higher-than-average annual returns seem likely.

How much profit would there be over 3 months of forward testing with 0.1 lot?

Will it yield similar results to the pseudo-forward test? Real forward testing is also anticipated!