High-probability averaging down × automatic compounding to double profits "Two-Sword Style Flurry"

【Two-Sword Rapid Fire Overview】

Currency Pair: [USD/JPY]

Trading Style: [Scalping][Day Trade]

Maximum number of positions: 23 (20 positions + 3 averaging-down positions)

Timeframe used: M5

Maximum Stop Loss: 100

Take Profit: 40

Forward testing: 2 months

Profit: +130,000 JPY

Pips gained: 1194 pips

Number of trades: 238

That's it!

Forward testing uses the default compounding setting,

Sizing starts from 0.05 lots per 1 million yen of margin.

【Logic】

The basic strategy is layering multiple Bollinger Bands.

We perform a precise, targeted averaging-down once per position.

There are three averaging-down widths, and if there are positions being averaged down,

we select the next averaging-down width to address drawdown.

If an opportunity arises while holding a position, we enter the next position to take advantage,

we do not miss the opportunity.

※ Maximum 20 positions + 3 averaging-down positions

Because the number of positions is large, margin calculation with fixed lots is difficult, but

if you turn on automatic compounding, it will adjust lots to a pre-set maximum DD% for you,

so it's simple and recommended!

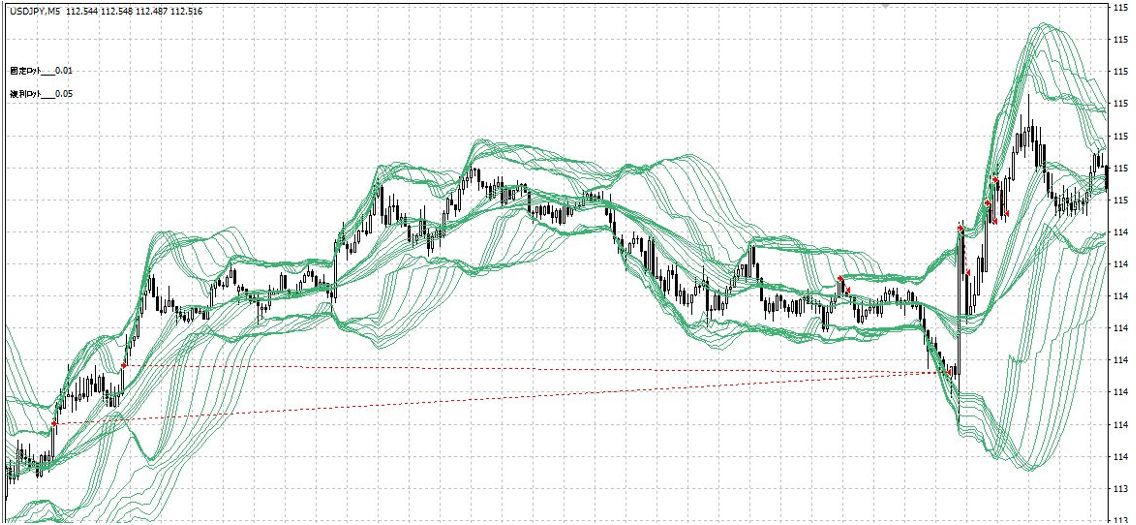

【Entry Example】

Red: SELL

When you have averaging-down positions, adjust the next averaging-down width.

If the initial lot is 0.05,

the second position may be 0.12 or 1.35, depending on the averaging-down width.

Basically, at one entry point we only place up to two entries, so unrealized loss

will not continue to increase indefinitely

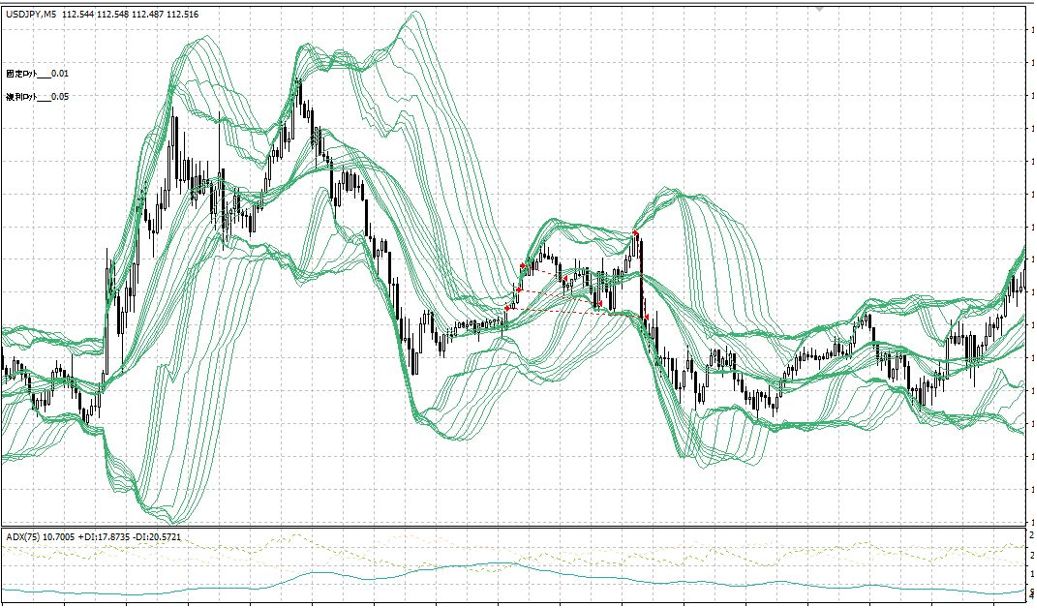

Using multiple moving averages plus multiple Bollinger Bands and applying a trend filter with ADX,

it seems to be a contrarian strategy that goes long when the market is not turbulent!

