7/7 Very strong U.S. economy & employment data ahead

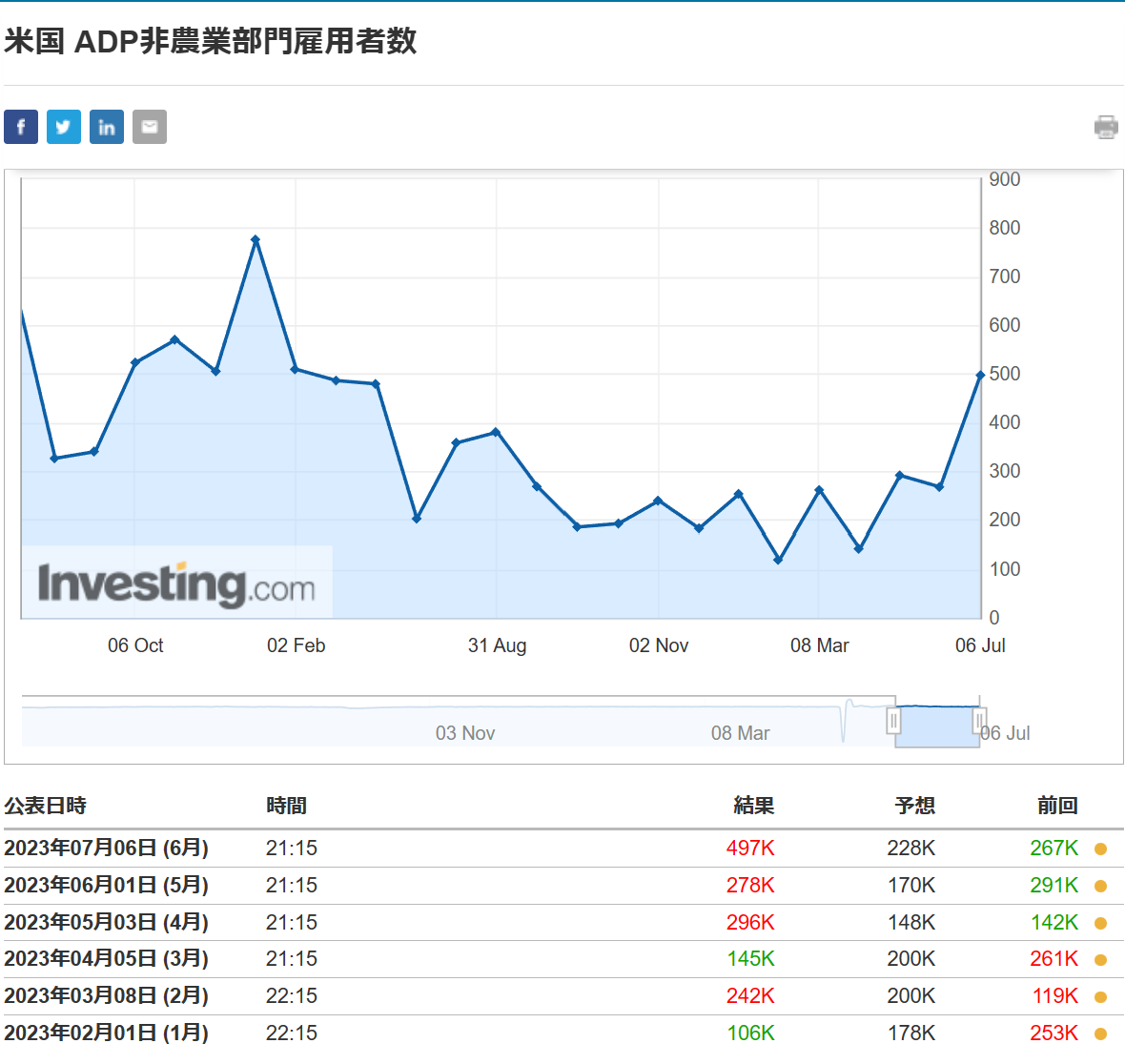

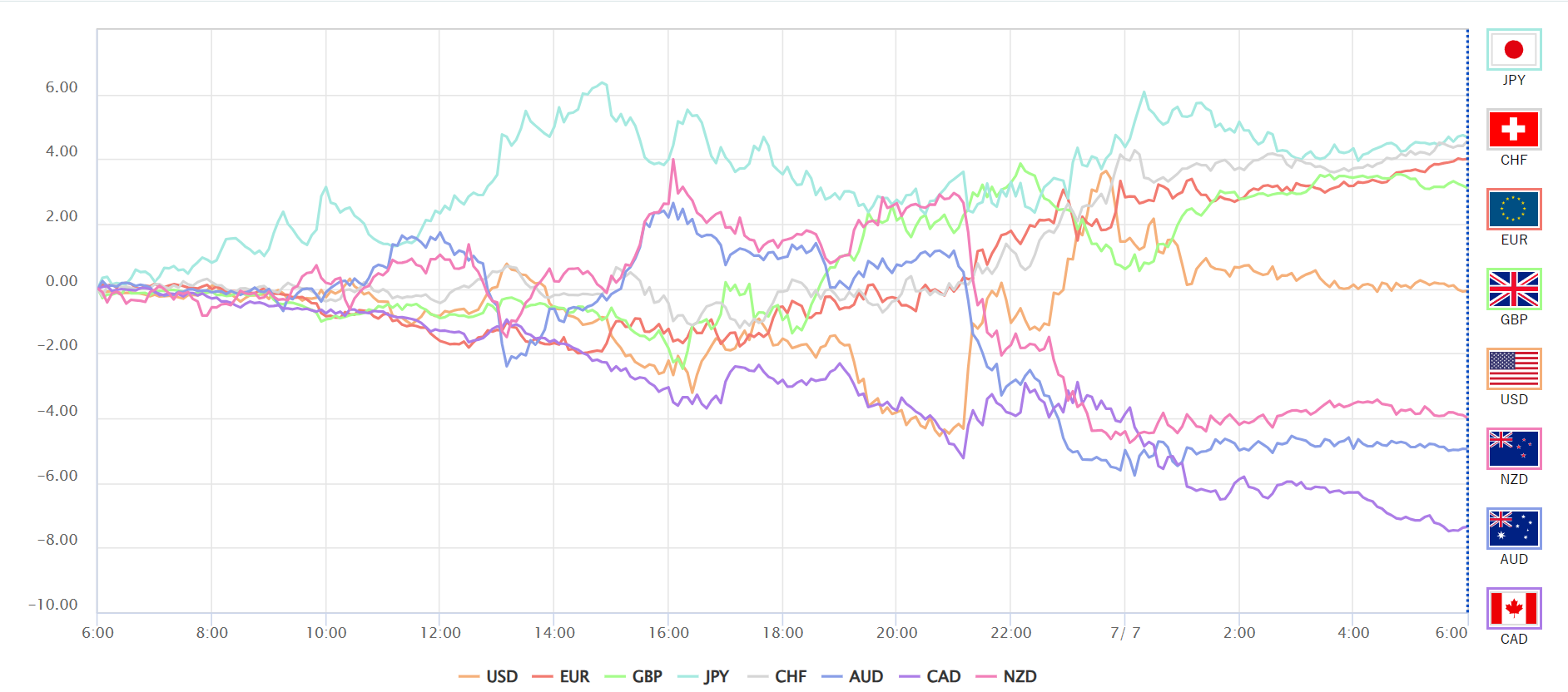

Yesterday's US indicators delivered very strong results. While reviewing, I want to check, but first the ADP employment report unsurprisingly diverged significantly from expectations, coming in at 497,000, and with liquidity being tight ahead of today's employment statistics, the dollar strengthened substantially as a reaction.

