This week's forecast

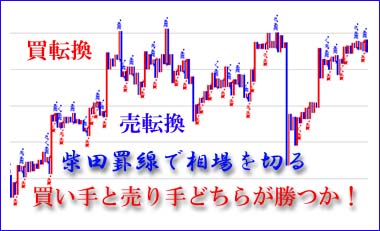

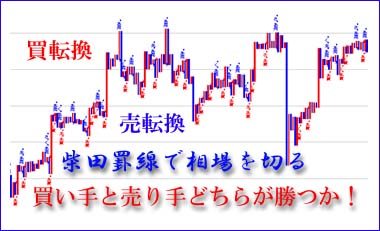

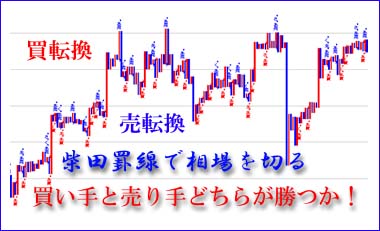

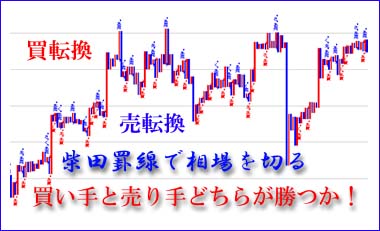

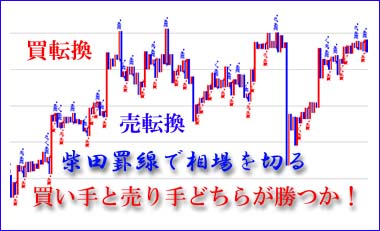

Market Observation from Shibata Lines

Last week, the market became wary again of the Fed’s tightening, with a sharp drop in the first half, followed by a view that the decline may have been excessive, and a choppy scene in the latter half with some rebound, but the Nikkei average fell for the fourth week in a row.

However, after-hours on the US market, Powell’s remarks emphasized that it is necessary to maintain a restrictive monetary policy for a while, causing the NY Dow to plunge by 1008 dollars.

In our forecast from last week, since the box range had been broken to the upside after a lengthy consolidation, the near-term bottom was seen around 27700 yen, with an expected range of 28000–29300 yen.

As a result, after peaking at 29222 yen on August 17, last week’s high was 28828 yen on the 22nd (Mon), and it fell to 28282 yen on the 24th (Wed), finishing the week at 28641 yen.

However, the weekend’s sharp drop in the NY Dow by 1008 dollars to 32283 dollars and the Nikkei futures at a decline of 390 yen to 28220 yen suggest a test of 28000 yen this week. Powell’s speech has passed, but important US economic indicators will be released in quick succession, so we will respond while reviewing their contents. Japanese stocks are undervalued, but will be affected if US stocks correct.

The Nikkei average tends to track the NY Dow, so it is necessary to monitor the NY Dow’s movements. The NY Dow seems likely to briefly rebound after adjusting toward the 32000 level (the 25-day moving average) after a near-term dip to 32828 dollars on the 24th, while the 34,281 dollars on the 16th looms as a near-term high.

Ultimately, on Friday the 26th, with a drop of 1008 dollars to 32283 dollars, it broke below the 32828 dollars low of the 24th, suggesting a re-adjustment is possible.

During this period, the Nikkei average has its near-term peak at 29222 yen on the 17th, and hit a low of 28282 yen on the 24th. This low approaches the 25-day moving average (as of the 26th, 28246 yen), so this week the market will first test this level, then test the 28000 yen milestone. It seems best to stay on the sidelines for a while until the Nikkei proves a positive turn by either advancing beyond the 29222 yen high from the 17th or showing a favorable change.

Indicator Analysis

Nikkei Average

Our forecast last week anticipated a significant rise to 29222 yen on Aug 17, with supply-demand dynamics calming after a short-term surge driven by buying pressure.

The near term would see a test of downside from this peak. On the 26th week’s end, at the Jackson Hole meeting, Powell’s remarks suggested vigilance toward rate hikes. Within the 28000–29300 yen range, a bottom-testing phase was considered.

As a result, in the first half of the week on the 24th (Wed), it fell to 28282 yen, then rose to 28792 yen on the 25th (Fri), finishing at 28641 yen in a range around 28500 yen. However, after Powell’s speech on the weekend, the NY Dow dropped by 1008 dollars to 32220 dollars, and the Chicago Nikkei futures stood at 28220 yen, down 390 yen.

This week, following last weekend’s NY Dow drop of 1008 dollars to 32283 dollars, Chicago Nikkei futures are down 390 yen to 28220 yen. The Nikkei average will test the 28282 yen low from the 24th, but this level is supported by the 25-day moving average (as of the 26th, 28246 yen). If this level breaks, the 28000 yen level becomes a key support, and depending on NY Dow movements, the market may search for a bottom around 27600 yen in a trading range.

NYSE Dow

Our forecast last week expected a pause after a move into the 34000s for the first time in about three and a half months, around Aug 25–27 Jackson Hole meeting and Powell’s remarks, with vigilance toward rate hikes. After initially pausing, the NY Dow fell to 33063 dollars by 22nd (Mon), then 32909 dollars on the 23rd (Tue), dipping below 33000. Later, concern eased, and on the 24th (Wed) it rose 59 dollars, and on the 25th (Thu) by 322 dollars to 33291 dollars, reclaiming the 33000 level.

This week will be a holiday-shortened week for Labor Day on Monday, Sep 5, leading to limited participation and a tendency for early adjustments. Important economic indicators such as the employment report and ISM manufacturing index will be released, so the market is expected to remain sensitive to rate movements. Powell’s measures to restrain inflation will keep monetary tightening in focus, and expectations for rate cuts are likely to retreat, weighing on near-term sentiment.

Forex (Dollar/Yen)

Last week, the dollar rose to 137.71 yen in the first half, but then fell below 136 yen on concerns over weak economic data. On the 26th, Powell’s remark that “it is necessary to maintain a restrictive monetary policy for some time” pushed back expectations for early rate cuts, and the dollar retraced to the upper 135s. The week ended at 137.64 yen.

With the possibility that rate hikes may continue through 2023, near-term expectations for higher policy rates will support less risk-averse dollar selling and less yen buying. At the upcoming FOMC on Sep 20–21, a 0.75 percentage point rate hike is likely, keeping the dollar firm.