This week's forecast

Market Observation from a Technical Perspective

Following the decline trend in the U.S. markets last weekend, today's Nikkei Stock Average opened lower, with a brief deterioration to 29,542 yen after 9:30, finishing at 29,774 yen up 28 yen, and the TOPIX at 2,042 points down 1 point.

However, after the selling momentum subsided, a rebound occurred on the back of buying on dips, and in the afternoon it rose to 29,806 yen, broadly confirming the bottoming of the downside.

In Europe, Austria has implemented another lockdown as infections of the novel coronavirus rise again. In Germany, infections are also increasing, raising concerns about negative effects on the European economy; however, there are no signs of a resurgence in Japan, and there is hope that funds may flow from Europe to Japan as a result.

The current state of the Japanese market remains technically in a short-term upward trend, with no change in the view that the Nikkei will recover to around 30,000 yen, though upside remains heavy.

For a while, the market is likely to consolidate while absorbing a return-move selling; however, the investment environment will continue to favor stock-picking and buying on dips.

In Europe, the U.S., and Korea, coronavirus infections are rising again, and there are growing concerns about potential negative impacts on the economy and headwinds for the stock market.

But the major difference from the past is the widespread vaccination, development of therapeutics progressing, and the imminent availability of oral medications for treatment.

The biggest difference is the substantial reduction in deaths and severe cases. In that sense, measures that would unnecessarily halt the economy are limited, so there is no need for excessive pessimism.

Also, in Japan there are no signs of re-expansion of infections, domestic economic reopening is underway, large-scale economic stimulus measures have been decided, and there is hope that funds will flow from Europe to the Japanese market.

Simply put, there is a possibility that funds will move from selling European equities to buying Japanese stocks.

Until now, funds expecting economic recovery flowed mainly into Europe and the U.S., but with increased uncertainty about Europe’s outlook, there may be moves to switch from European stocks to Japanese stocks.

Quarterly earnings results have ended, Japanese corporate earnings have been solid, many attractively priced stocks exist, and large-scale government economic measures have been decided, which provides a reason to shift from European stocks to Japanese stocks.

The major reason for shifting is that infections in Japan have almost settled.

In the U.S., as December approaches, the debt ceiling issue will surface again, tapering in monetary policy will begin, and expectations for a rate-hike timing will intensify.

It would not be surprising if there is movement to switch from expensive U.S. stocks to undervalued Japanese stocks.

From the viewpoint of global capital flows, if money shifts to rebalance away from being skewed toward the U.S. and Europe, it will be positive for Japanese stocks.

Tomorrow’s Japanese market will be closed for Labor Thanksgiving Day. This week, markets will likely react to Europe’s coronavirus situation, but in Japan, the baseline stance remains stock-picking with buying on dips for strong-performing stocks.

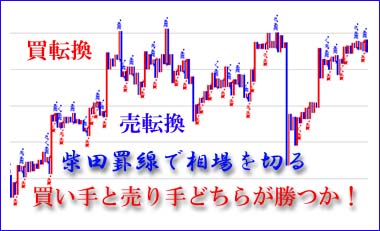

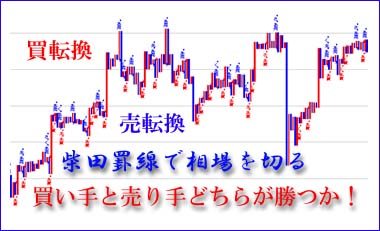

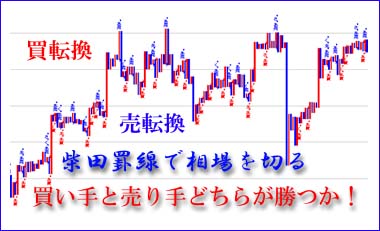

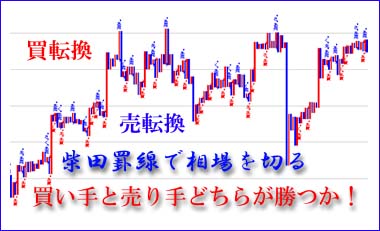

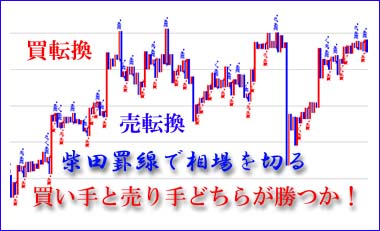

Market Observation from Shibata Lines

<This week, with holidays in between, will 29,200–30,000 yen continue as a box range?>

This week’s Nikkei Average is likely to continue the “close yet distant 30,000” theme. With a holiday tomorrow, a return to 30,000 is difficult. Even if the three major U.S. indices reach new highs, the Japanese market is unlikely to follow due to foreign buyers who are wary of Japanese politics.

On the 19th, Kishida’s administration announced the largest ever fiscal expenditure of 55.7 trillion yen as economic measures. The day before, the 18th (Thursday), upon the report, the market briefly surged but was soon pushed down by selling.