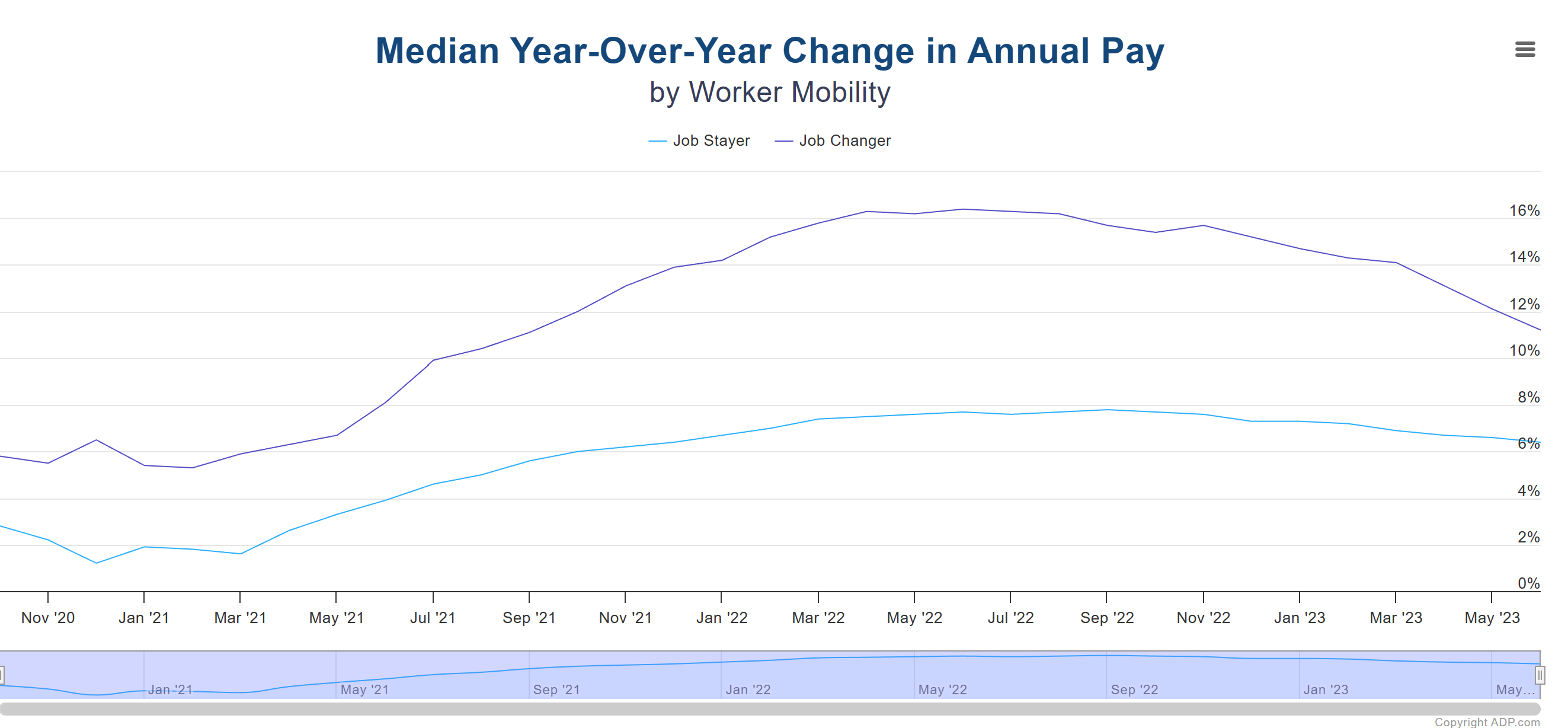

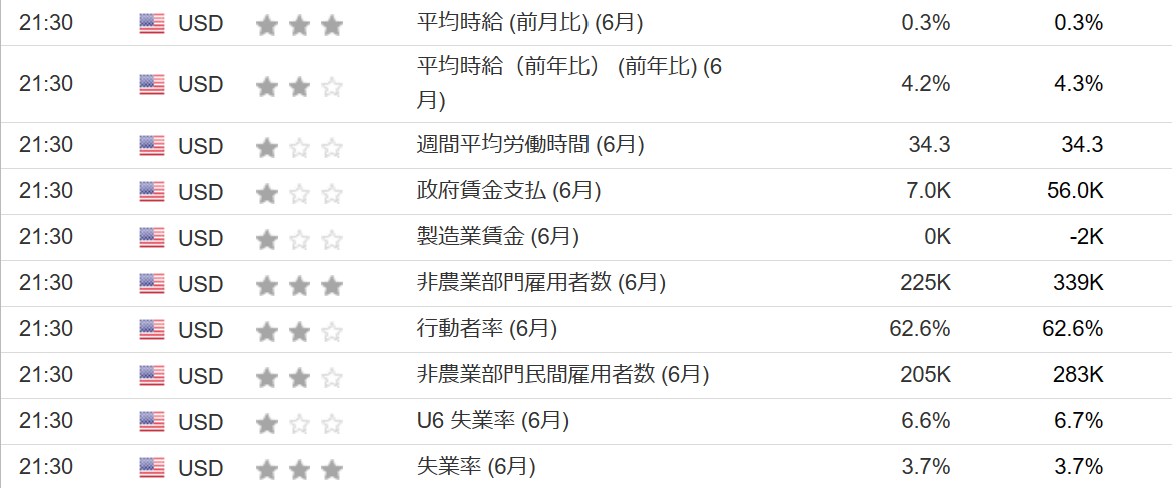

In the wage component, since the growth rate is shrinking steadily, wage inflation is being regarded as contained, and today’s average hourly wage does not seem likely to show a large upside surprise.

The ISM Non-Manufacturing PMI indicates disinflation and is very strong. I cannot attach the ISM monthly report here, so please check it yourselves; the price index exceeded expectations, but it has clearly declined from the previous month, showing that inflation is being suppressed. Orders, employment, production, and nearly all other components are rising. The services sector shows a very strong result.

