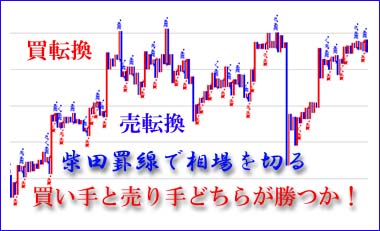

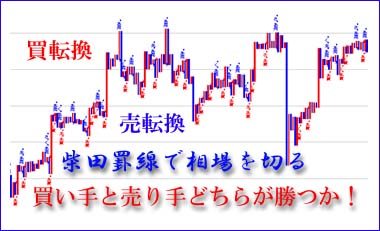

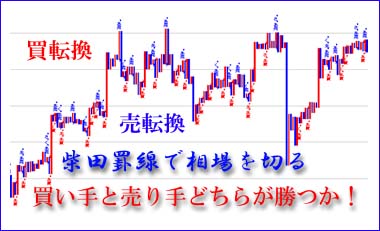

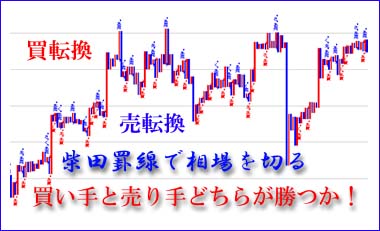

Reason for the near but distant recovery to the 30,000 yen range

In this week's forecast, it was posited that if the price closes above 29,880 yen on November 4, it could break into the 30,000 yen level, but yesterday, the 16th (Tuesday), it rose to 29,960 yen, but near 30,000 yen there was selling pressure, and the closing price was 29,808 yen, marking four consecutive days of gains but with upper resistance.

There is heavy selling around the 30,000 yen level, and many seem to believe that if it clears this level and recovers to the 30,000s, price movement will become lighter. Today it closed at 29,688 yen, down 119 yen.

Yesterday's currency movement saw the yen weaken to 114.85 per dollar, at one point the weakest in 1 year and 4 months. Normally Japanese export-related stocks would be heavily bought in such circumstances, but that did not happen. There are good and bad yen weakenings, and currently the bad kind is evident. This is because crude oil has surged and staying high, pushing up prices. In advanced economies, Japan has the worst income growth, so prices rise, worsening living standards. Even if profits are made on exports, imports become more expensive, further pushing up prices. Therefore, in the near term domestic demand stocks are lackluster, and one could say we are in a “near yet far” path to recovering the 30,000s.

① The core of exporters is Toyota Motor, which is highly profitable, but now it’s not that any Japanese car can be exported at high prices; rather, it’s Toyota-like high-quality-focused vehicles that are exported, and the ripple effect on other automakers is limited, so the overall tailwind for Japanese stocks is constrained by a shift in value.

② Raw materials (such as crude oil) costs and the ongoing yen depreciation worsen trade terms, shifting the weight of investment choices, making it harder to welcome the weak yen.

③ Even after the July-September quarterly results, the expected EPS (earnings per share) for the Nikkei average remains only modestly increased.

These points ①–③ are the major reasons for the “near yet far” recovery of the 30,000s. However, markets do not always move logically, so from factors such as rise in US stocks, a pause in crude oil prices, a pause in yen depreciation, and November’s anomalies, if a trigger arises, the 30,000s could be recovered, and if the closing price clears the September 14 year-to-date high of 30,670 yen, 31,000 yen could come into view.

× ![]()