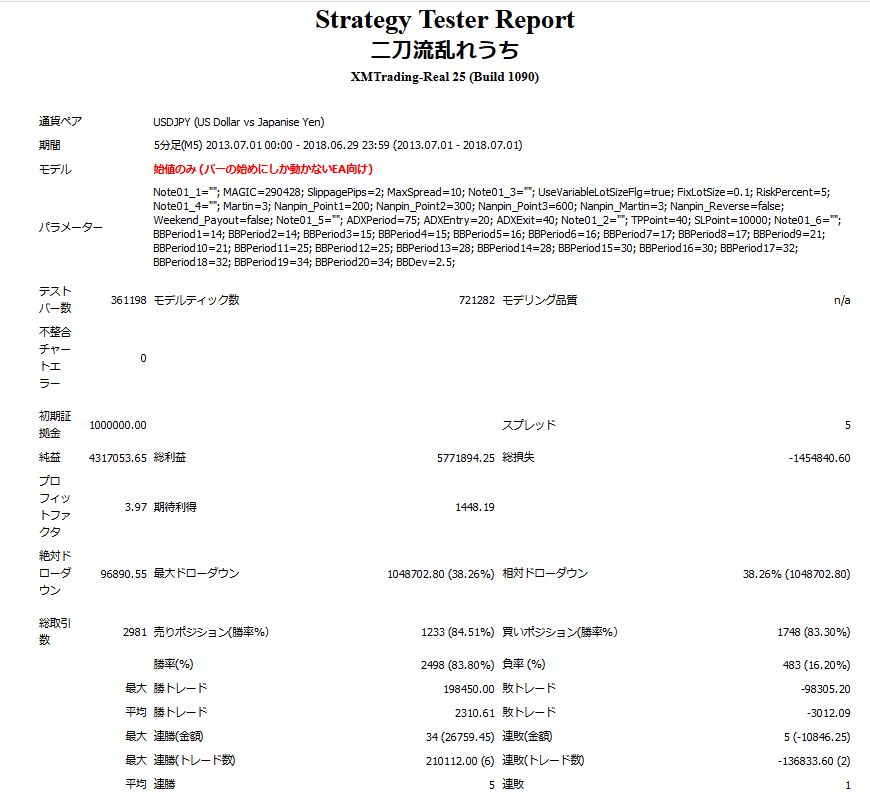

【Backtest Analysis】

Five-year backtest results with compounding ON and default settings are shown here

2015.07.01-2018.07.01

Compounding ON, Margin 1,000,000 JPY

Relative drawdown 38%

Net profit +4,300,000 JPY

Total trades 2981

This is the result. For compounding, please consider the relative drawdown.

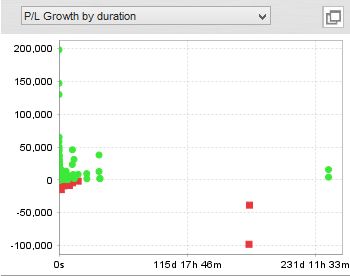

【Monthly P/L】

Because it is an averaging-down EA, there are hardly any negative months.

January 2018 was negative because positions opened in January

were forcibly liquidated when the backtest ended in July, causing the loss.

Averaging-down is a drawback unless it is resolved, but

it is a trade-off that also contributes to monthly profit.

From the backtest, the maximum holding time was 243 days, starting in January 2014.243 days.

However, on average, it tends to close within a few days.

(Two of these are forced liquidations due to backtest end.)

Because it occurs only once every few years, if you're concerned,

you may quickly close them manually.

【Annual Trades and Win Rate Win Rate】

Annual number of trades is about 600 per year.

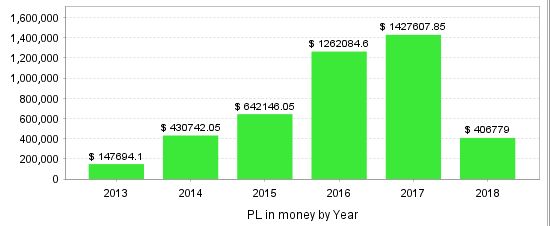

【Annual Profit】

Because of compounding, it increases as years pass.

Over five years of operation, from 1,000,000 yen to 5,300,000 yen,+530%.

With averaging-down EAs, the most alarming risk is that unrealized losses increase during sharp market moves and the account can blow up, but

the \"Two-Sword Rapid Fire\" limits the number of averaging-downs per trade and the total number of positions,

and with the automatic compounding feature risk is easily controlled, which is good.

Also, instead of averaging down by price range, it uses strategic averaging-down in high-win-rate areas, making it a short-term setup

which is another attraction.

We cannot simply derive a exact annual yield, but with compounding you might expect around +50% per year.