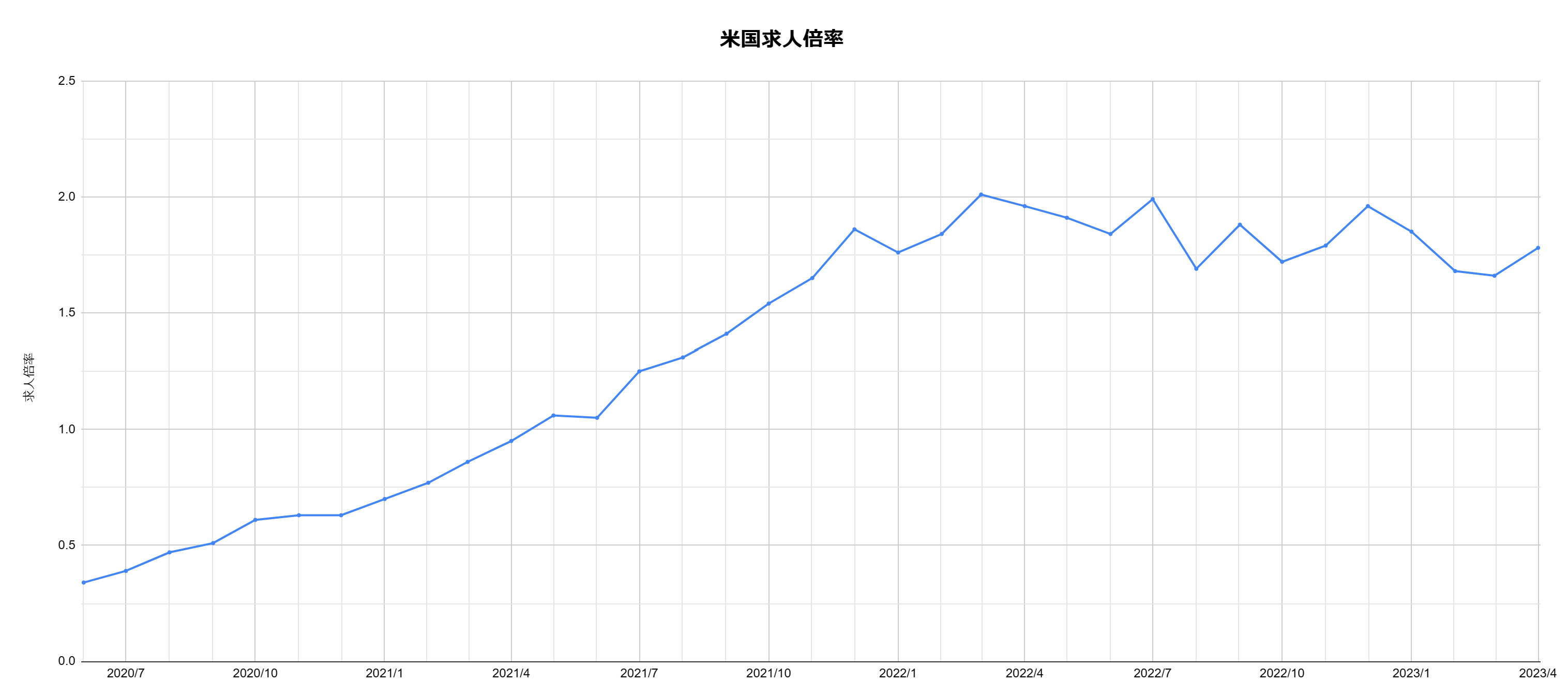

Subsequently, with the release of Jolts job openings and the ISM Non-Manufacturing PMI, Jolts job openings declined. Labor demand is expected to gradually decrease, but I would like to use today’s unemployment rate in conjunction with this to form a wage inflation outlook. The job openings-to-unemployed ratio, calculated as job openings divided by the number of unemployed, has risen from last month, and the ratio tends to lead wage growth about six months ahead. Therefore, if the unemployment rate falls significantly, it could push the job openings ratio higher, so this is worth watching.

Regarding today’s employment statistics, the forecast for employment, even when looking at ISM employment, remains low and is not expected to undershoot. Looking at the ADP wages, average hourly earnings do not appear likely to rise sharply. As for the unemployment rate, although layoffs are progressing, the figure from last month’s release suggests a certain trend.Using the CB Consumer Confidence Index, expectations for employment opportunities improved from 43.3 to 46.8, and the outlook became more optimistic as the index for judgments about employment opportunities rose from 12.6 to 12.4. Since this index correlates with unemployment, this would likely suppress the unemployment rate, as anticipated.

Seasonally, June tends to see relatively fewer staffing cuts, and considering the Challenger layoff data released yesterday, which has fallen to January levels, I think unemployment will not rise this month, but we should be cautious about the potential for sticky wage inflation.

