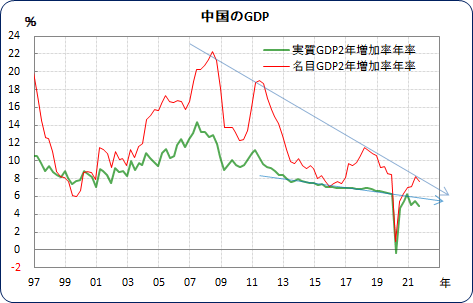

View of China's GDP

China's real GDP for July–September 2021 grew 4.9% year-on-year. Quarter-on-quarter it rose 0.2% (annualized 0.8%). Compared with the previous quarter (April–June), it was almost flat.

In the past, in China, maintaining employment for the people required 8% growth, and 8% growth was regarded as necessary to earn the people's trust in President Xi Jinping.

But that necessity no longer exists. Xi Jinping has become equivalent to Mao Zedong, holding the authority to rule the country for life.

If so, President Xi Jinping’s ideology (socialist thought) has shifted toward the political goal of common prosperity to rectify economic disparities, with concentrated tightening on the glamorous entertainment industry where wealth gathers, reducing the burden of education, tightening internet regulation, and strengthening regulation of the real estate market. In addition, to showcase China to the world, a decarbonization policy is being advanced.

As a result, housing sales, construction activity, consumption, and investment are being restrained. Moreover, due to the decarbonization policy, electricity shortages occurred in September, and manufacturing has been forced to scale back production or suspend operations.

Probably there will not be a return to high growth. The level of growth that is considered acceptable remains unclear for now.

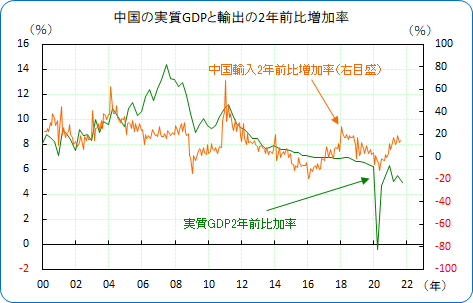

The next graph shows how much China’s GDP has grown compared with two years earlier.

Because last year’s growth was distorted, it cannot be compared with a distorted last year, so it is being compared with two years ago.

Real GDP (the concept of output) has shifted downward from the previous trend. This is probably the result of concentrating on the Cultural Revolution-like measures. At the same time,we can say that purchasing power has decreased (even if the purchasing amount does not change, the quantity purchased has decreased) due to inflation.

Indeed, the Chinese economy is softening, but from overseas perspectives there is no particular cause for concern. (There will likely be impacts on companies that sell to Chinese consumers, though.)

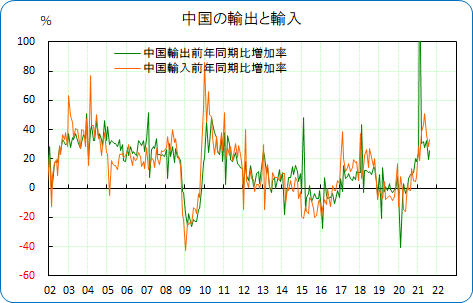

This is because exports and imports remain solid.

For resource-rich countries exporting resources to China, China is steadily increasing imports; for sectors relying on Chinese imports, China is steadily increasing exports.

China’s economic softening is China’s own problem. The credit issue of the Evergrande Group is basically a domestic issue for China.

China’s economic softening is not necessarily good news for Japan’s stock market, but there is no need to be overly pessimistic.