What is FX

FX is the abbreviation for「Foreign Exchange」.

Originally it meant “foreign exchange trading,” but recently it has become a common term referring to「foreign exchange margin trading」.「foreign exchange trading」 and「foreign exchange margin trading」 differ in whether the foreign exchange trading is done with a margin or not.

In short,「currency exchange」, right?

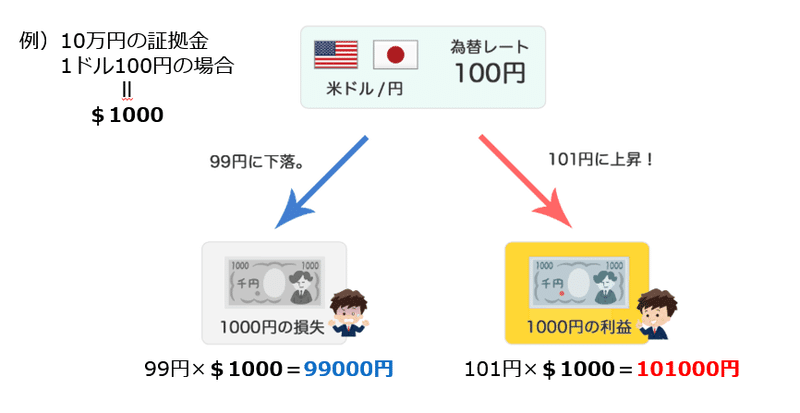

This diagram shows a buy order when 1 dollar = 100 yen.

If the price rises to 101 yen, the difference of 「1 yen」becomes a profit, and if the price falls to 99 yen, the difference of 「1 yen」becomes a loss.

This time it was a buy order, but if you place a sell order, the result would be the opposite.

If the price rises to 101 yen, the difference of 「1 yen」becomes a loss, and if the price falls to 99 yen, the difference of 「1 yen」becomes a profit.

Trading currencies from other countries like this is called「FX」.

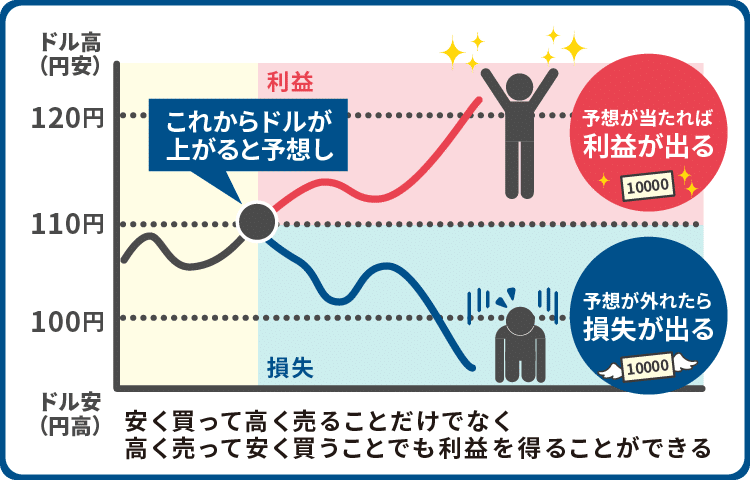

Buy when it is cheap, and sell when it is high.

Conversely, sell when it is high, and ride out the rise before it happens.

I think this kind of trading is a game of accumulating profits through repetition.

If you visualize it, it looks like this.

If you think it will rise, buy; if you think it will fall, sell.

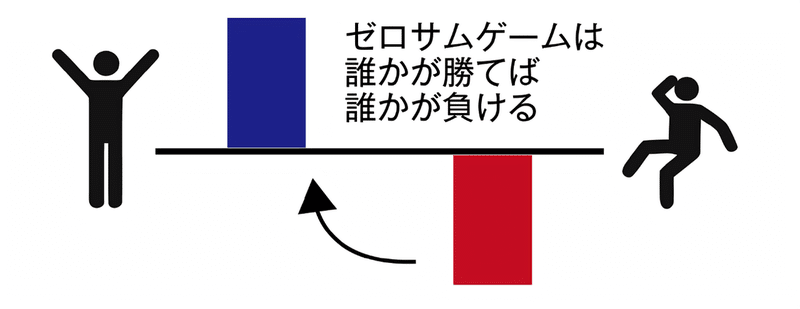

It may feel like a binary gamble, butworld events and human psychology make it a complex and difficult zero-sum game..