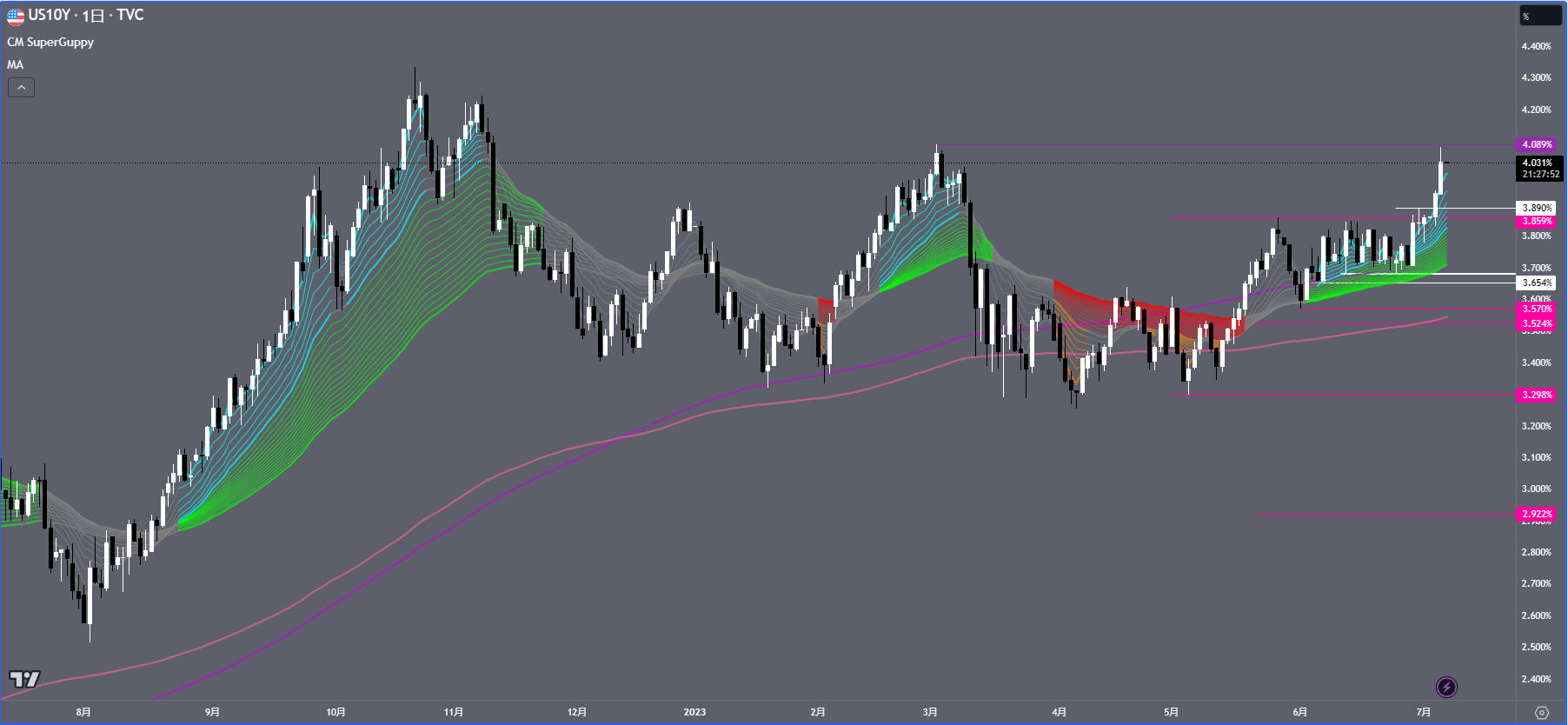

Following yesterday’s data, the US 10-year Treasury yield rose to around the March high of 4.1% and moved into the 4% range.