This week, attention will be on whether large-scale fiscal measures will again spark an upside move. Headlines cite a distribution-focused pillar with a total project scale of 78.9 trillion yen, but foreign investors’ lack of enthusiasm for this distribution-focused approach is said to stem from the market’s souring mood toward “distribution,” implying that investors’ share would be reduced, hence concerns about Kishida’s economic policy.

There is also talk that the strengthening of financial income tax is resurfacing, which adds to cautious sentiment. The Kishida administration must clearly present growth-oriented policies before distributions to reassure foreign investors; otherwise, even if the 30,000 level is briefly achieved, there may be no strong upside.

Currently, it is a box range between 29,000 and 30,000 yen, but from the August 20 low of 26,954 yen to the October 6 low of 27,293 yen, the October 25 low of 28,472 yen, and the November 1 low of 29,040 yen, the downside has been climbing steadily.

Against that backdrop, the November anomaly suggests that infections from the novel coronavirus may be subsiding, corporate earnings may be revised upward, and large-scale economic measures have been announced, creating expectations for further gains.

In terms of chart analysis, the daily 25-day moving average (as of the 19th: 29,302 yen) and the support line from the October 6 low of 27,293 yen near 29,700 yen indicate an ongoing upward trend, and this week the “close yet distant 30,000” may be cleared.

Indicator Analysis

Nikkei Average

Last week’s forecast suggested that within a 29,000–30,000 yen range, if the intraday low of 29,040 yen on November 11 were to be surpassed by closing above 29,880 yen reached earlier in the week, a return to the 30,000 level could be anticipated.

The week began with solid U.S. stock performance and support from Chinese equities, pushing November 16 (Tuesday) to 29,960 yen, higher than 29,880 yen earlier in the week, but the closing failed to clear the level, finishing at 29,808 yen, up 31 yen. On the 18th (Thursday), the index fell to 29,402 yen; the economic measures announced on the 19th were reported to be a record 55.7 trillion yen, and a rebound to 29,715 yen followed, but selling retraced to 29,598 yen, down 89 yen. On Friday the 19th, the Nikkei ended at 29,745 yen, up 147 yen, after the Nasdaq hit new highs.

This week, Monday the 23rd is a holiday and markets are likely to be thin. First, market reactions to Kishida’s distribution-focused 78.9 trillion yen project (costing 55.7 trillion yen) will be watched closely.

If foreign investors react positively, it could pave the way to a return to 30,000 yen, but the focus on distribution and lack of a clear growth policy is concerning.

From Shibata’s chart, the uptrend A that began from 16 March 2020 at 16,358 yen peaked at 30,795 yen on 14 September, then dropped to 27,293 yen on 6 October; the recovery from there has shifted the 30,000 level into a resistance line of the uptrend (A). A major trigger is required for a return to 30,000.

NY Dow

Last week’s forecast suggested that if October retail sales and retail earnings were strong, stock prices would rise, but if inflation accelerates, expectations for an early rate hike could push prices lower.

Early in the week, the Dow rose on expectations of falling long-term yields, but as retail sales data approached, traders waited. On November 16 (Tuesday), October retail sales beat expectations and the Dow rose to as high as 229 points, but closed down 54 points as it faced resistance. Following that, inflation and a resurgence of COVID-19 weighed on the Dow for three straight days, ending Friday the 19th at 35,601, down 268 points. However, tech stocks rose, and the Nasdaq hit new all-time highs for the second day in a row.

This week’s forecast expects Thursday the 25th to be a Thanksgiving holiday, and Friday the 26th to be a shortened trading session, leaving only Mon-Tue-Wed as trading days, which suggests limited movement. Attention is on President Biden’s nomination plan ahead of Thanksgiving; most expect Powell to be reappointed, but if Brainard is nominated, short-term uncertainty could trigger a decline.

In Europe, some countries plan lockdowns due to renewed coronavirus infections, which would negatively affect the stock market if they spread, though vaccines are expected to prevent large-scale outbreaks.

Forex (USD/JPY)

<Last week’s movement… dollar/yen hits a fresh year-to-date high on improving economic indicators>

U.S. October retail sales beat expectations, the 10-year yield rose, and dollar buying and yen selling strengthened. The dollar rose to 114.97 yen on November 17. Afterward, profit-taking led to dollar selling and yen buying, pushing below 114. On the 19th, the dollar briefly fell to 113.35 yen, but then the European Central Bank President’s statement that “no hurry to tighten policy” triggered euro selling and yen buying, contributing to dollar weakness.

However, when an Federal Reserve official supported accelerating the pace of tapering, the dollar’s decline paused, finishing at 114.01 yen.

<This Week’s Outlook… Will the dollar struggle for gains?>

Expectations for earlier Fed rate hikes have faded, but the European Central Bank’s measures are expected to remain in place for longer, so the dollar may continue to attract as a safe haven. Other major central banks remain cautious about tightening, which supports dollar buying. However, the 1 dollar = around 115 yen level remains a high area since March 2017, suggesting upside may be limited.