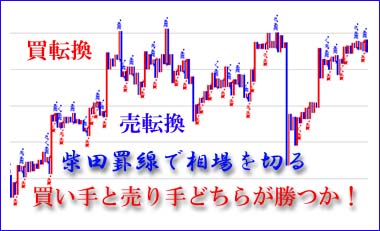

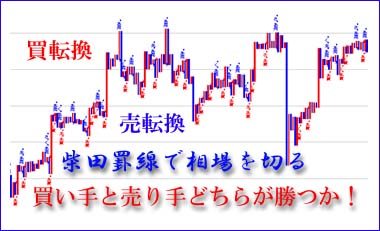

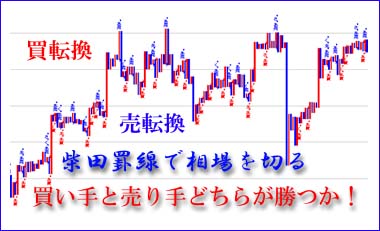

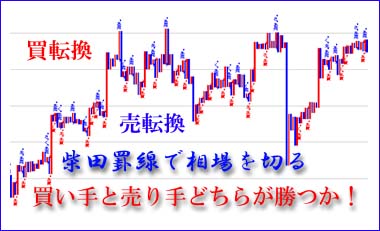

The September market ranges sideways, with a possible range of 27,300 to 28,600 yen.

In this week's forecast, since the August consumer price index will be announced in the United States on the night of the 13th (Tuesday) Japan time, if inflation confirms a slowdown, the U.S. market is expected to become more bullish, providing an additional tailwind for Japanese stocks.

In the early part of the month, based on past experience, it is suggested that September may test its lows, with a potential to fall to 27,268 yen on Wednesday, September 7, and to probe the downside.

However, on that day the U.S. market started with a rebound, entering a oversold rally, and the Nikkei Stock Average followed suit.

This week, it is projected to break through the resistance levels of March 25 at 28,338 yen and June 9 at 28,389 yen in one blow to 28,542 yen, up by 327 yen, and the next day the 13th (Tuesday) also rose 72 yen to 28,614 yen.

In the near term, upside seems heavy, but the rebound from the September 7 low has become larger, reducing the likelihood of probing for a bottom; for now, the focus is on confirming the August consumer price index.

Now, the August CPI released last night in Japan time surpassed market expectations (expected +8.1%, actual +8.3%), leading the NY Dow to plunge by 1,276 points for the fifth day in a row, and the Chicago Nikkei futures to fall 770 yen to 27,630 yen.

Today, the 14th (Wednesday), with the August CPI unexpectedly higher, the NY Dow plunged sharply, and the Nikkei Average opened down 481 yen at 28,132 yen, briefly fell to as low as 27,795 yen with a drop of 818 yen, and closed down 796 yen at 27,818 yen. Based on this movement, the downside is expected to be around the September 7 low of 27,268 yen, with the upside around the 28,600 yen level; the range is likely to oscillate within this band as the basic pattern for September markets. In the near term, a sense of uncertainty is likely to linger ahead of the FOMC meeting on the 20–21st next week.

× ![]()