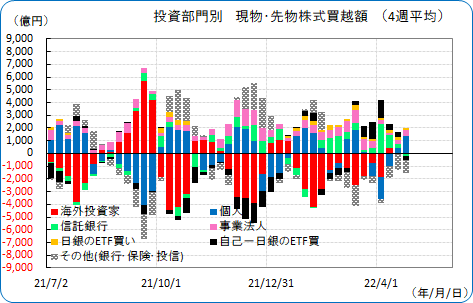

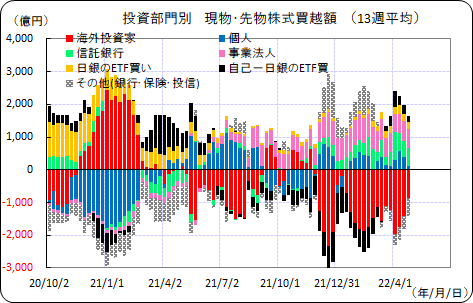

Japanese stock investment sector demand and supply from Tokyo Stock Exchange data

There is nothing particularly noteworthy, so I will jot down what I noticed.

Unless otherwise noted, this is for the week of April 18–22.

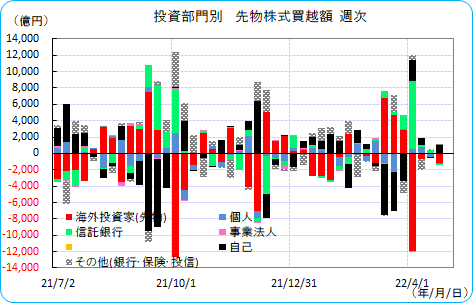

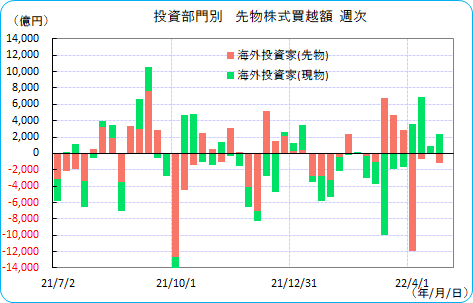

First, futures. Foreign investors (red) are selling slightly. In response, the securities companies act on their own account.

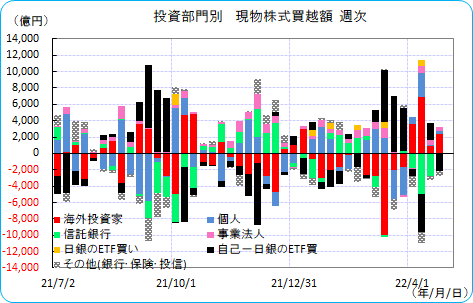

Looking at the spot market, foreign investors are buying. On the other hand, securities firms on their own account are selling. They are opposite to the futures market.

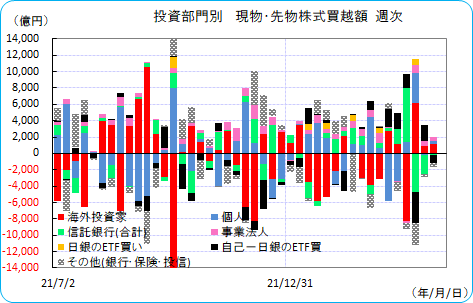

When you total futures and spot, you get a pattern of foreign buying and securities firm selling. Individuals are buying a little as well.

Turning to foreign investors,

for three weeks in a row since the week of March 11, hedge funds and others were buying in futures, while pensions and others were selling in the spot market, but

since the week of April 1, the trend has reversed. Since then, pensions and others have been buying in the spot while hedge funds and others have been selling in futures.

Ideally, hedge funds would quickly step in and push up prices, with pensions etc. chasing after, but there is no strength at all. Hedge funds are exiting too quickly.

Looking at a four-week basis, net buying is only by individuals and corporate-related funds (mostly share buybacks) and the Bank of Japan. Foreign investors are not clearly visible in the graph, with a four-week average of a 2.2 billion yen net selling. During this period, the TOPIX fell by 76.3 points. It is hard to rise unless foreign investors come into the market.

On a 13-week (three-month) basis, you can see the supply-demand trend. Foreign investors are net sellers. Without foreign buyers turning net buyers, a rising market is unlikely.

Meanwhile, buyers have been stable recently in share buybacks by companies themselves. Trusts (mainly pensions) are likely buying for rebalancing. The BoJ and a few others account for the rest.

For precaution, prices are determined by supply and demand, but retrospective supply and demand show that buys and sells align. Of course. If someone buys, there will always be someone who sells it. Therefore, even if you talk about supply and demand, the pre-existing supply-demand (those who want to buy more or sell more) is more important. Investors who want to buy cheaply (or sell when prices rise) do not determine the market. The investors who first drive prices down (or up) are necessary—the ones who actually set the market.

Moreover, investors like the BoJ, who will absolutely buy when prices fall (and will not sell even if prices rise) and who have large amounts and a budget for annual purchases, gradually influence the market.

Even the GPIF’s past large-scale changes in its basic portfolio would move the market by purchasing regardless of market conditions.

As for individual trading activity,

the Tokyo Stock Exchange publishes the breakdown of trading by investor type (individuals). The figures are augmented by estimates of the amount of stocks individuals are purchasing through public offerings and secondary offerings, to provide a figure that more closely reflects actual individual stock purchases, and this is published on the following site.