Will the U.S. growth rate also slow down, and what will be the impact on stock prices?

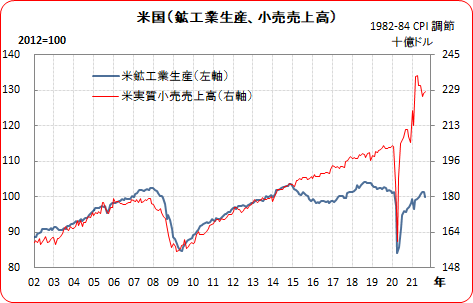

U.S. industrial production and retail sales for September have been released.

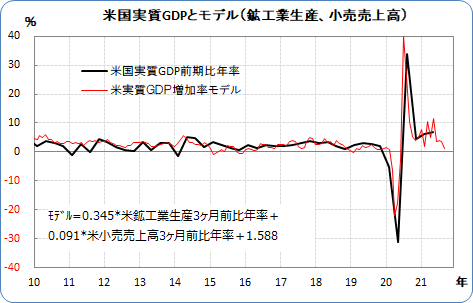

From both indicators, the estimated annualized quarterly growth rate of real GDP for July-September is 2.86%.

However, the estimated annualized growth rate for the three months to September has rapidly fallen to 1.03%.

China’s real GDP growth for July-September, due to China’s own circumstances, dropped sharply to 0.8% annualized, and the U.S. economy is also softening.

The backdrop to the slowdown in U.S. growth is

(1) the end of cash handouts from COVID-19 measures.

(2) amid a global semiconductor shortage, auto production has declined.

(3) the adverse effects of Hurricane Ida that struck the South at the end of August = mining operations were disrupted

The problem is that there is no clear prospect of improvement in the semiconductor shortage, and labor shortages continue, so manufacturing activity is expected to remain under pressure.

With the removal of cash handouts from COVID-19 measures, incomes have fallen. Still, due to labor shortages, the uptrend is likely to continue.

As above, growth is likely to stay stagnant going forward, but what about the impact on stock prices?