[Episode 4] System Trading Portfolio and the Volatility Trap

The 4th installment of "System Trading for Top Intelligence" covers the System Trading Portfolio and the Volatility Trap.

The main site isInitiative - Future-thinking System TraderThis site handles a wider range of phenomena, but in "System Trading for Top Intelligence" we dig deeper into the themes, so please bear with us.

【System Trading Portfolio】

Suppose there are systems with roughly break-even profits and losses. If a system can be incorporated into a portfolio with low correlation to the currently operating trading systems, it becomes a candidate for inclusion in the portfolio.If the currently operating trading systems show an upward trend, daily profit and loss fluctuations (the ups and downs) tend to move smoothly. If volatility of profits and losses becomes smoother, leveraging can aim for even higher returns.

It would be easiest to explain with images, so please see below.

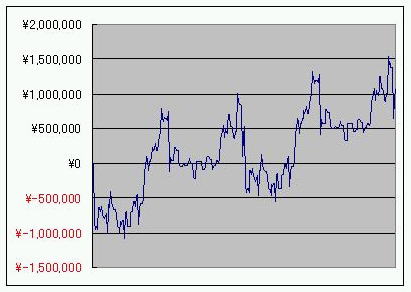

Currently operating trading systems

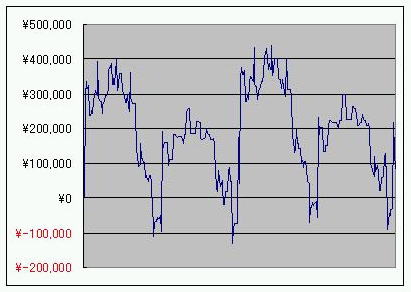

System with roughly break-even profits and losses

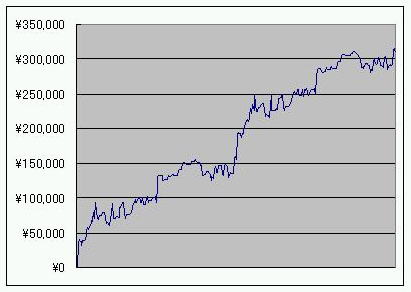

System after portfolio inclusion

【Volatility Trap】

Assume a low-volatility portfolio exists. This portfolio could be mutual fund returns, trading system profit curves, or anything else, but I want to consider here whether a low-volatility portfolio can truly be said to have lower risk. Generally, low-volatility portfolios are considered to have lower risk, but in many cases that is not actually true. Personal investors often have a better sense of this than institutional investors.

1) Past performance does not indicate future performance.

Events such as the Lehman Crisis, the Great East Japan Earthquake, Brexit, and the election of President Trump cannot be explained by past price movements. People often feel that past performance does not predict future performance, yet in calm times they may assume that the trend will continue. Be aware that anything can happen in the future.

2) The time frame of performance evaluation changes the volatility calculation.

Widening the time frame tends to understate volatility. For example, even if there is sharp movement within a day, if you only look at the closing price that movement is not reflected, and volatility is understated.

3) Common volatility calculations include both upward and downward fluctuations.

A portfolio gradually making lower lows has low volatility, but obviously it is not profitable. In finance, risk may refer to price movement, but investing in such a portfolio makes little sense, and it is correct to say the risk is high. Personal investors' intuition is often more accurate.

【Summary】

While I argue that trading system profit and loss should be smooth, I also question whether simply low volatility is acceptable. Dividing volatility into upper and lower limits is one useful solution. I believe reducing profit and loss fluctuations as much as possible while aiming for high returns with leverage is the correct stance for individual investors when facing the market. Let's both work hard to achieve substantial profits!

---------------------------------------------------------------------

Top Intelligence is a term derived from top athletes, used to mean athletes who use their brains. Trading requires practice and mental imagery, just like athletes. In real use, you never know what will happen, but the demand for results is the same as for athletes. And for that reason, we continue training. There are times when things don’t go well, but we do not give up. We pursue the summit with an unyielding spirit (resilience).

Until now, elite and intelligence have often been emphasized as fragile and delicate like glass, but we aim to cultivate what you could call a hybrid vigor and push forward. Let us, with a top intelligence who is incredibly tough, walk toward the ideal together with readers.

As much as possible, we publish strategies and adopt an open-source approach. Through output and refinement of ideas, let us evolve each other’s investing techniques.