This week's forecast

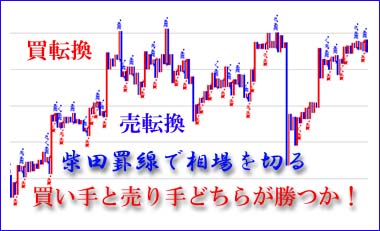

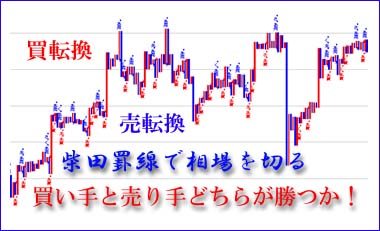

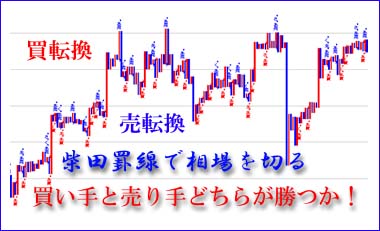

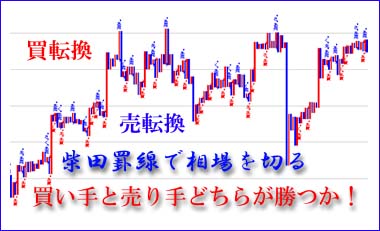

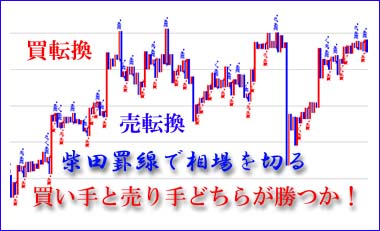

Market Observation from Shibata Rule Line

<This week expects a range of 28,500 to 29,700 yen>

Last week's unexpected rise in the Nikkei Average was supported by buying from overseas investors. The Nikkei Average closed Friday the 12th at 29,426 yen, confirming an intraday high for the year, indicating potential for further upside. However, due to the U.S. debt ceiling issue and lingering concerns about the stability of the financial system from regional bank troubles, the Dow Jones Industrial Average has been laboring, and market volatility could be triggered. While the debt ceiling issue is likely to be navigated again this time, the potential for market disruption remains non-negligible, and the mixture of financial anxiety and economic risks suggests a scenario where the market could stay unstable in the near term.

A major factor behind the recent rise in Japanese stocks has been buying by overseas investors, so if the U.S. market trembles due to the debt ceiling issue, its impact cannot be avoided. Still, Japanese companies are actively returning value to shareholders, and the comparatively cheap valuation of Japanese equities provides medium-term supportive material. For this week, earnings reports will largely be out by Monday the 15th, which could allow for a speed adjustment; if that occurs, it can be viewed as a buying opportunity.

Indicator Analysis

Nikkei Average

<Last week's movement>

Last week, after recovering to the 29,000 level on May 1 and 2 during the Golden Week lull, a pause was expected.

As a result, on Tuesday the 9th, aided by gains in U.S. stocks and a weaker yen, it rose by 292 points to 29,242, reaching a year-to-date high. A pause followed, with a range around 29,000.

However, on Friday the 12th, during mini-option SQ, the SQ value was 29,235, and the index rose further to 29,426, up 299 points, and closed at 29,388, up 261, a high not seen in a year and a half.

<Outlook for this week>

The Nikkei Average has already surpassed the long-term resistance around August last year’s high of 29,222, so a range of 28,500–29,700 yen is expected. With earnings reports wrapping up on Monday the 15th, if there is a speed adjustment, that would be a buying opportunity.

Dow Jones

<Last week's movement>

On Friday, April 28, major company earnings were well received, and the Dow rose by 272 points to 34,098, reclaiming the 34,000 level. On Monday, May 1, it rose to 34,257, but then peaked and pulled back, with concerns about prolonged rate hikes, potential government asset depletion by June 1, renewed regional bank distress, and other factors driving declines: Monday the 1st down 46, Tuesday the 2nd down 367, Wednesday the 3rd down 270, Thursday the 4th down 286, and Friday the 5th down 546 before a sharp rebound. Subsequently, concerns about the debt ceiling and regional banks’ troubles resurfaced, with further declines: Monday the 8th down 55, Tuesday the 9th down 56, Wednesday the 10th down 30, Thursday the 11th down 221, and Friday the 12th down 8 on weaker consumer sentiment from the University of Michigan.

<Outlook for this week>

This week, inflation remains unclear, and a consolidation range is likely to continue. The inflation slowdown signaled by April’s CPI and PPI readings has boosted expectations that rate hikes may pause, supporting stock prices as rates are priced in higher. However, May's University of Michigan consumer sentiment index showed unexpectedly higher long-term inflation expectations, leaving a possibility of further rate hikes and keeping rates higher for longer, which could restrain technology stock gains.

Earnings reports from major retailers and April retail sales will be watched, and concerns persist about consumer confidence amid high prices and rising interest rates. The broader financial system remains opaque, with little expectation of rapid market stabilization. With debt ceilings potentially hitting the limit again on June 1, vigilance remains, and President Biden is slated to visit Japan for the G7 summit.

Upcoming indicators include April retail sales, April industrial production, weekly initial jobless claims, and May's Philadelphia Fed manufacturing index.

FX (USD/JPY)

<Last week's movement>

Between the end of the previous long holiday and May 2, Tuesday, ahead of the FOMC meeting, the dollar was bought due to expectations of prolonged rate hikes, rising to 137.76 yen per dollar.

This level likely marks a near-term peak; on Thursday the 4th, news of regional bank distress pushed the yen down to around 133.50, closing at 134.23. Since then, the pair has hovered around 134–135 yen. Amid expectations of continued rate hikes, dollar buying has continued, while expectations for a rate cut later in the year have emerged, leading to mixed direction and lack of clear trend.

After the University of Michigan's consumer sentiment data on Friday the 12th, inflation concerns prolonged, pushing the dollar higher by more than 1 yen to 135.70 yen per dollar, as the yen weakened rapidly.

<Outlook for this week>

This week, U.S. inflation indicators are expected to show a slowing pace, and rate cuts may be priced in less, leading to a bias toward lower dollar sentiment. However, concerns about persistent inflation have diminished the likelihood of early monetary easing by the Fed, so higher rates and a stronger dollar could prevail. If inflation remains elevated and consumer spending shows improvement in indicators like April retail sales, dollar selling could lessen. A 134–136 yen range is anticipated.