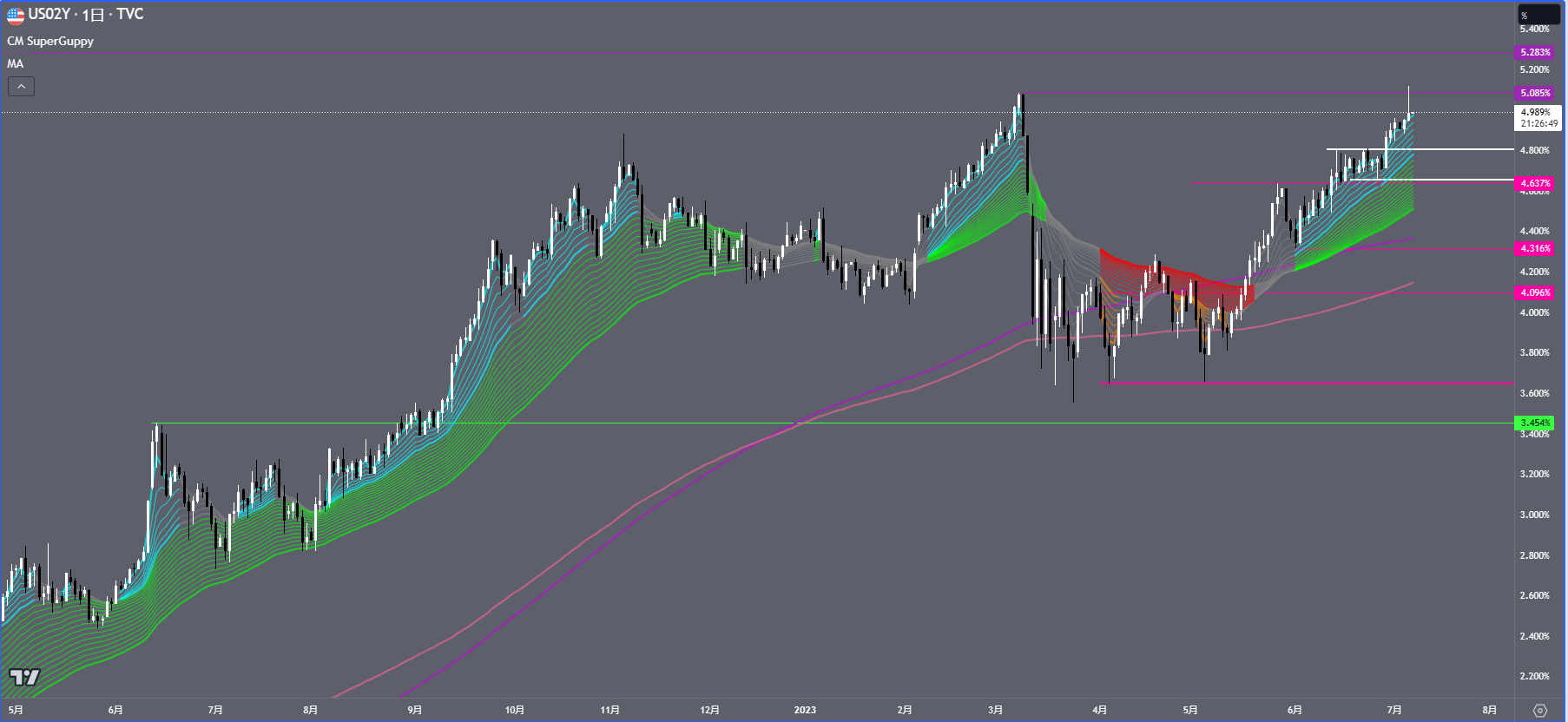

The 2-year yield is approaching the March high and briefly surpassed 5%. Depending on today’s results, a breakout is possible.

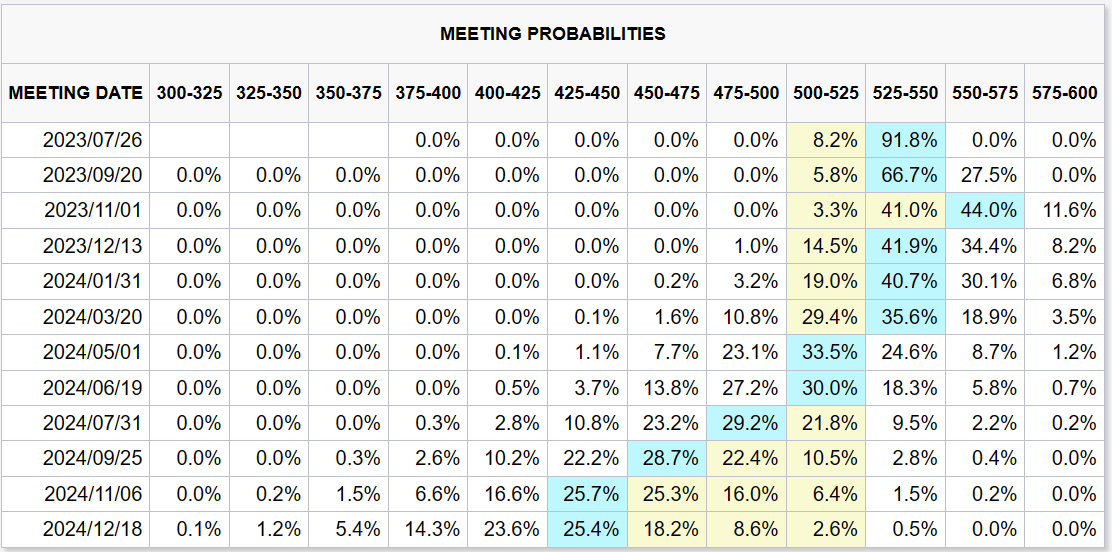

The market is pricing in two rate hikes this year. With a strong economy, three rate hikes are also coming into view to some extent. The Fed, aiming to fight inflation, is prepared to tackle the economy even at the risk of causing some damage, and will face it head-on.

Yesterday, the dollar was temporarily bought on the ADP news, but as the market moved toward the close, positions were reduced around theロンフィク boundary (note: likely a term referring to a market boundary). This suggests that today’s employment statistics are being factored in and anticipated.