Zero-sum game

FX is called a “zero-sum game,” where when someone wins, someone else loses.

It’s a merciless world like that.

Someone else’s loss becomes someone else’s gain.

Domestic accounts and overseas accounts

When trading FX, the most popular method is「securities account」 or「broker」

Securities companies are divided into「overseas」 and「domestic」, each with its own merits and drawbacks.

There are advantages and disadvantages to each, so this note will describe them and end there.

Merits of domestic accounts

1. There is capital preservation, so even if the securities company goes bankrupt, internal funds are often preserved.

In other words, you get refunded.

2. If you make more than 3.3 million yen in profit, taxes are lower domestically.

Overseas is taxed progressively, so as profits increase, tax rate increases, but domesticallya flat 20%.

Even overseas accounts have up to 3.3 million yen taxed at 20% or less, so 3.3 million yen is considered a tax tipping point.

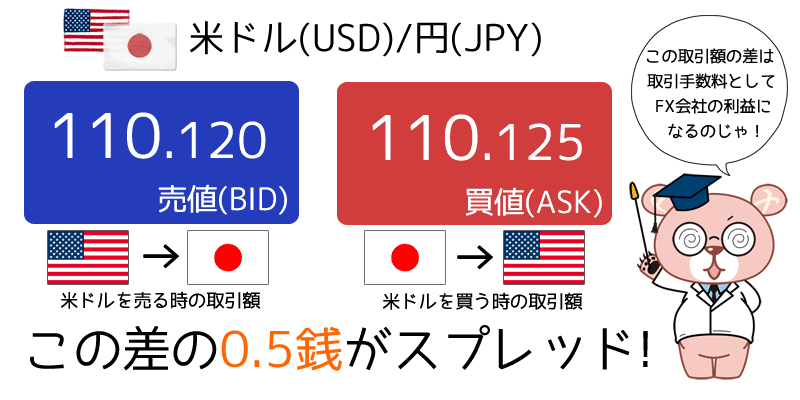

3. Narrow spreads.

The spread is like a “fee.”

Details will be explained later in the note, but domestically you can trade with spreads about half of overseas.

Demerits of domestic accounts

1. There is an additional margin system.

Overseas accounts have「zero-cut system」

However, domestic accounts have “additional margin,” or “calls for margin,” so if you incur a loss beyond your deposit, it becomesa debt.

2. Leverage is up to 25x.

For corporate accounts it can be up to 100x, but basically domestic accounts haveleverage of 25x.

Leverage typically gives a sense of higher gambling risk, but I believe leverage is there to protect a trader’s margin, so it is the opposite of fear.

That’s all for domestic accounts.

Next, about overseas accounts

Merits of overseas accounts

1. Zero-cut system

A big benefit, isn’t it?

You cannot lose more than your deposited amount, which is reassuring.

2. High leverage

Overseas allows high leverage.

Leverage is a system to protect against zero-cut, in my view.

3. If profit is below 3.3 million yen, taxes are lower than domestically.

Here is a quick tax rate table.

Until 3.3 million, it’s inexpensive.

Therefore, moving beyond 3.3 million yen to overseas and then back domestically is the most tax-efficient flow, I think.

4. Many brokers offer generous bonuses.

Bonuses are advantageous if you can receive them.

Because you can trade more than your own funds, your potential earnings increase.

Domestically, you don’t hear many bonuses like that.

Demerits of overseas accounts

1. Many brokers lack capital preservation and financial licenses.

Without capital preservation or financial licenses, even if the broker goes bankrupt,the money in your trading account is not guaranteed.

More than that,there is a risk of running off with your funds.

2. Spreads tend to be wider than domestic accounts.

Most brokers have spreads about twice as wide as domestic accounts.

3. Higher risk of withdrawal refusals compared to domestic accounts.

Many brokers will refuse withdrawals with unreasonable complaints.

Please be very careful when opening and funding.

That’s all for today.

To be continued next time.

Thank you!